Financial difficulty is a big reality and there are various reasons that might lead you to get entangled in the web of borrowings and loans. No matter the amount of planning, you fail to fulfill your financial obligations. If you find yourself struggling to resolve your outstanding debts, you should compose a financial hardship letter so that lenders can consider what you propose.

Contents

Financial Hardship Letters

When do you need a financial hardship letter?

The main purpose of a financial hardship letter is to obtain leniency in payment deadlines or the consolidation of your outstanding debts. Moreover, you can also use this letter to prevent foreclosure, to help pay credit card debts, and medical bills.

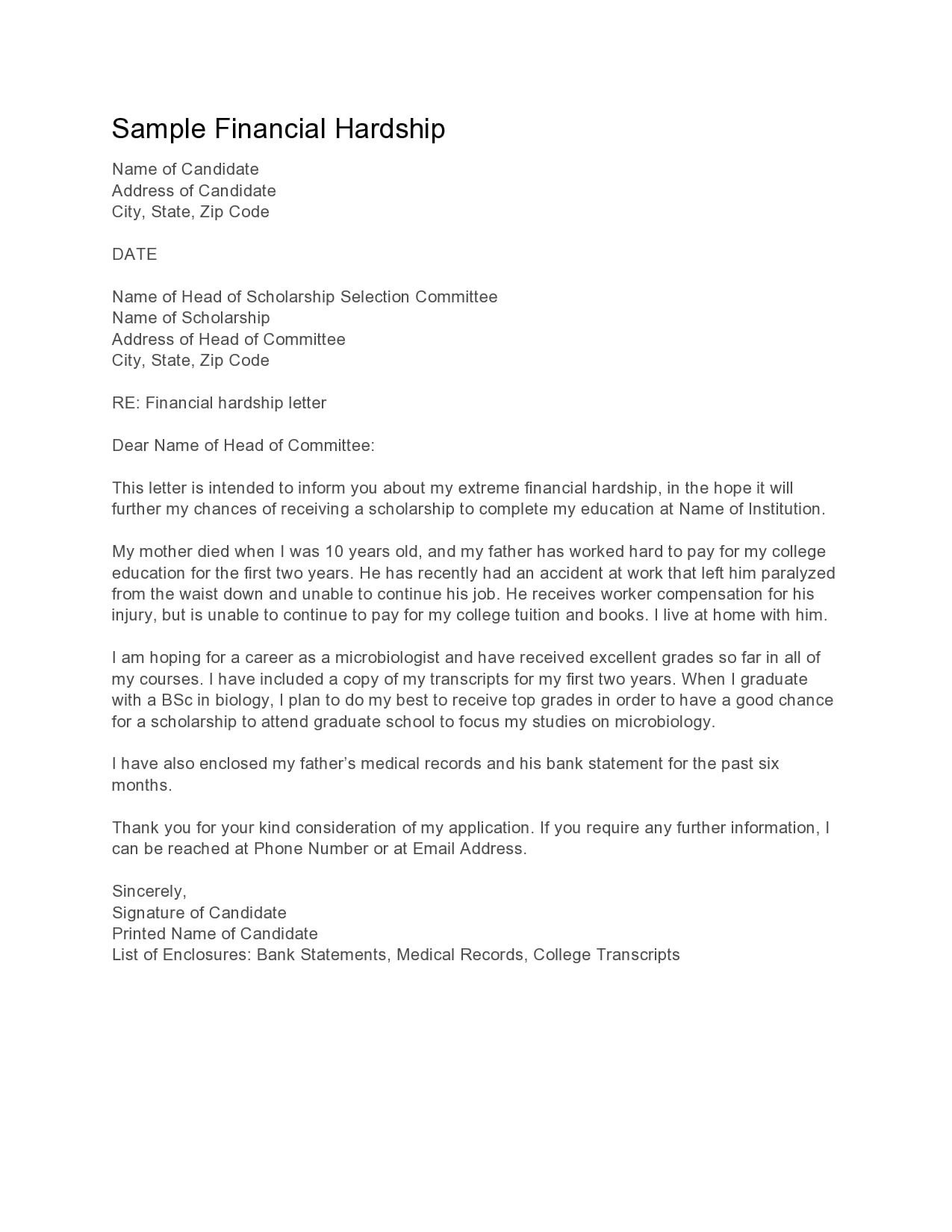

Students who can’t afford to pay for higher education may also write a debt hardship letter to increase the likelihood of obtaining a tuition fee reduction, a grant or a scholarship.

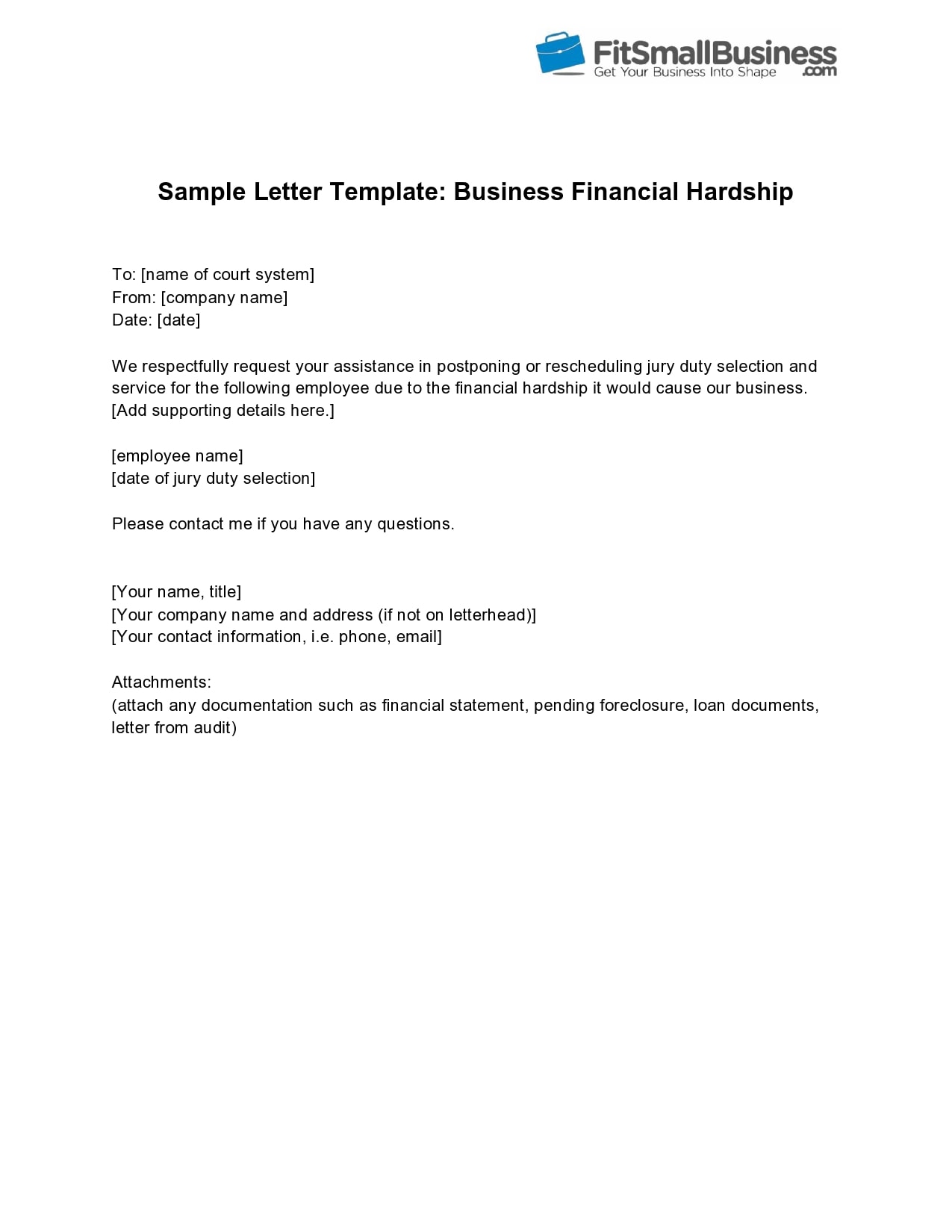

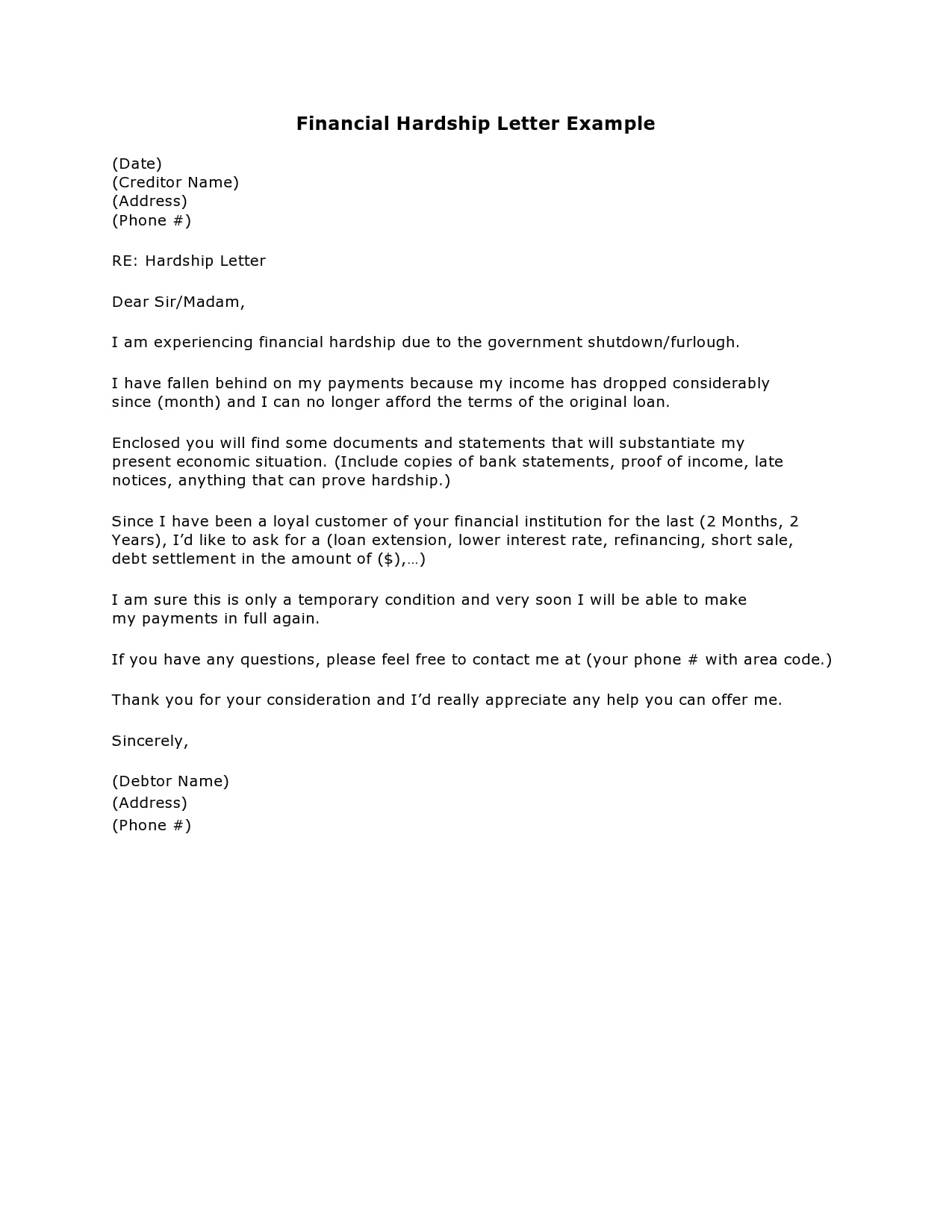

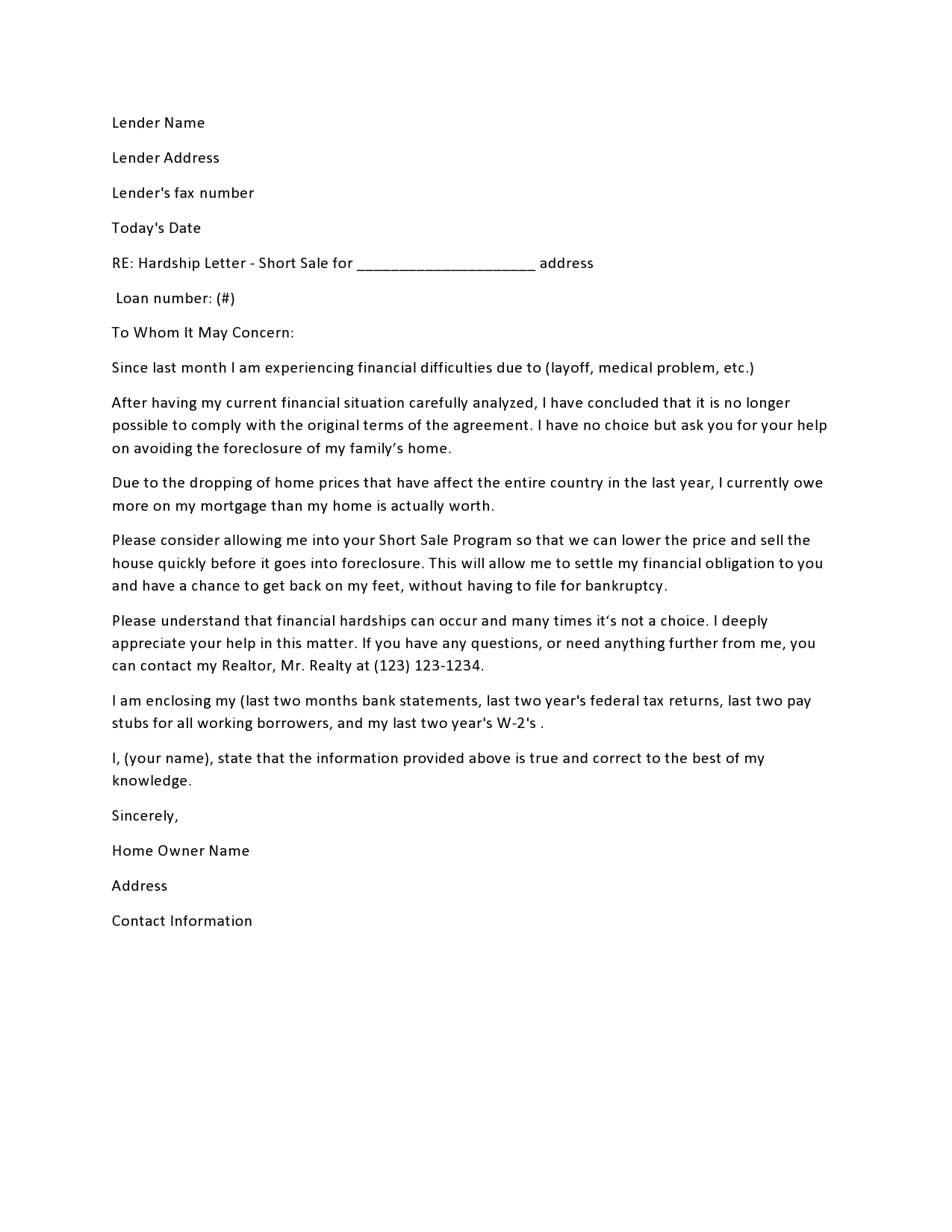

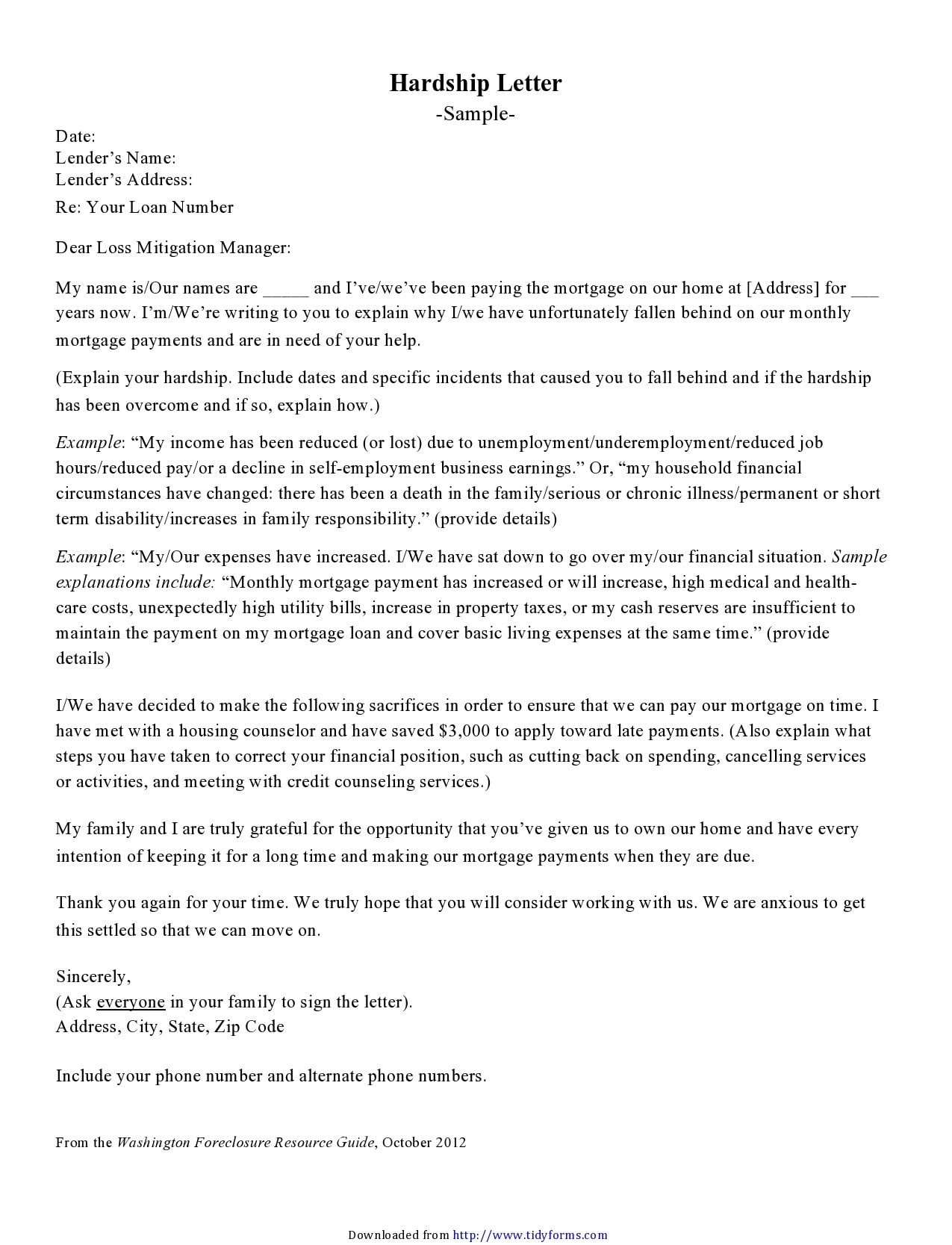

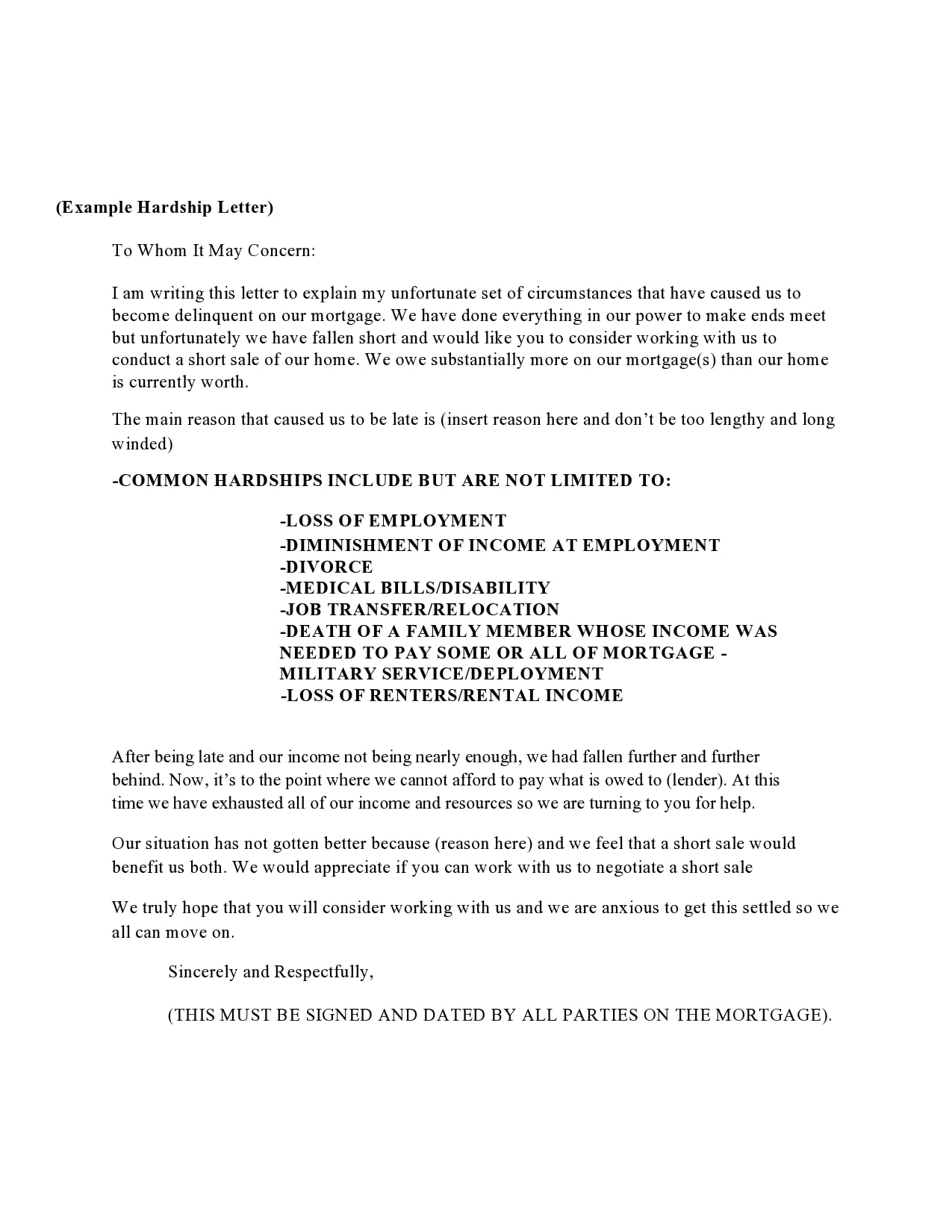

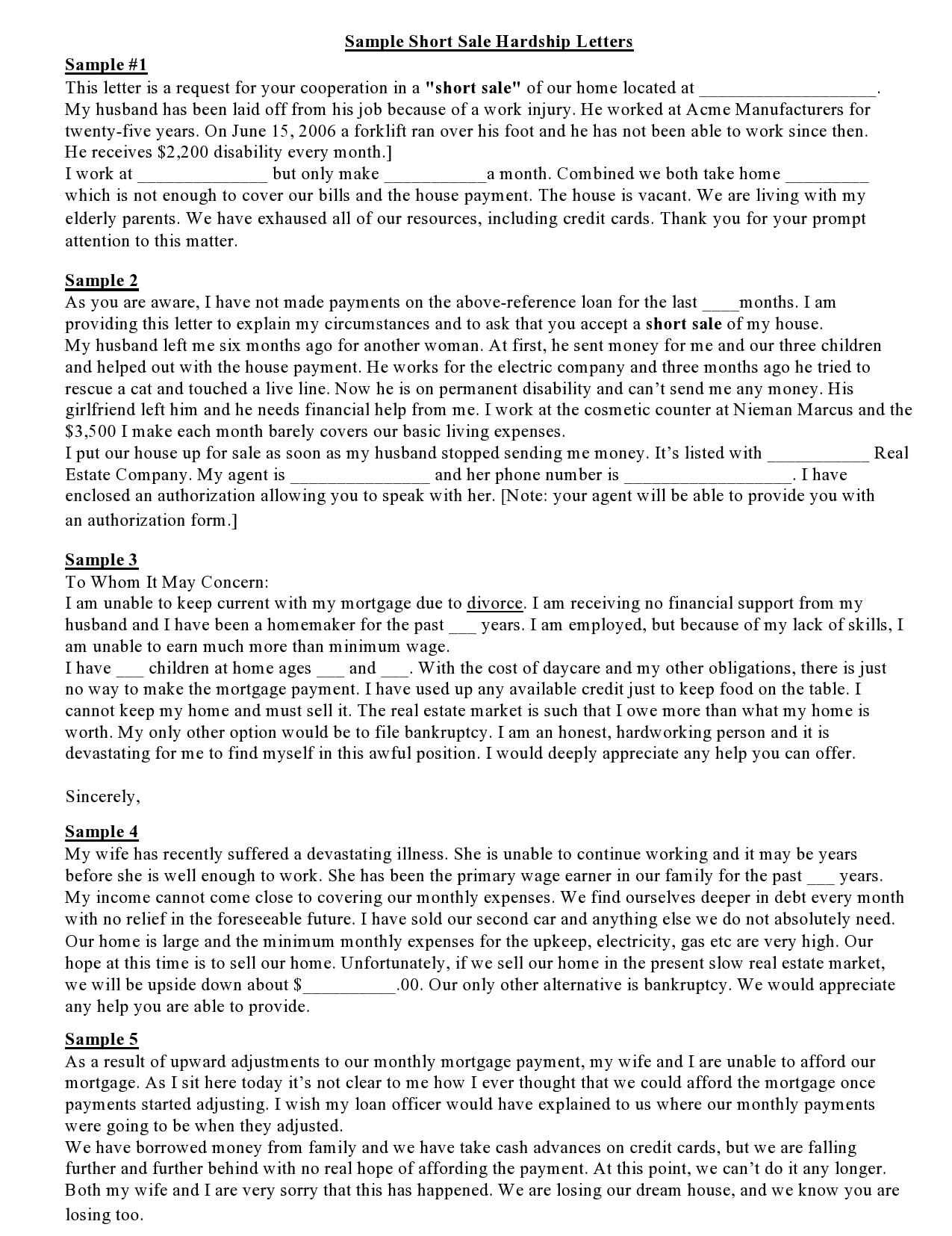

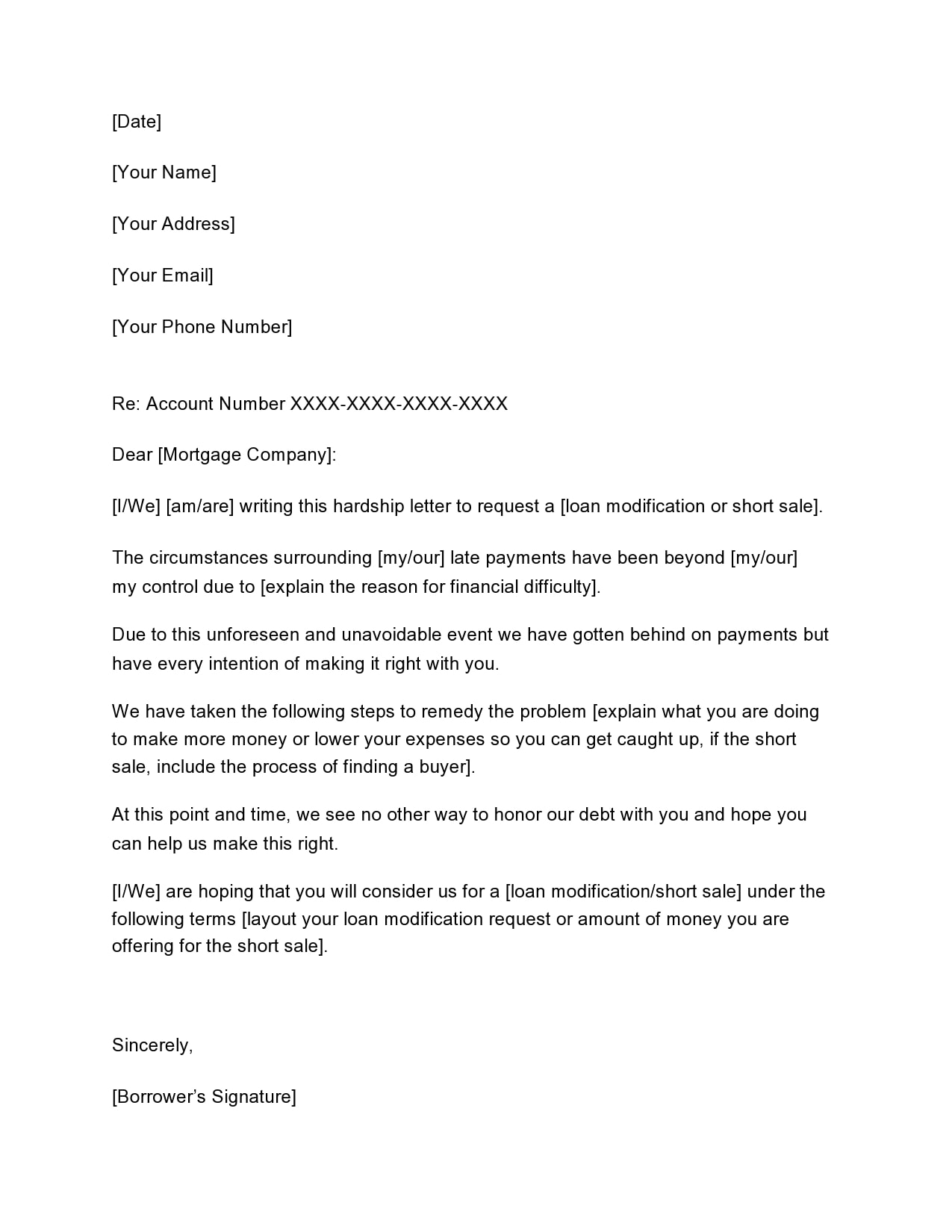

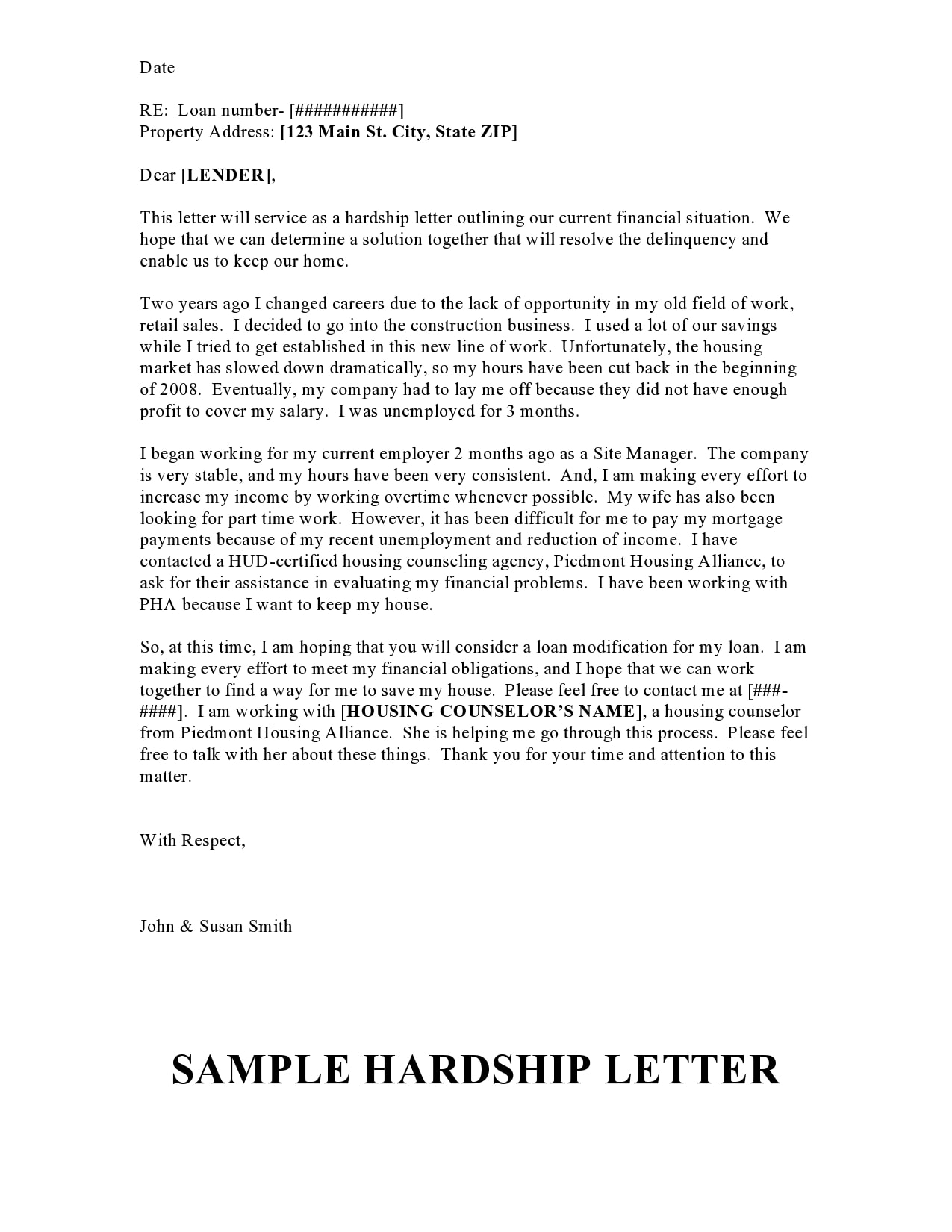

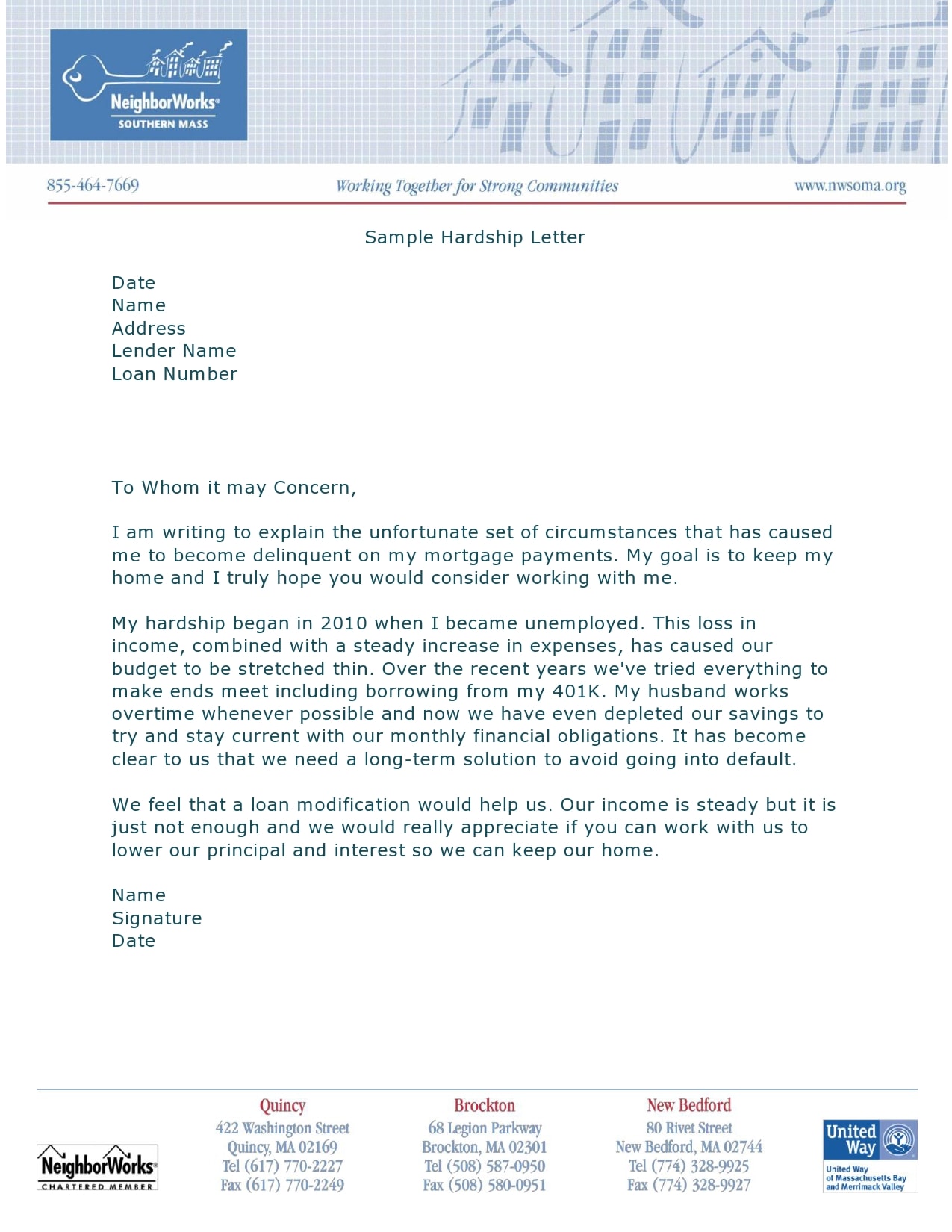

Many consider this letter as a common one. You send it to a lender to inform them that you’re in financial trouble and that you’re trying your best to sort things out. There are various reasons why people write these letters but the most common one is to make a request for a loan modification or a short sale to avoid foreclosure.

In such a case, even if you’re already represented by a lawyer, you as a homeowner must still present this letter as part of the loan modification process. To present the strongest possible case to the lender, your lawyer must submit the letter together with other important documentation.

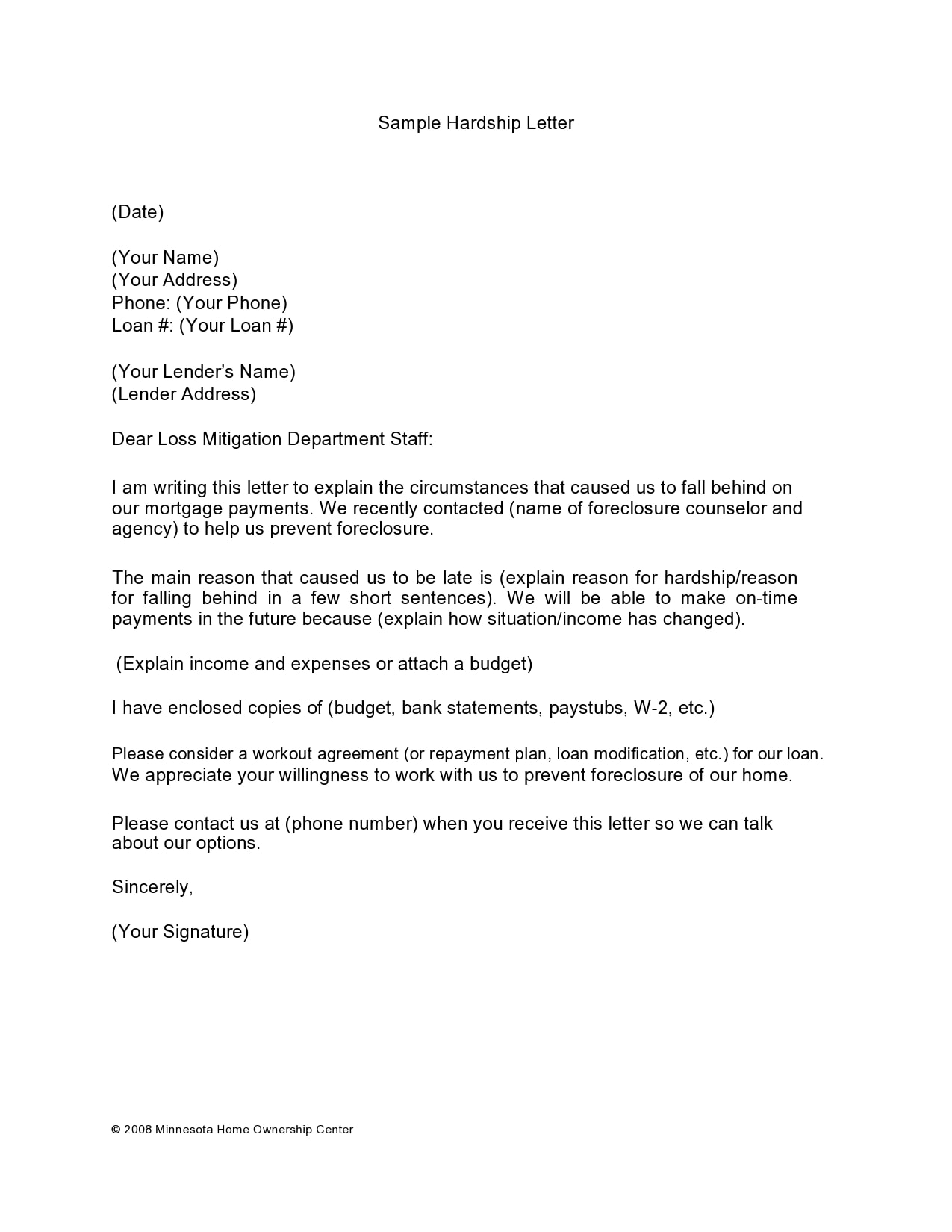

It’s important to write this letter if you’re having issues paying off your home mortgage. If you want the lender to consider you for a loan modification, a temporary repayment plan or a short sale, writing this letter becomes a mandatory requirement.

When you’re writing the letter for a loan modification, remember that it’s important to the lender to know the reason why you have missed your mortgage payments for a few months. This means that you have to be very honest when writing the letter.

More importantly, you should let your lenders know how you will support your future payments, should they make the decision to approve your request for a loan modification. You can convince the lender to forego foreclosure and make modifications to your loan instead if you can provide these details.

Debt Hardship Letters

What is an example of a hardship?

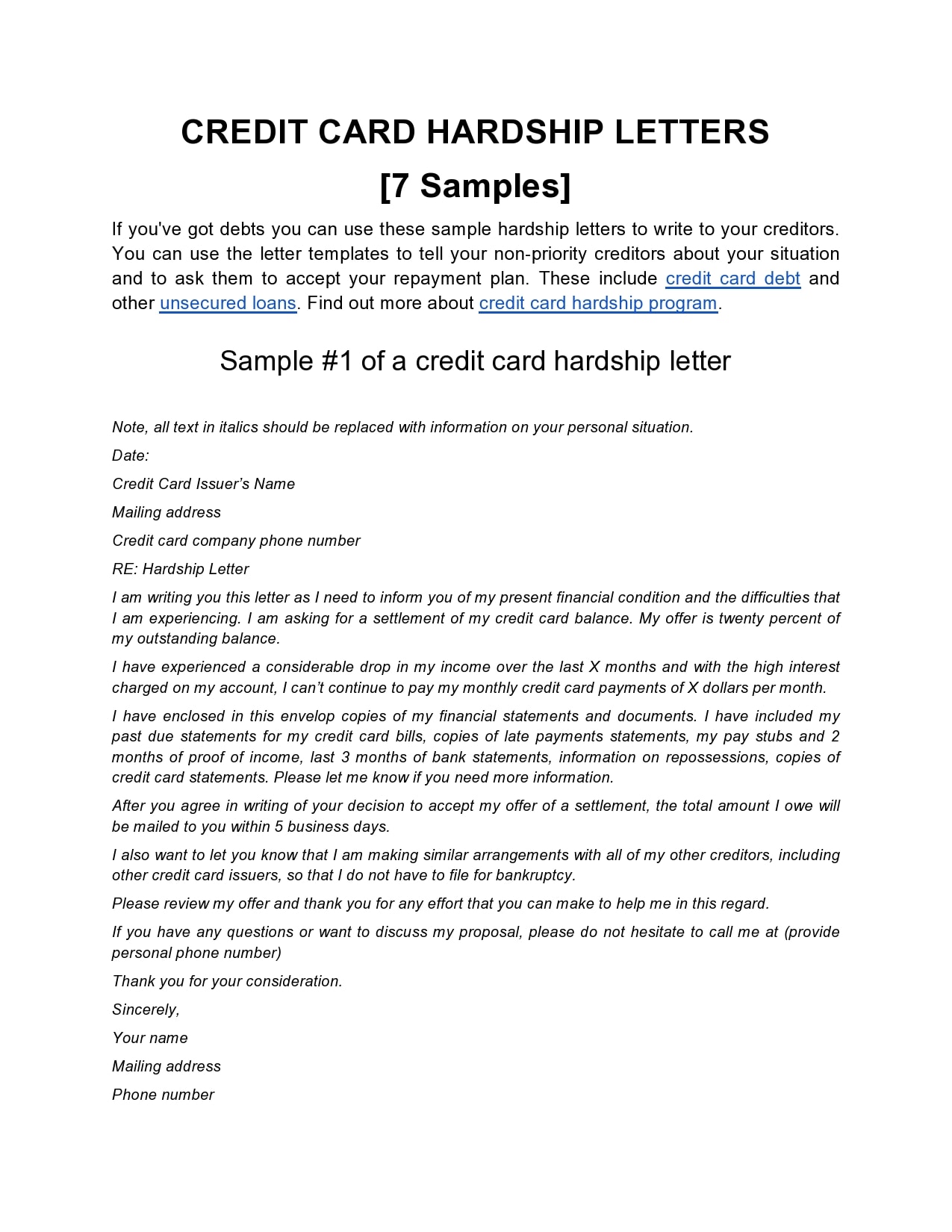

A financial hardship letter is usually written by those who cannot make their payments towards debt. It is the best way to explain to a lender why you’re lagging in your obligations. The lender can use the letter to decide whether or not they will offer relief either through deferred, suspended or reduced payments.

There are several situations that might qualify as a hardship. Although most of these are purely financial, there are some that may involve other life events. Here are the most common situations that may qualify as hardship:

- Change of your employment status

- Death

- Divorce

- Injury or illness

- Loss of income

- Military deployment

- Natural disasters

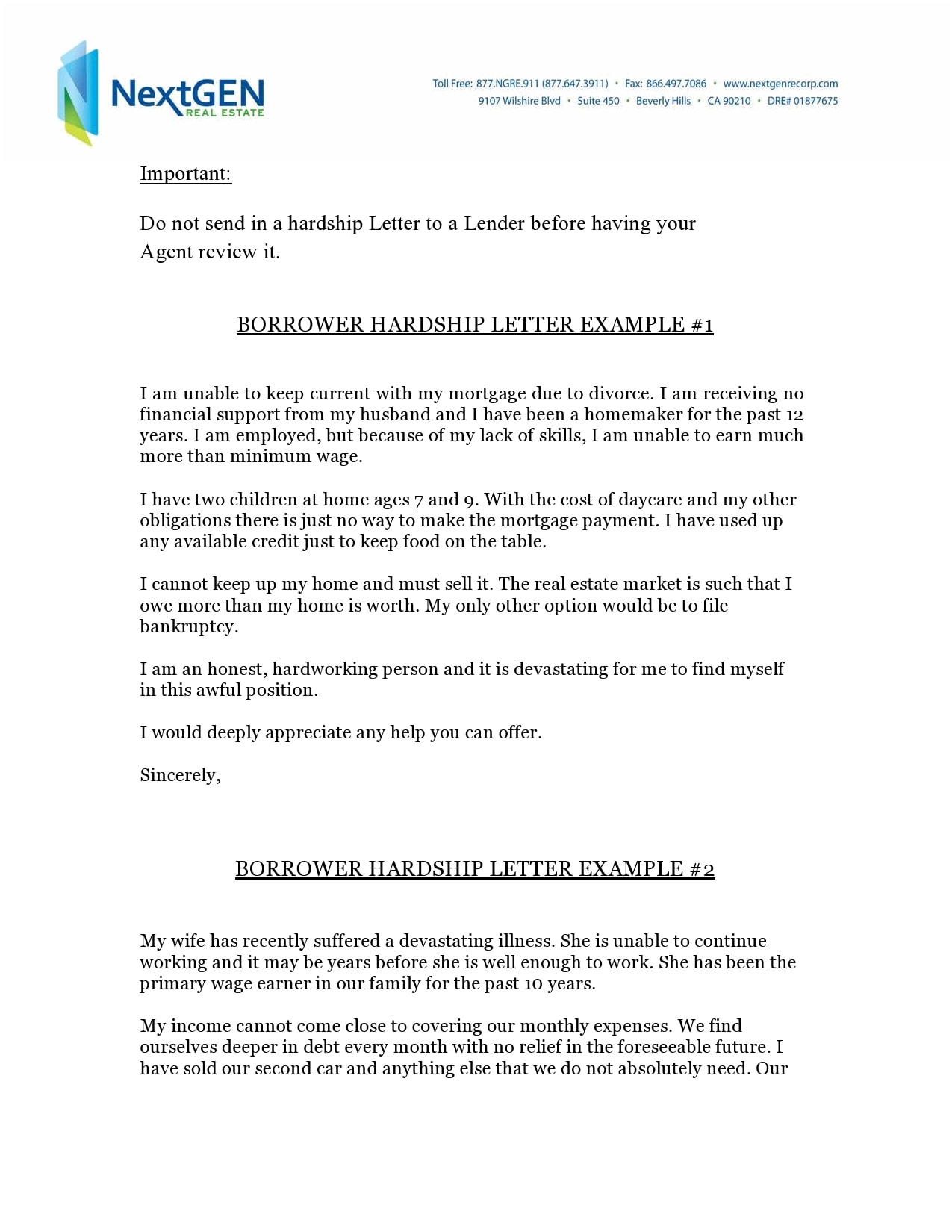

Whatever the reason for your hardship is, it’s very important to be both honest and open with your lenders. You have to prove to them that you’re willing to work together to find a solution with a reasonable request along with a commitment to pay back what you owe.

What points should you address?

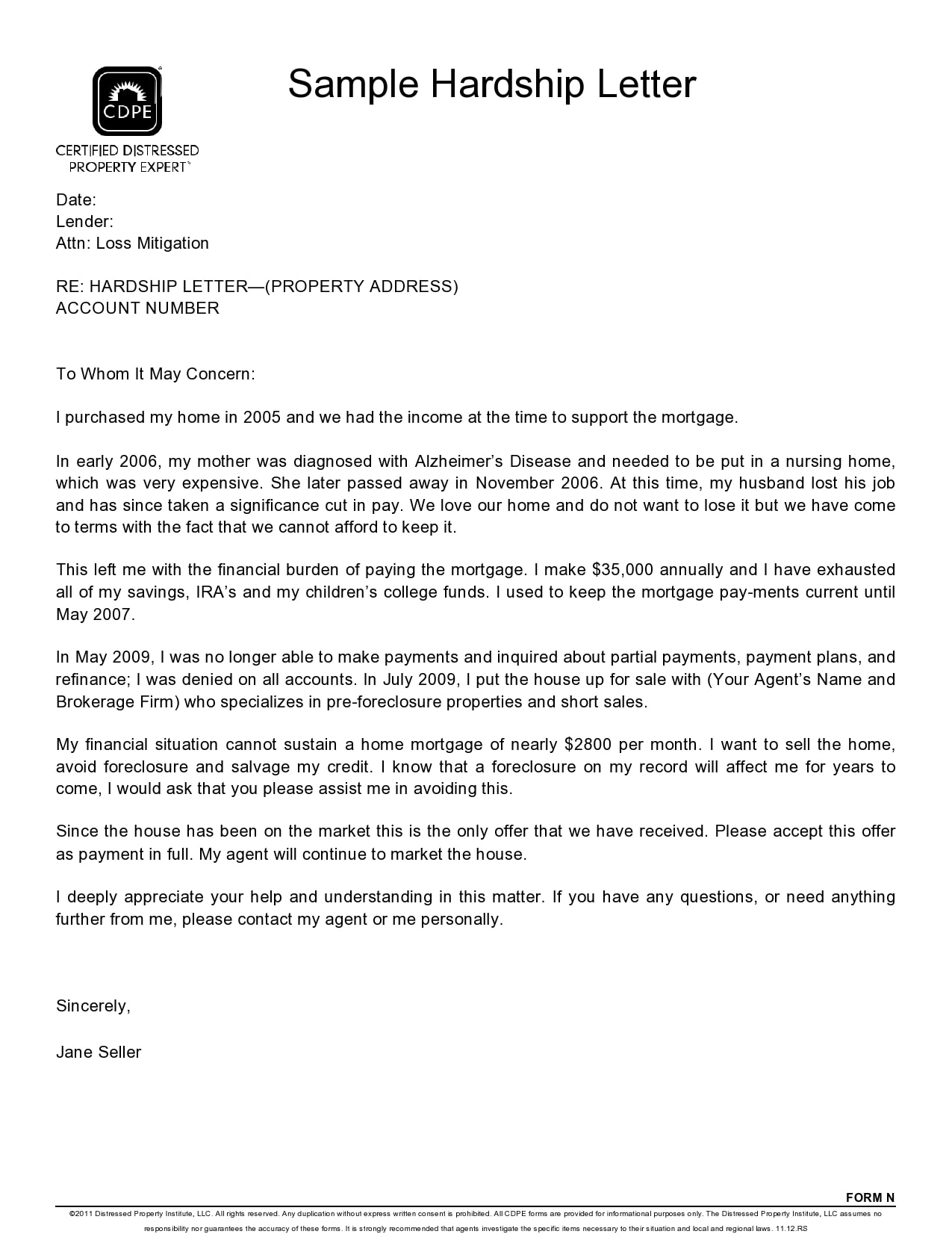

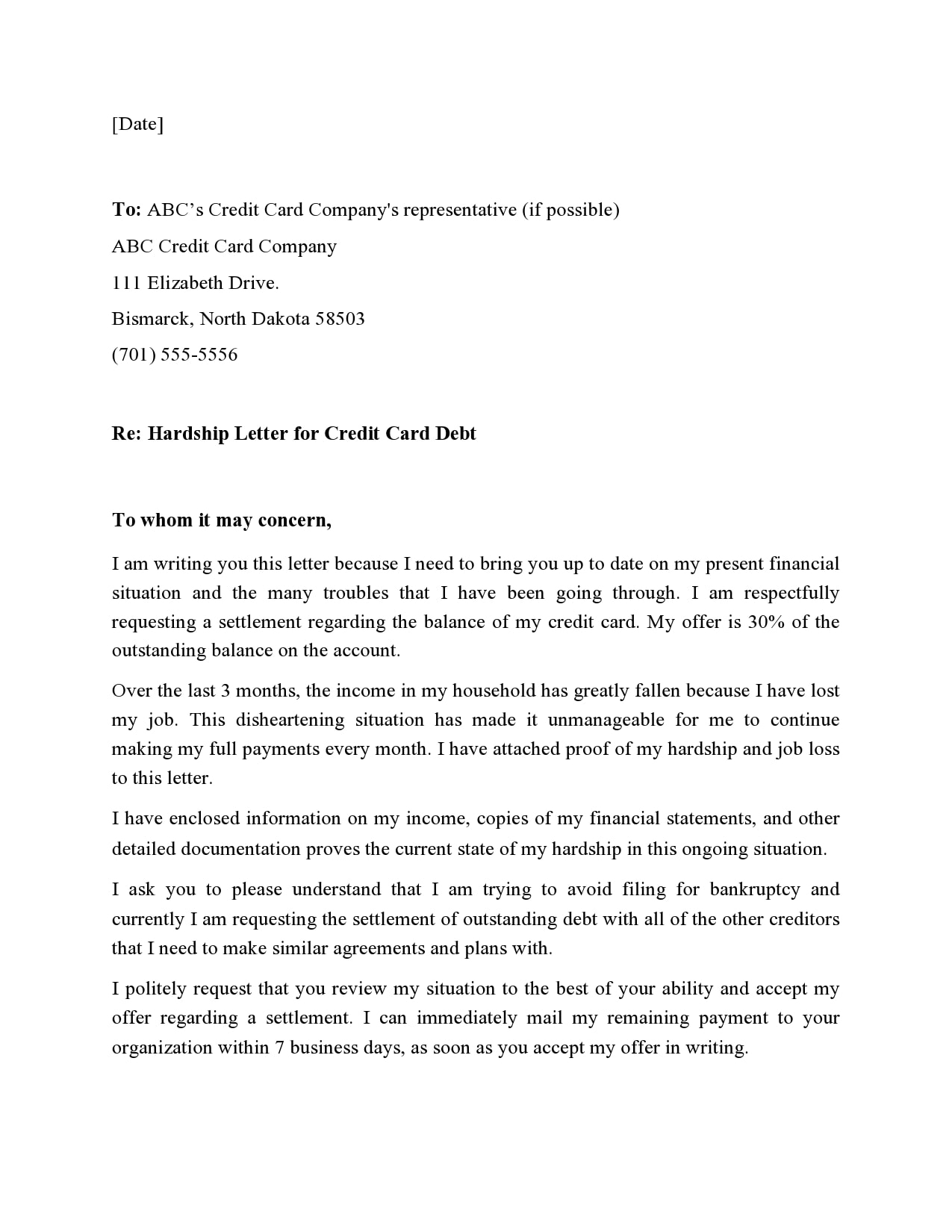

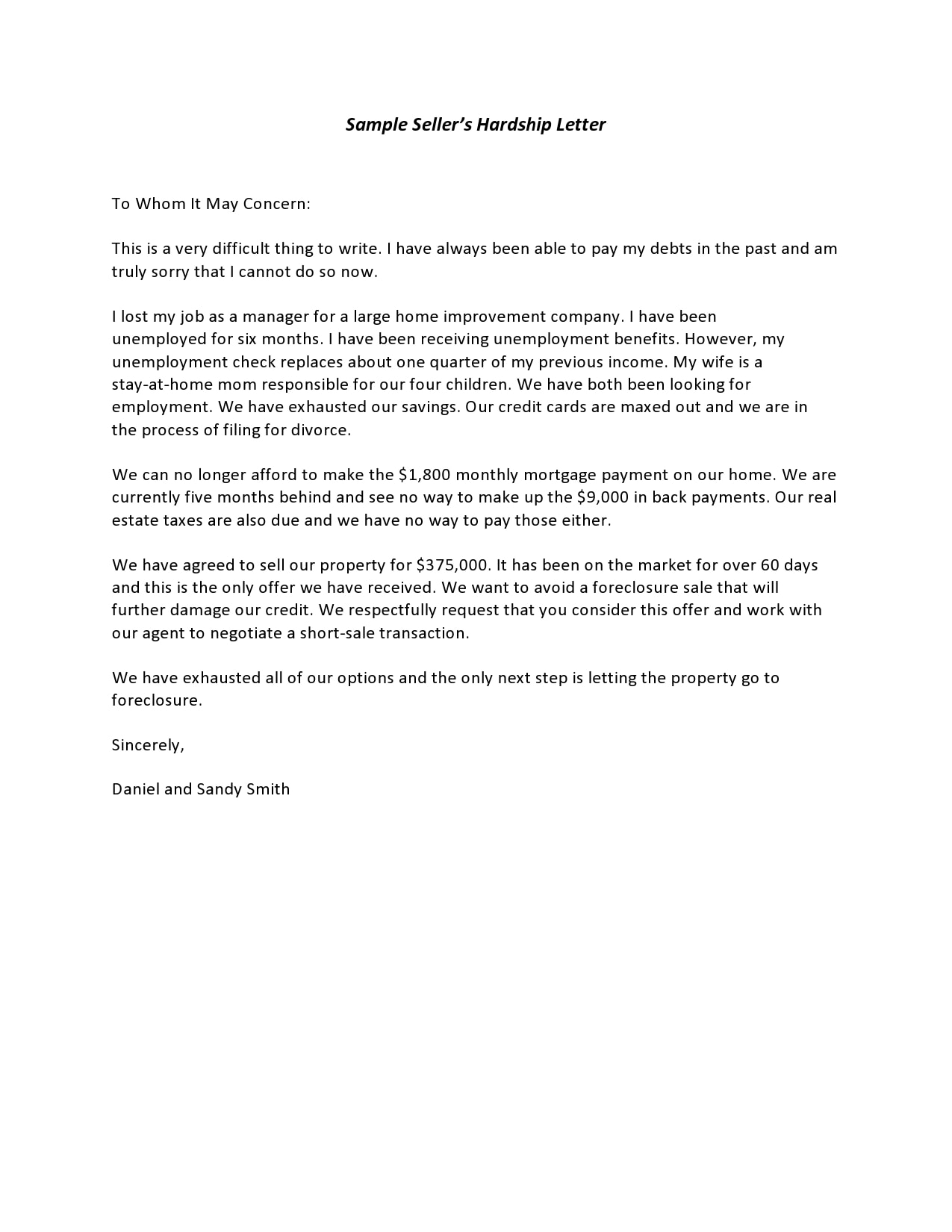

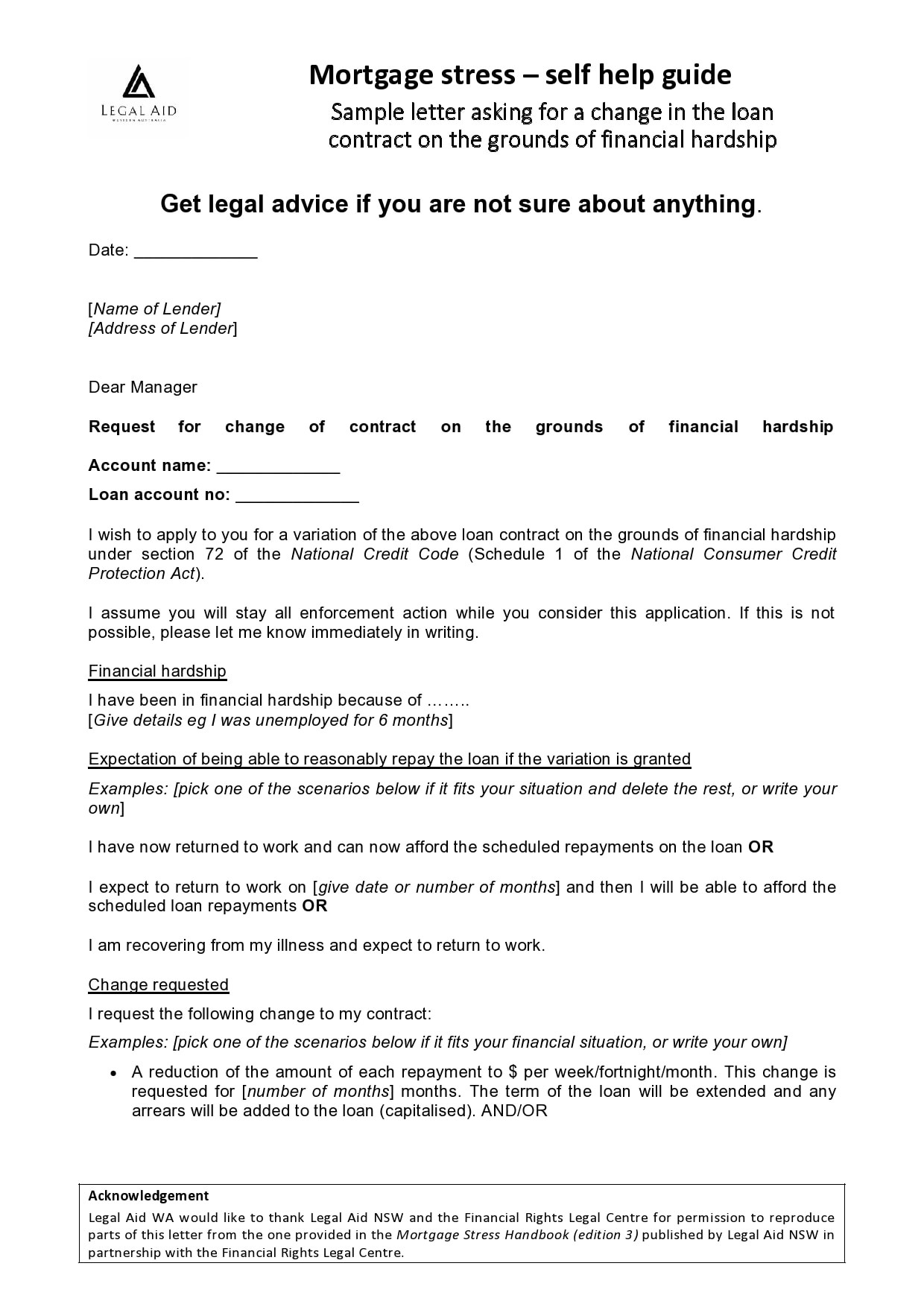

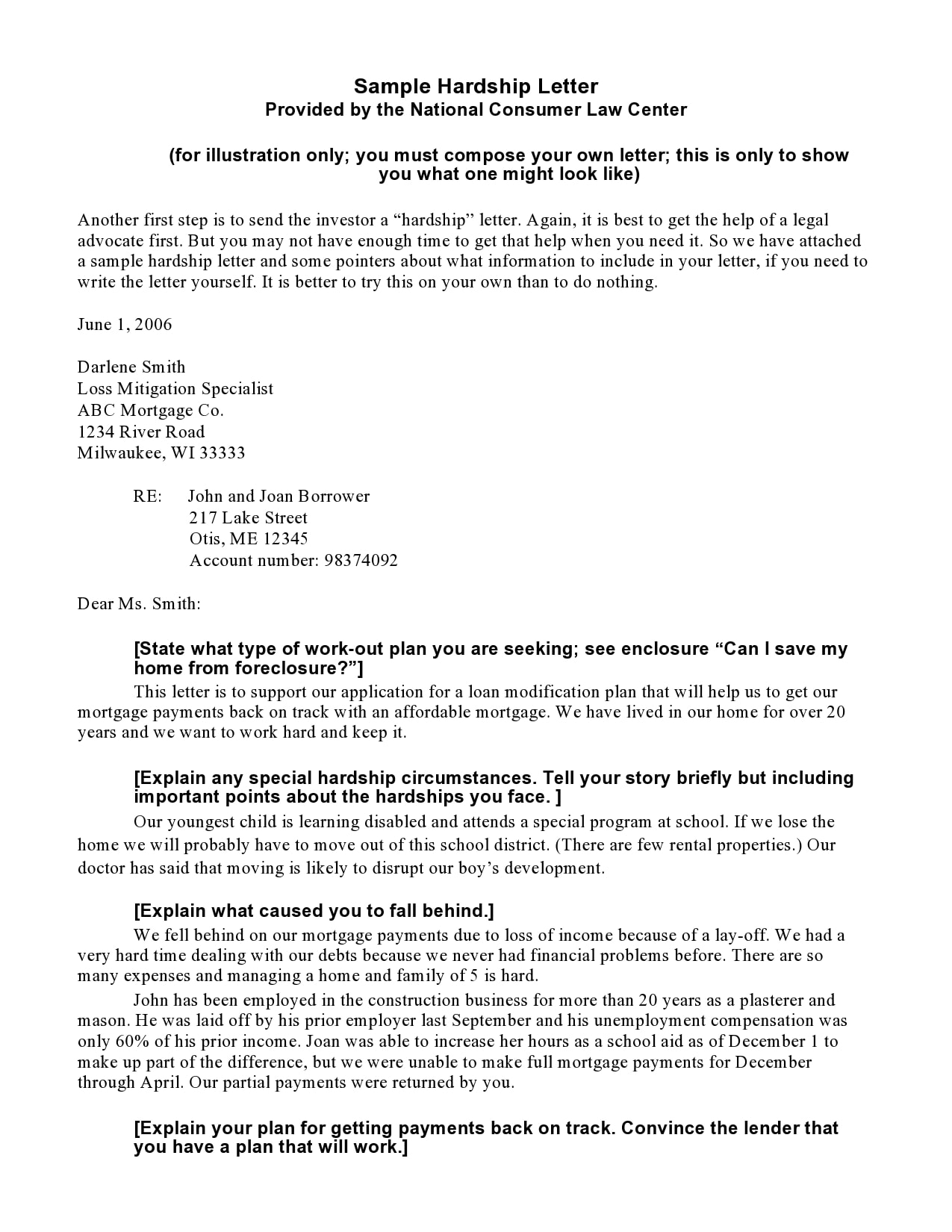

If the last resort for you to settle your debt is a short sale, you still need to send to your lender a financial hardship letter. Here, you will explain why you as the homeowner need to default on your mortgage and you need to sell your home for less than what it’s worth.

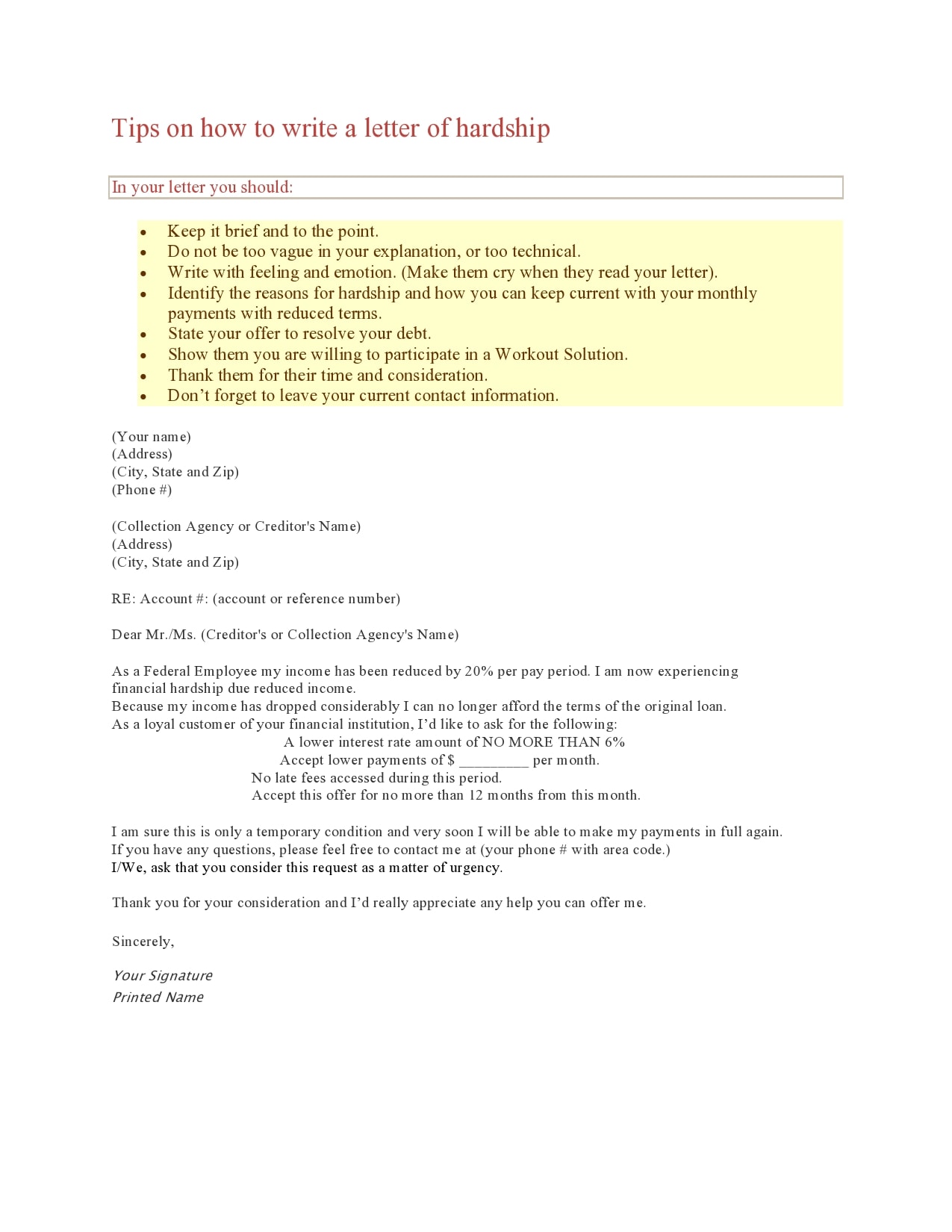

The most effective letters should read like an attorney’s pleading. You have to establish facts in such a way as to convince a lender to grant you a loan modification or a short sale rather than a foreclosure. In most cases, a hardship letter template should not exceed one page and should address these points:

- How your current financial situation occurred.

- What changes have happened in the real estate market since your initial financing.

- What you have done to improve your situation.

- Why you cannot improve your situation.

You have to prove to the lender that you don’t have the resources to pay the mortgage in full and you can prove this by providing them with supporting documents which might include tax returns, bank statements or pay stubs.

It is also a good move to provide the lender with comparable sales from an agent that can support your claim that you don’t have enough money to cover all of the costs.

Hardship Letter Templates

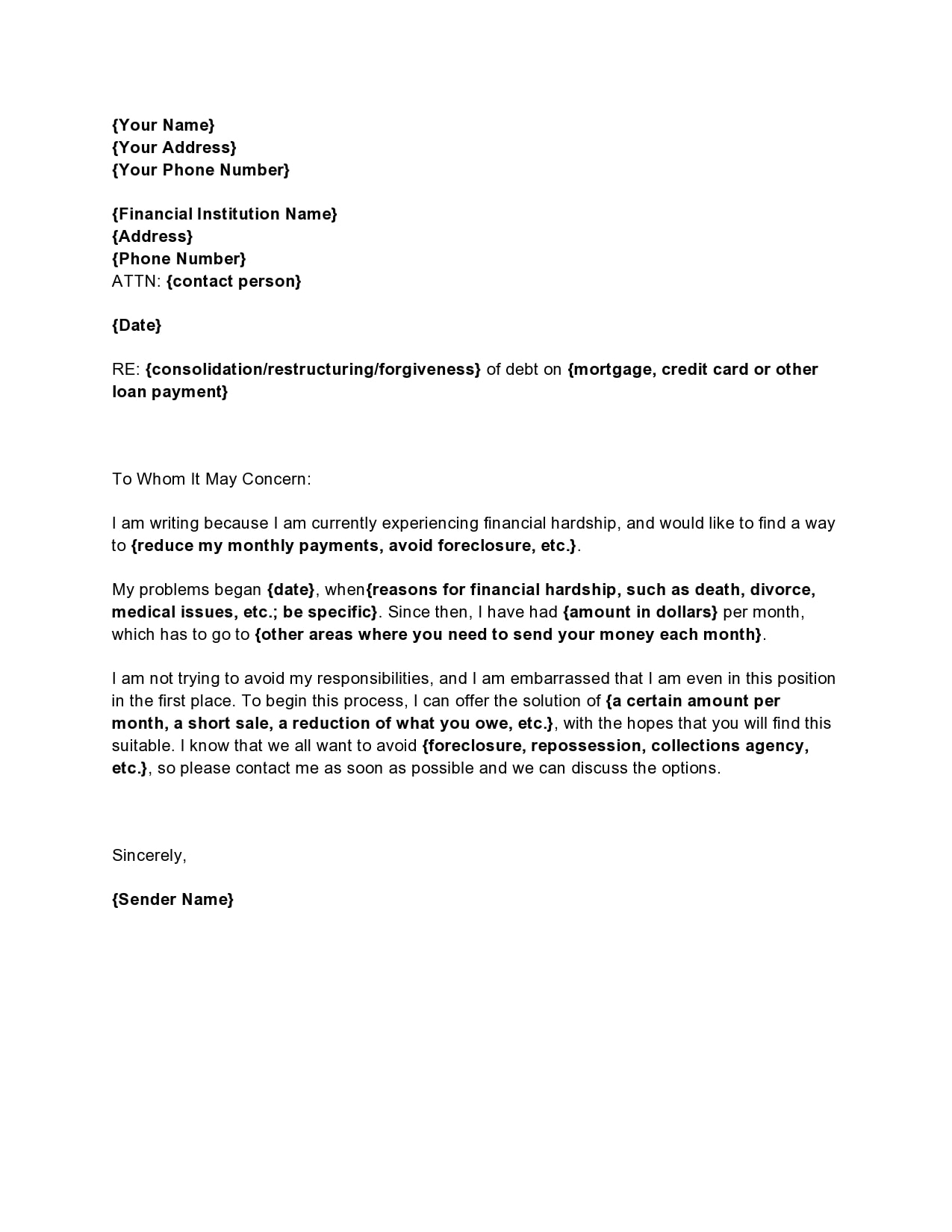

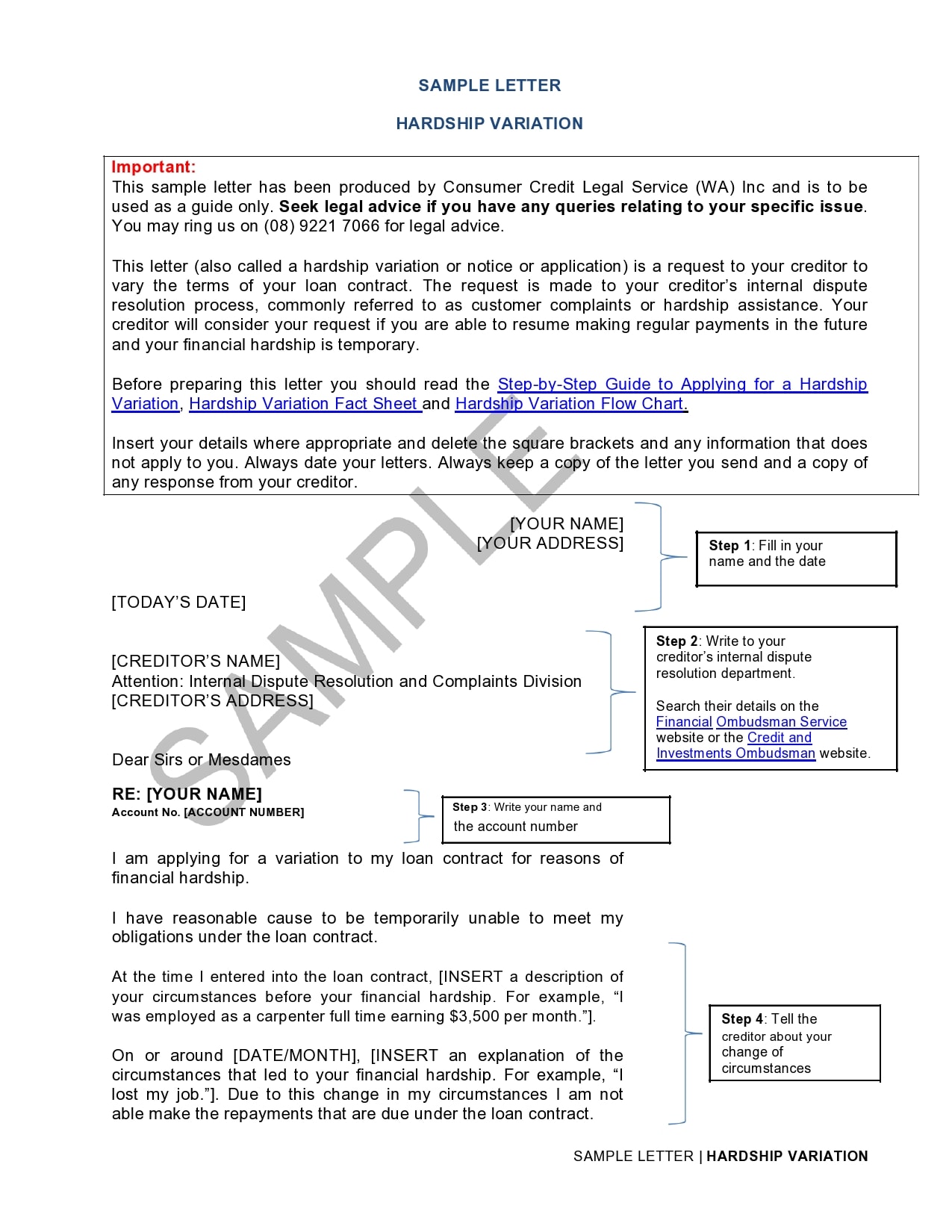

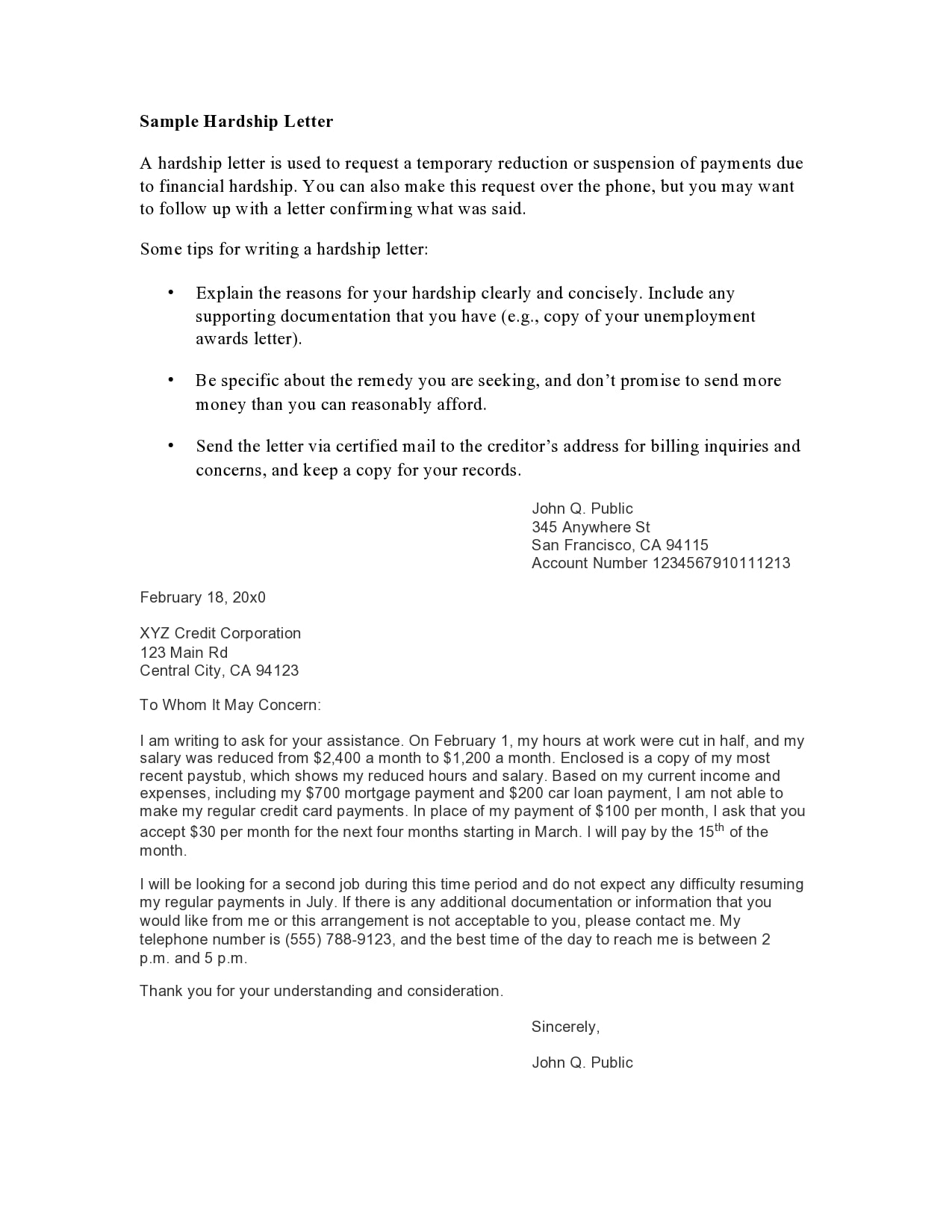

How do I write a financial hardship letter?

No matter what your specific situation is, you can follow these guidelines when drafting a financial hardship letter so any lender will take your request seriously:

- Keep your letter short

Your hardship letter template should be no more than 1-page long. You have to be both concise and straight to the point. Remember that a long letter might lessen the chances of your case getting approved as your reader will lose interest. - Personalize your letter

It would help a lot if you can personalize your letter too. You can do this by including the details about your real situation so the reader can empathize with you as a fellow human being. - Clearly state your problem

In a sentence or two, summarize the specific situation that has pushed you to compose the hardship letter sample. If you want too, you can provide additional details later on. - Provide enough information

Providing the reader with enough detailed information can help them understand your predicament. To prove this, you can attach supporting documents like bank statements, cash flow statements, income tax statements, letters, invoices, and more. - State your request

State exactly what you’re requesting from the reader in the subject line of and in the first paragraph too. Then you can reiterate your request in slightly different wording at the end of your letter. - Show gratitude and humility

You would only write this letter when you are in financial distress and it is your last resort. Avoid going into side issues or playing the blame game. For this letter, it’s not ethical. Show respectful and don’t forget to thank the reader in advance for considering your situation.

")