Once signed and verified, a personal loan template is a legally-binding document that establishes the terms and conditions of a personal loan. Considered as a contract, the borrower should abide by its governing laws, terms, and conditions. They must make their payments on time as per the terms of the contract.

Contents

Personal Loan Templates

What is a personal loan?

Simply put, a personal loan involves a specific amount of money borrowed by a person and it involves the use of a personal loan agreement template. It is the responsibility of the borrower to pay you back as the lender along with the agreed-upon interest rate.

If you agree to give a personal loan to someone, you must create a personal loan template for the agreement. Then you can think about the type of personal loan you will agree too:

- Co-Sign

When the borrower has no credit or poor credit and will need another person to assume liability in case the borrower can’t pay. - Fixed-Rate

Here, the interest rate won’t change during the whole course of the loan’s repayment period. - Secured

The borrower must put up collateral in case of default. The most common collateral examples include a second mortgage on their home or their car. - Unsecured

Although the borrower isn’t required to put up collateral as part of the agreement, their personal assets might still get confiscated legally in case of default. - Variable Rate

This involves a third-party that sets the interest rates.

Personal Loan Agreements

What are the 3 parts of a loan?

It’s important for the borrower to understand the fundamental principles of loaning before making any decisions. As a lender, you should also familiarize yourself with these principles. When you’re creating a personal loan template, consider these 3 main parts of a loan:

- Interest Rate

This is the amount that you charge for borrowing your money. Usually, this is a small percentage of the loan amount. There are two types of interest rates:

Fixed rates that don’t change.

Variable rates that may change throughout the course of the repayment period. The change is usually based on standard market rates. - Security Component

This is in reference to the assets – or collateral – that the borrower puts up to guarantee the loan. The two types of loans involved here are:

A secured loan where the borrower guarantees that you will get repaid one way or another by offering you a claim on an asset that the borrower owns. Should the borrower fail to pay the loan, you can take possession of the collateral to get back your investment. This type of loan guarantees you a great sense of security and allows you to charge a lower interest rate.

An unsecured loan where you won’t require the borrower to put up any collateral. As such, you won’t have protection if the borrower defaults on the loan. For this reason, unsecured loans typically have high-interest rates compared to secured loans. - Term

In a personal loan contract, this refers to the amount of time that the borrower needs to pay back the loan. The most common term is between 1 and 5 years. Longer terms mean higher interest rates.

The term refers to the maximum amount of time that the borrower has to pay back the loan. But loans can always get paid off before the agreed-upon term.

Can you give someone a personal loan?

Yes, you can give someone a personal loan, although that decision depends on you. But before you create your personal loan template, may want to ask the following questions to the borrower:

- What do you need the money for?

You have the right to know for what purpose the borrower needs the money. If you believe the reason isn’t adequate, then it’s best to refer the borrower to the nearest lending institution instead. - How long will you take to pay the loan back?

If the loan is just a necessity until the borrower’s next paycheck, you might feel comfortable charging zero-interest. No need for terms or a personal loan form. A mere handshake can close the deal. But if the loan involves a significant amount or the borrower needs months to pay it off, then you should create a written agreement. - What is your current financial situation?

As the lender, you’re responsible to find out if the borrower is in an adequate financial situation before agreeing to the loan. The situation may be an awkward one, but remember that the borrower approached you for the money – not the other way around.

Be as practical as possible and think just like a lending institution. If the situation is too dire, don’t agree to the loan.

Personal Loan Contracts

How do I write a personal loan agreement?

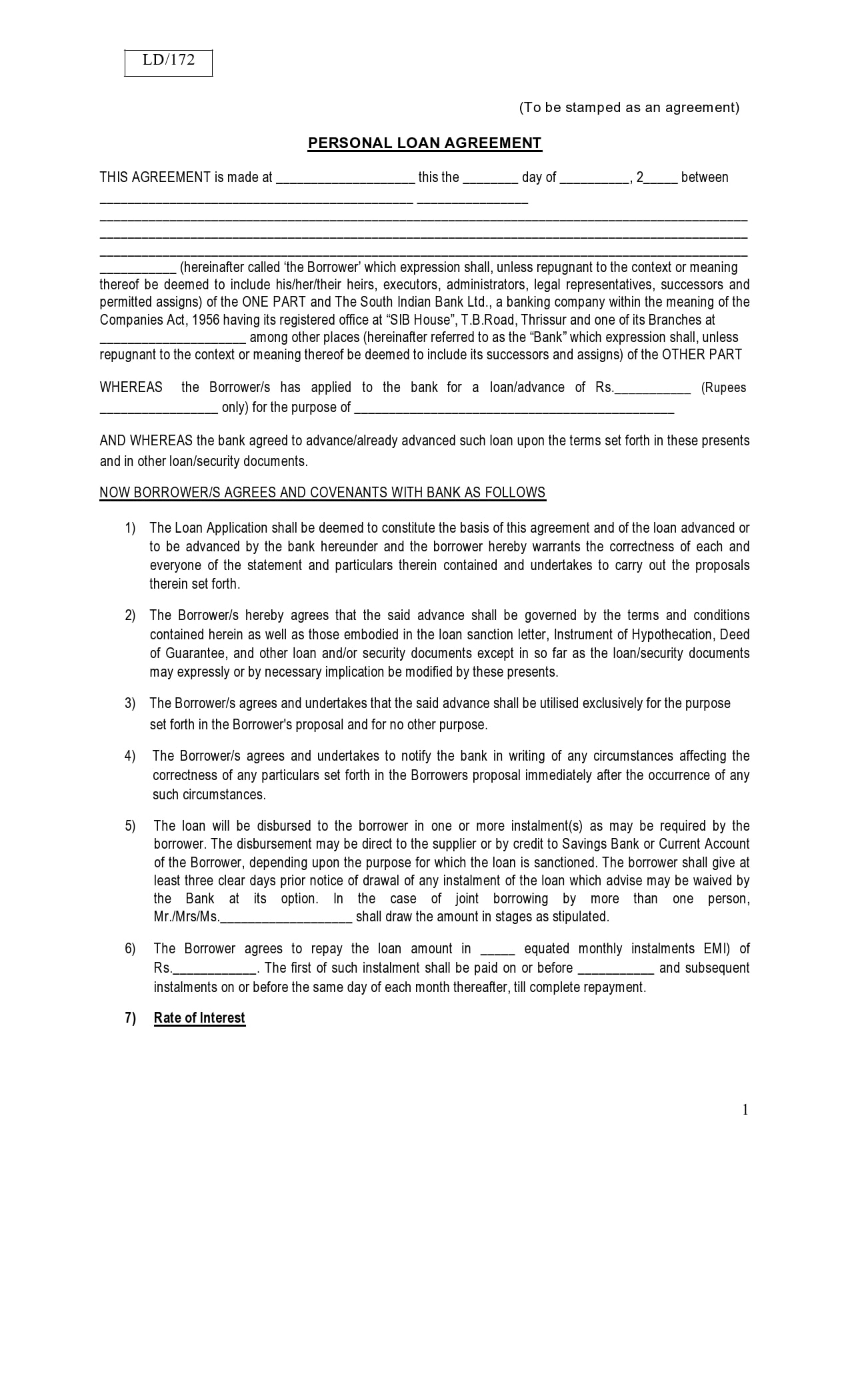

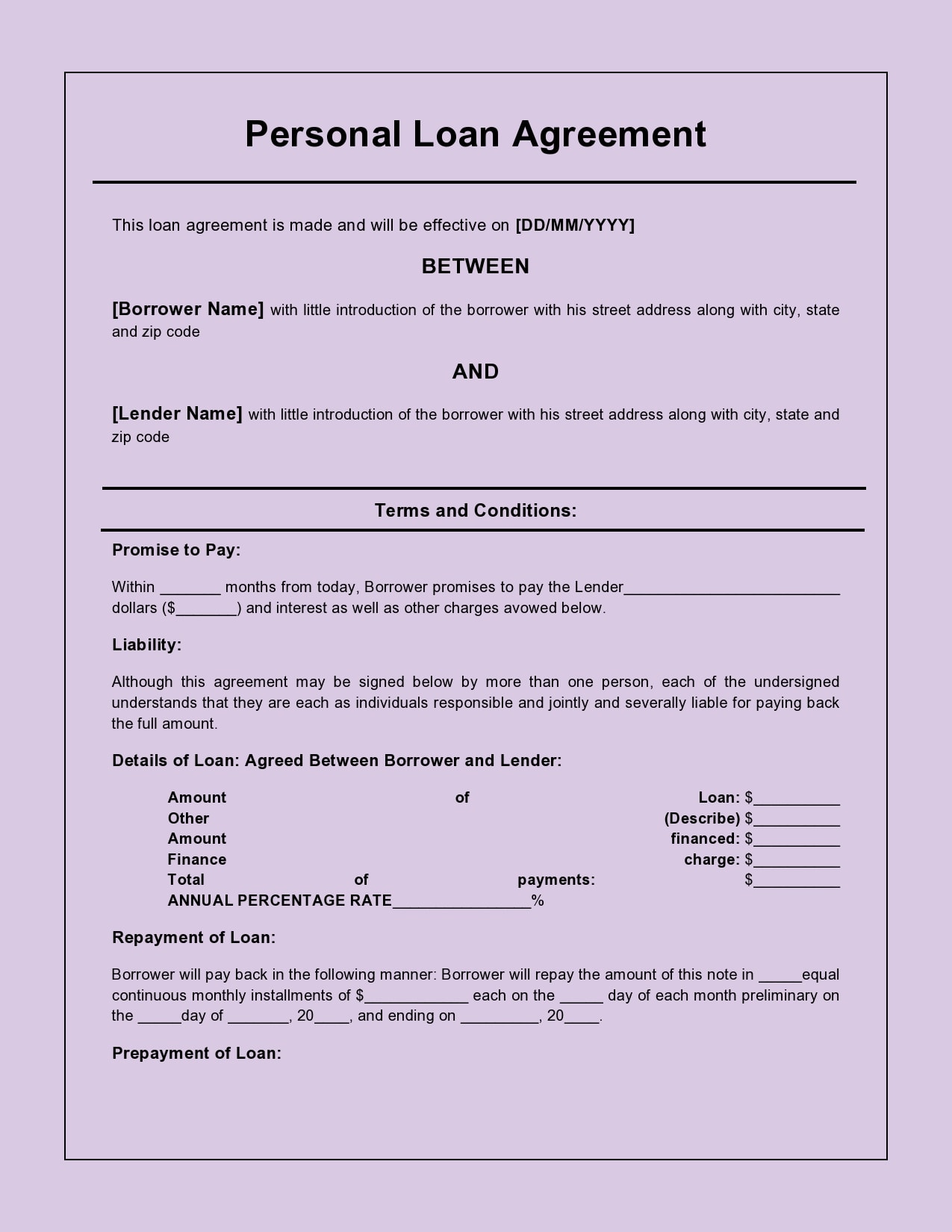

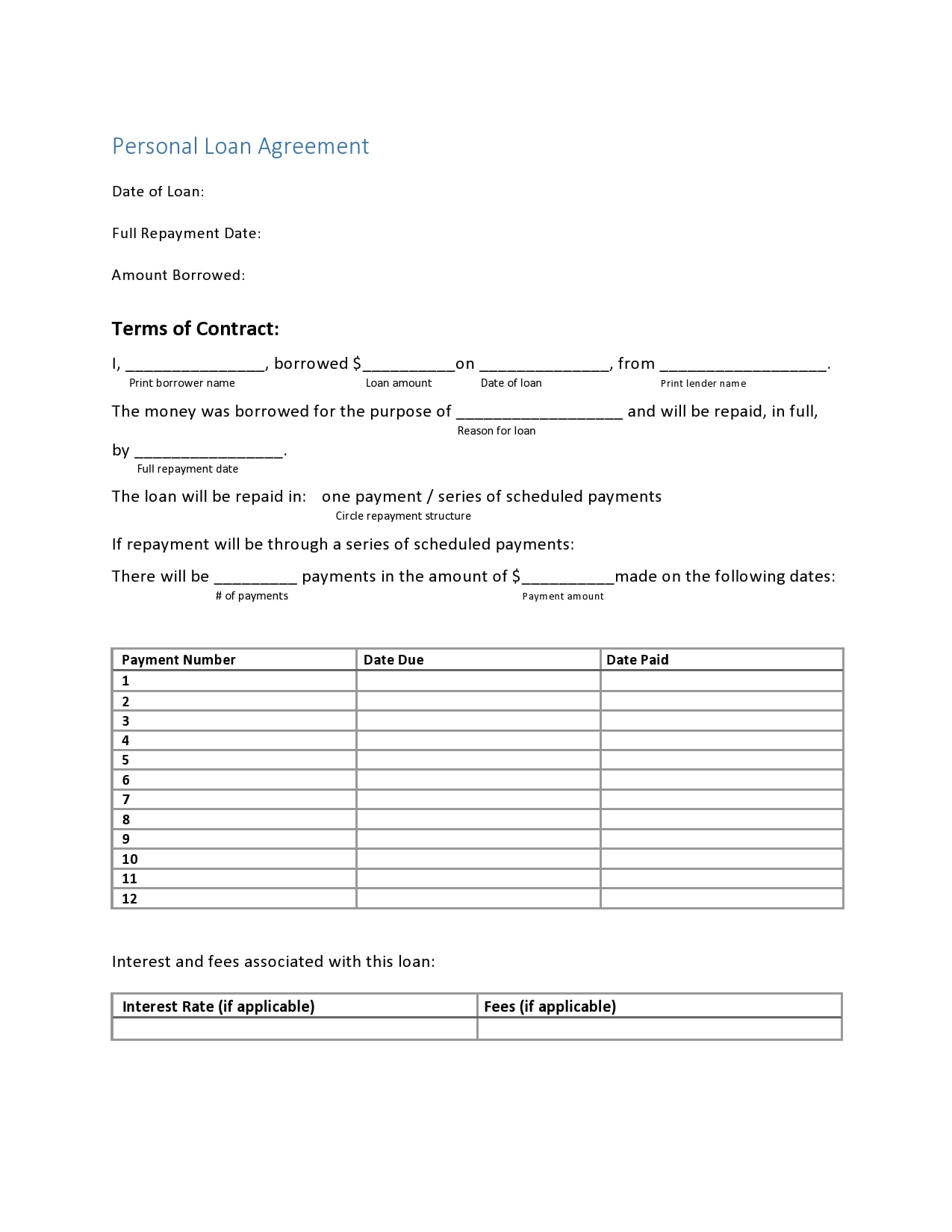

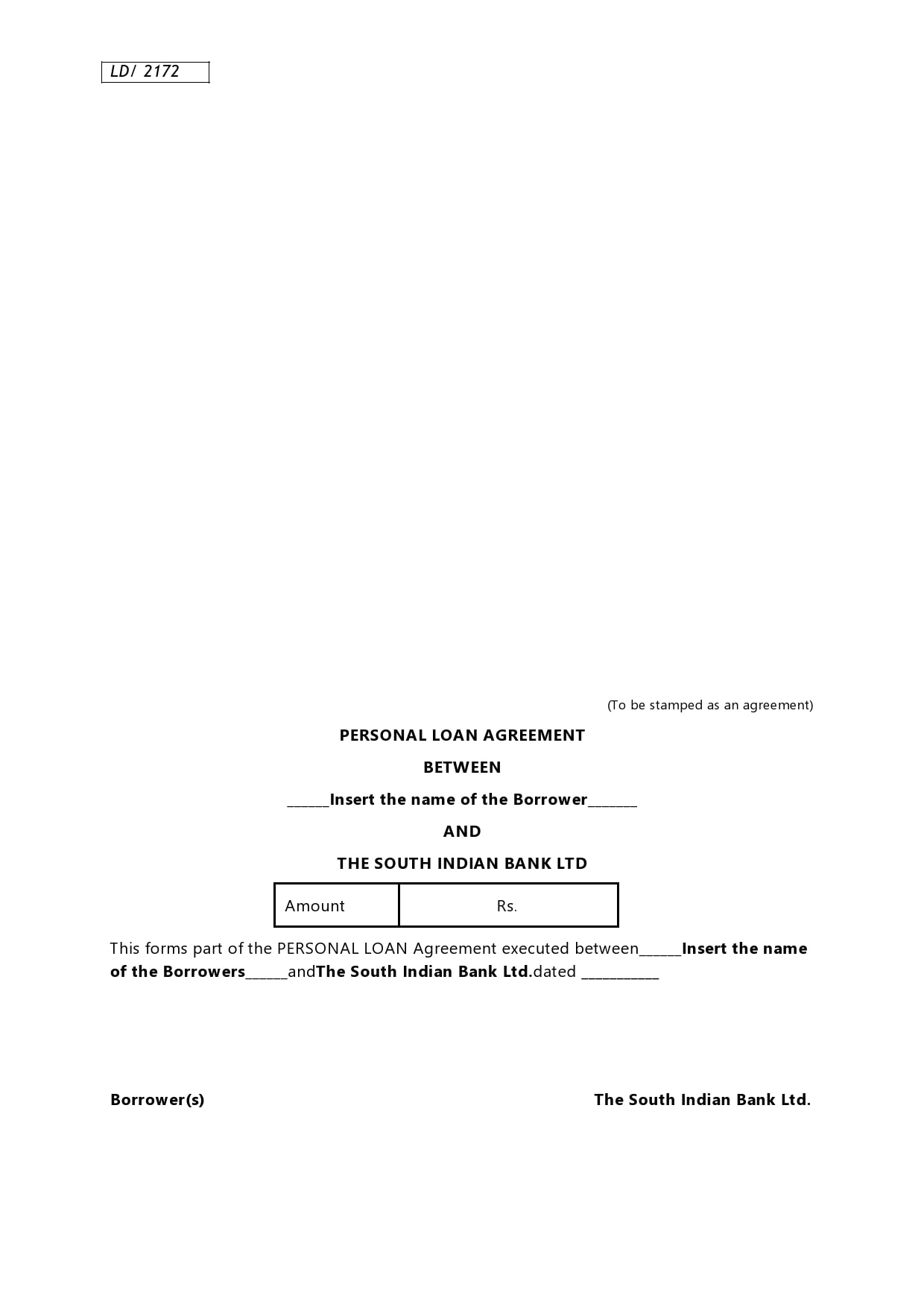

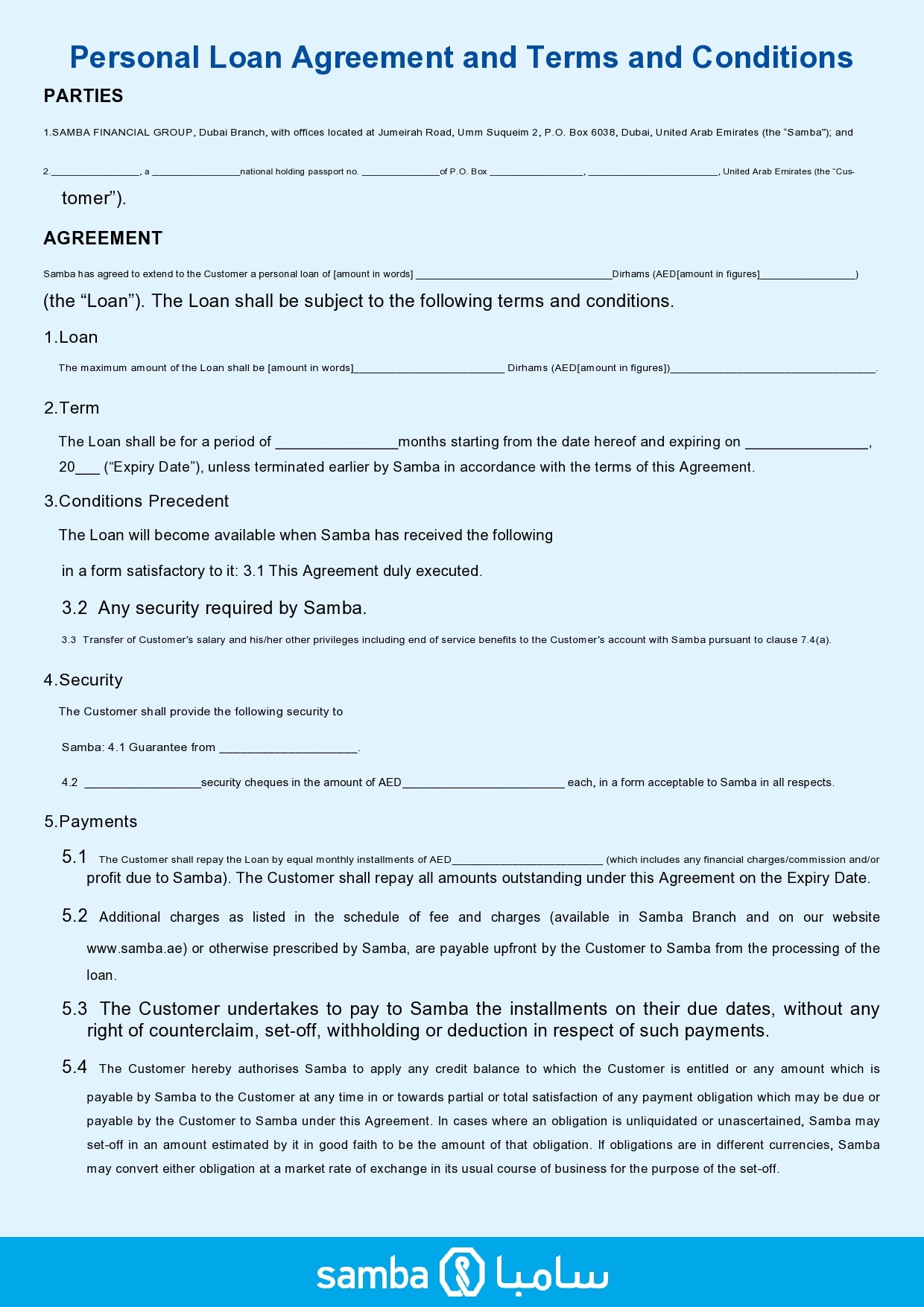

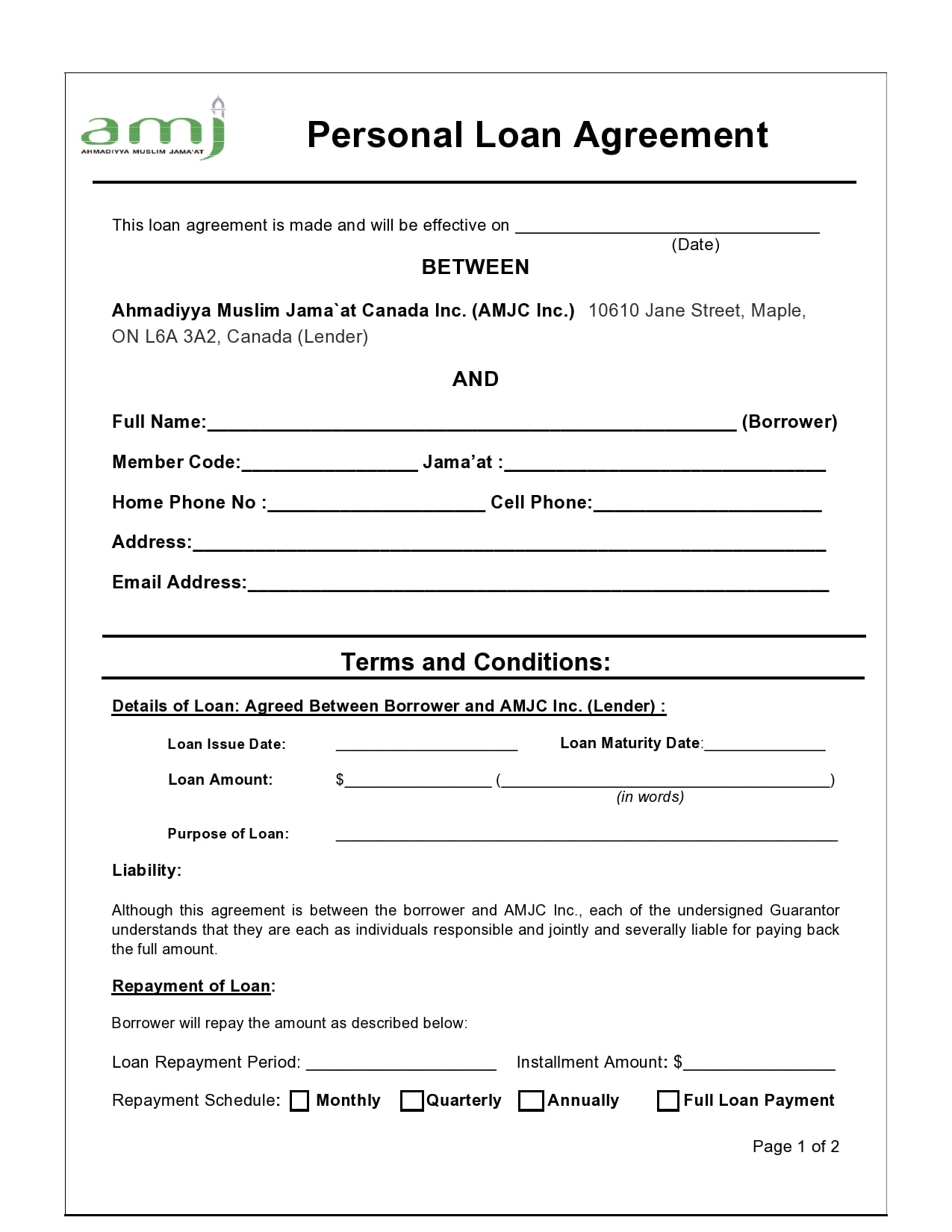

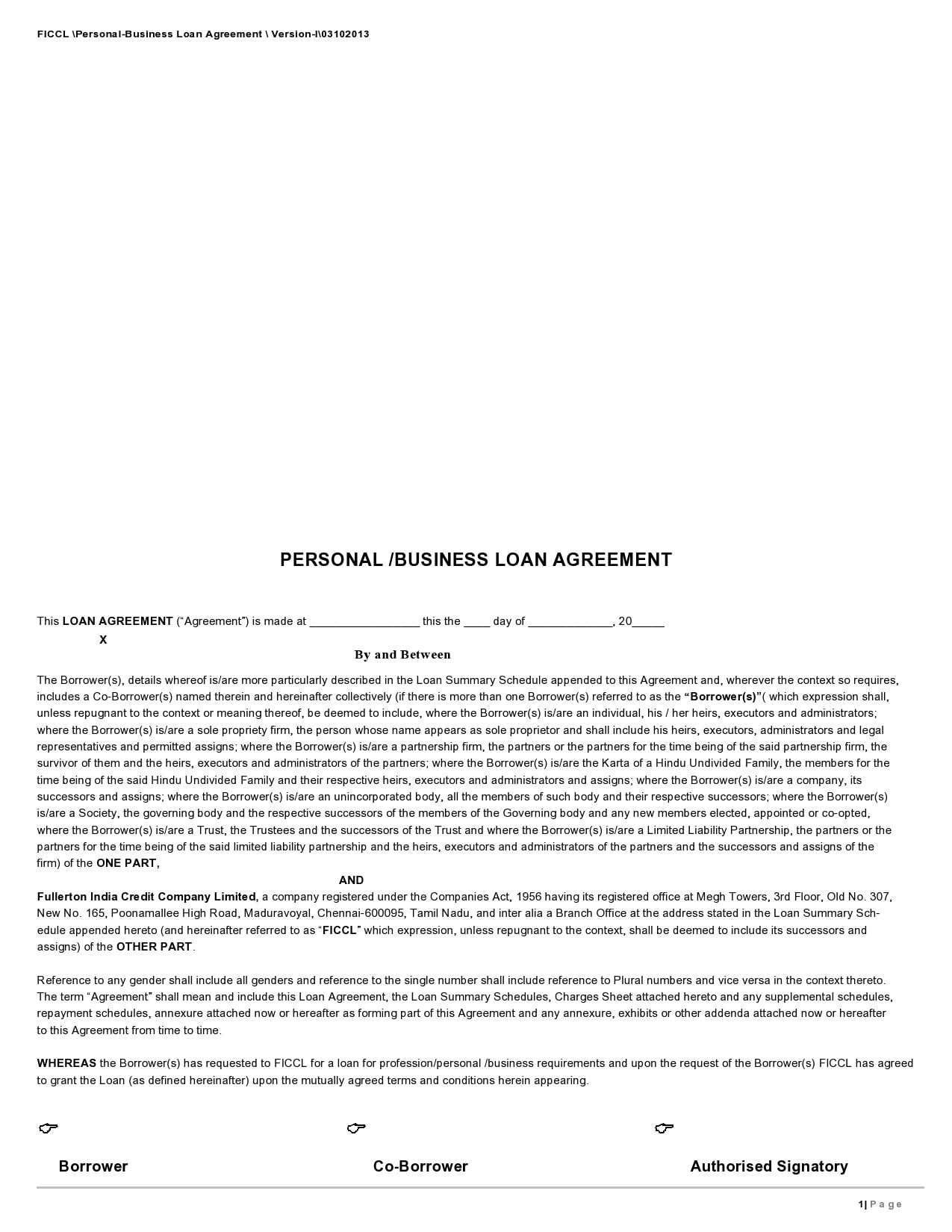

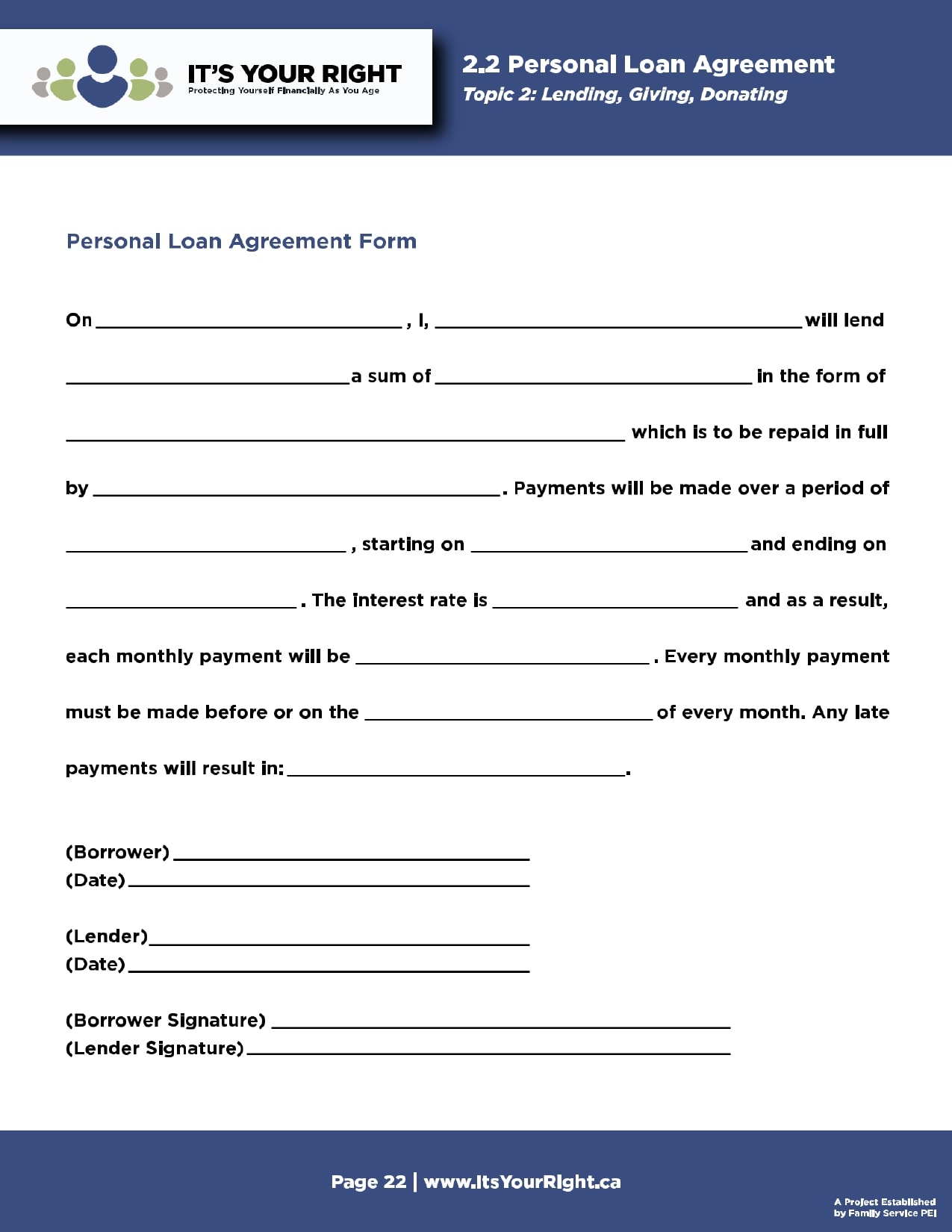

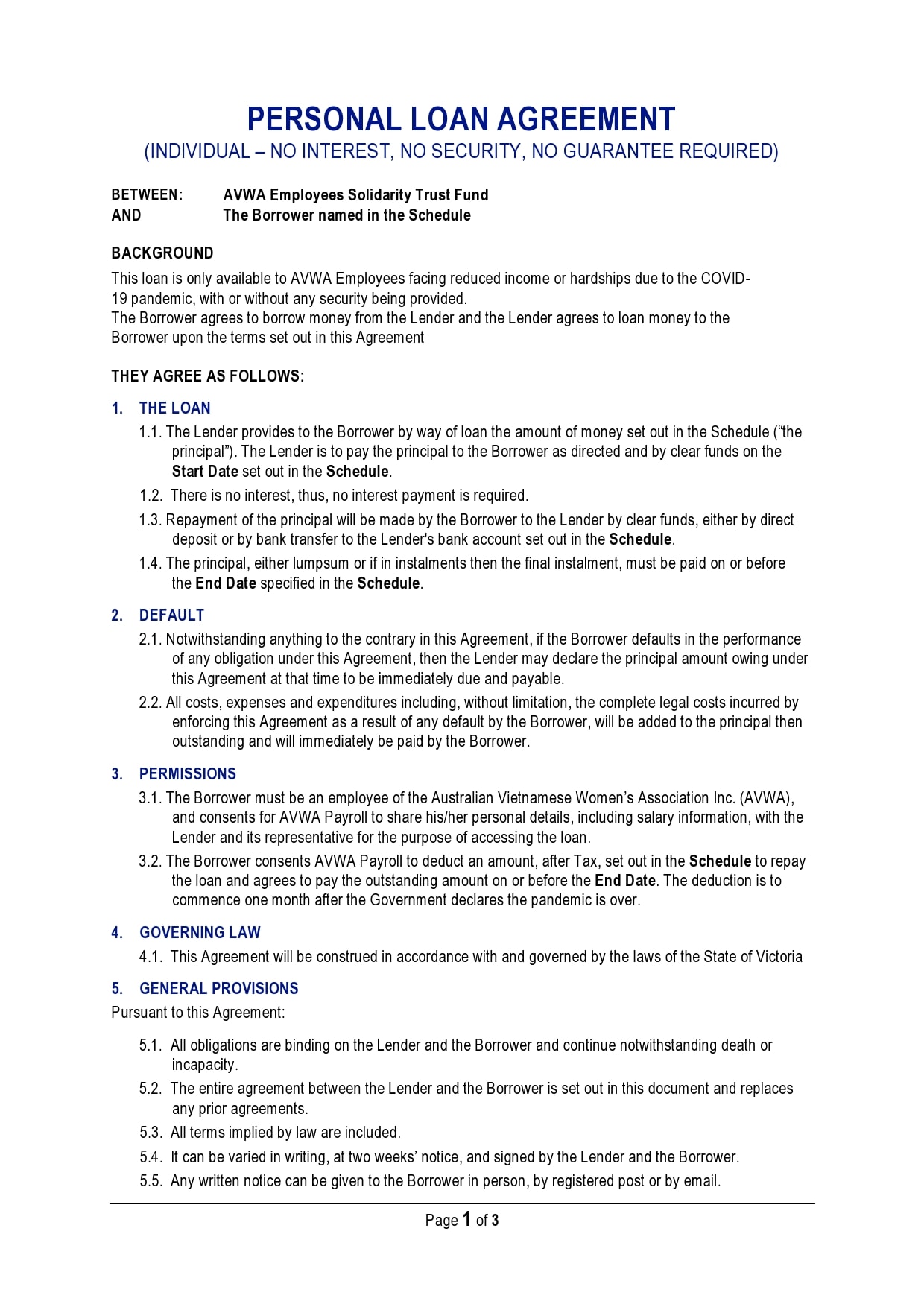

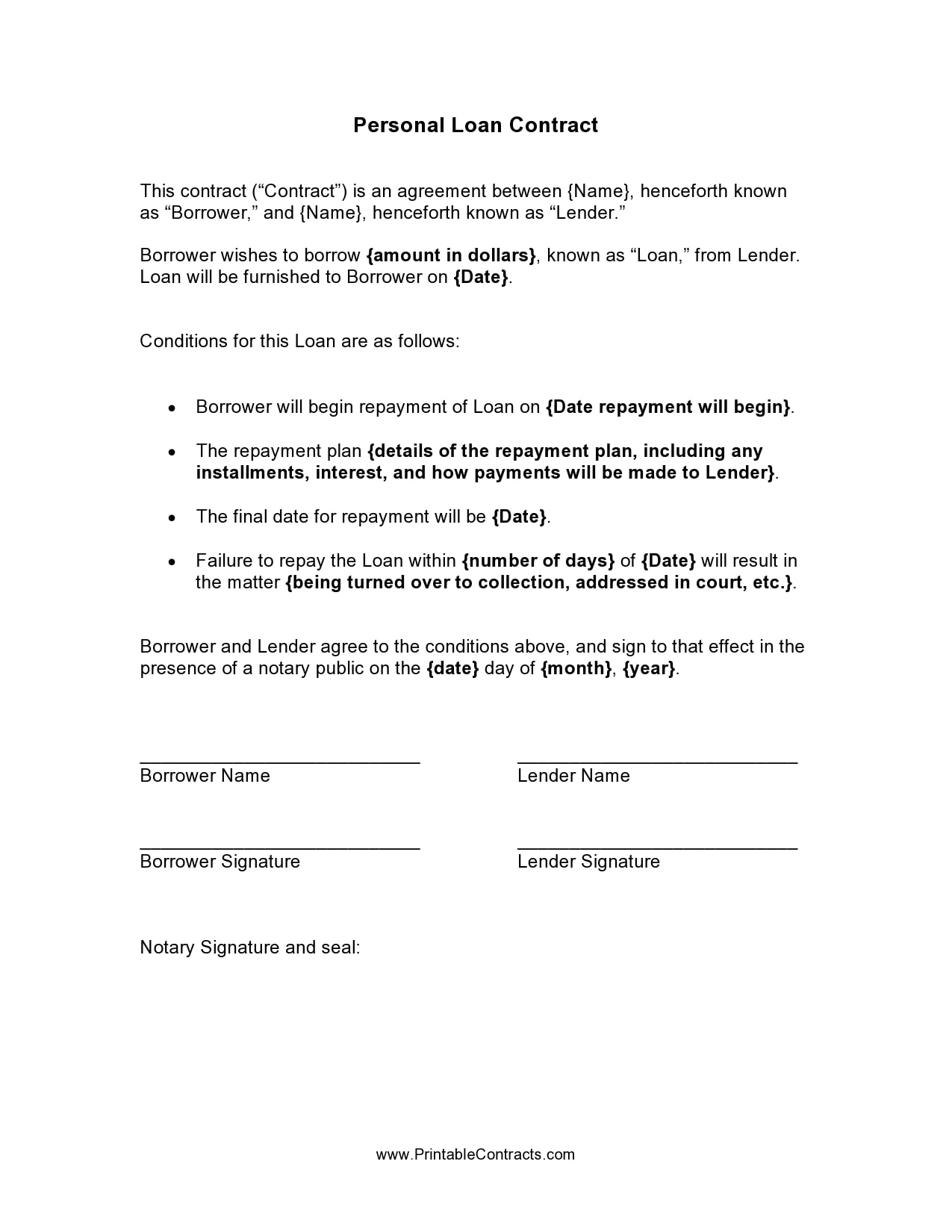

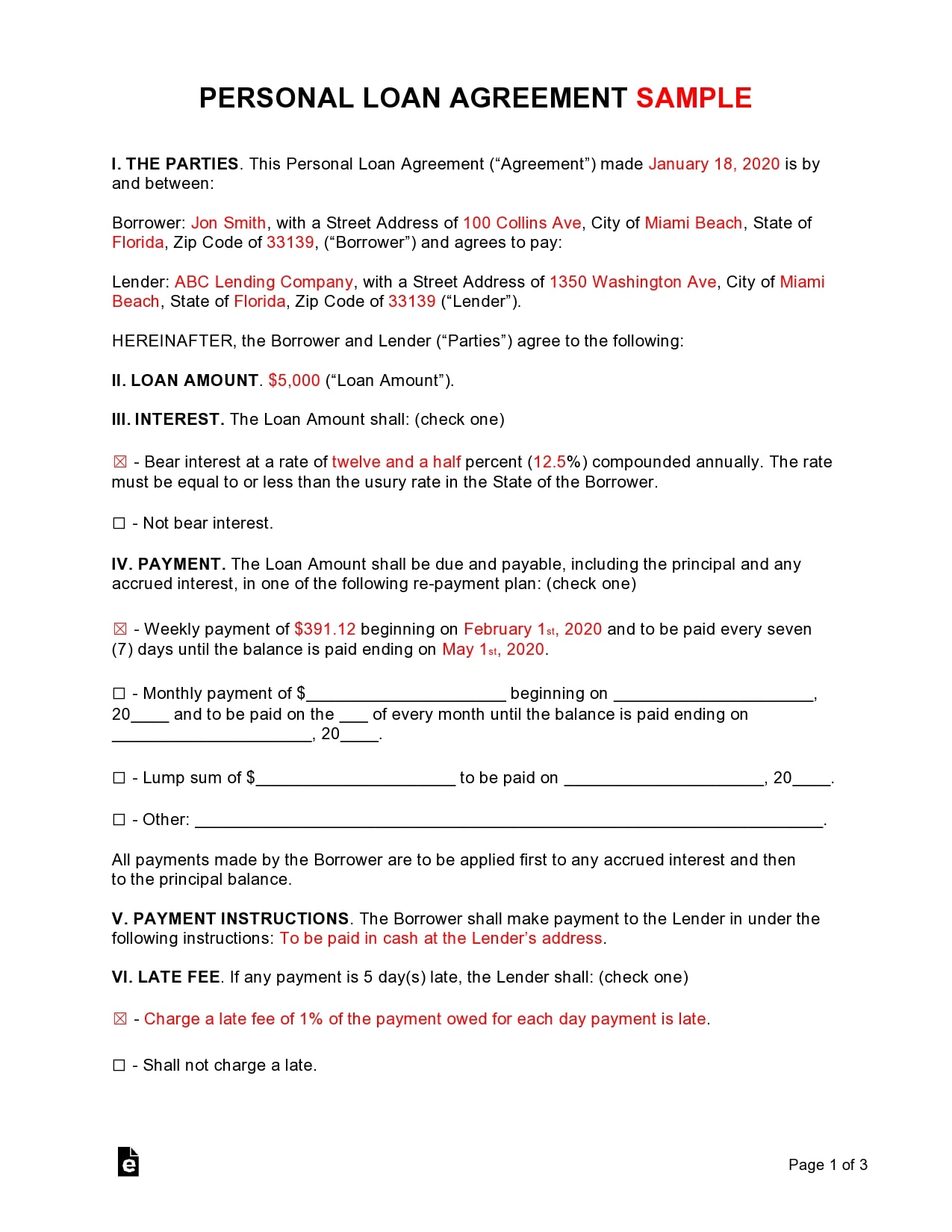

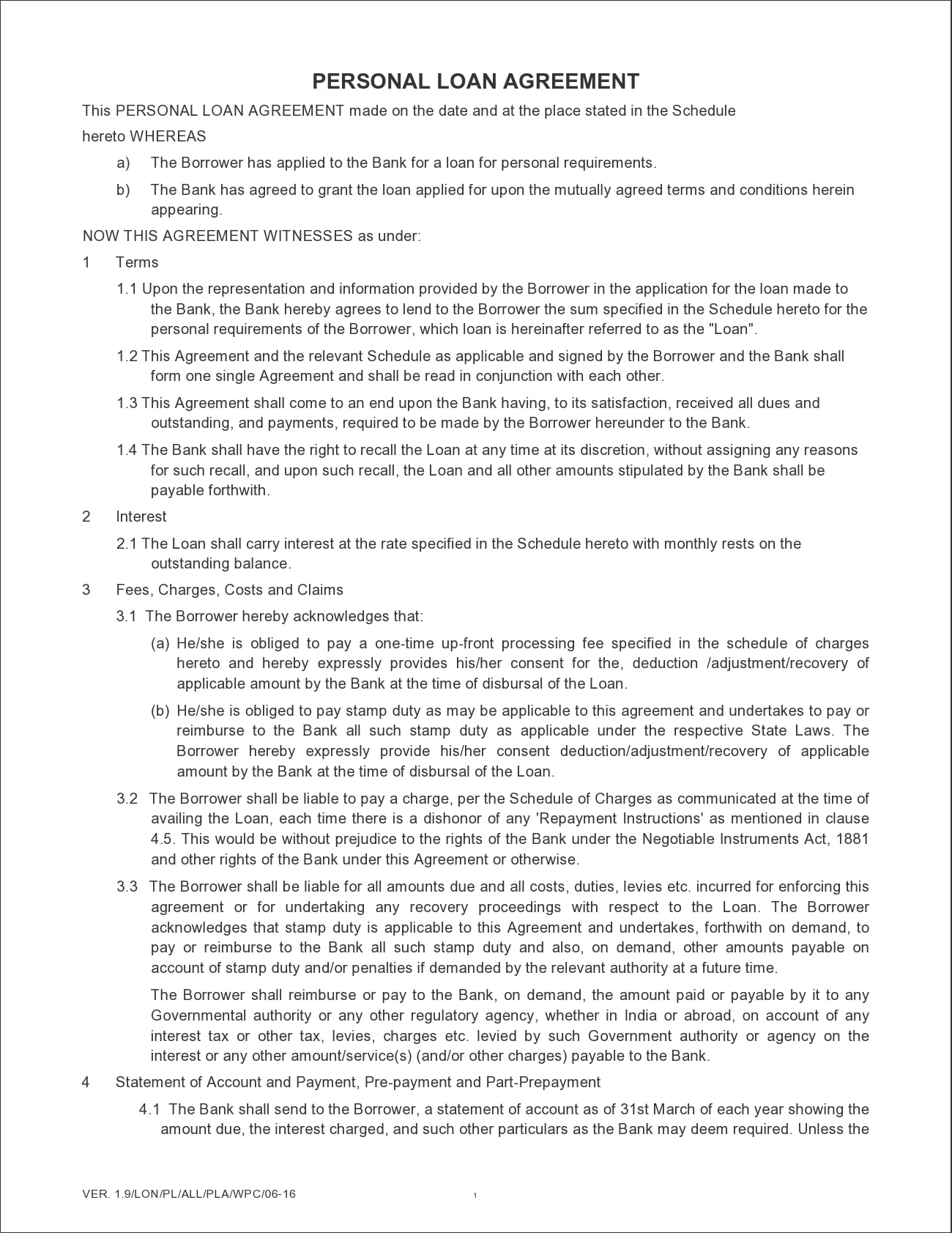

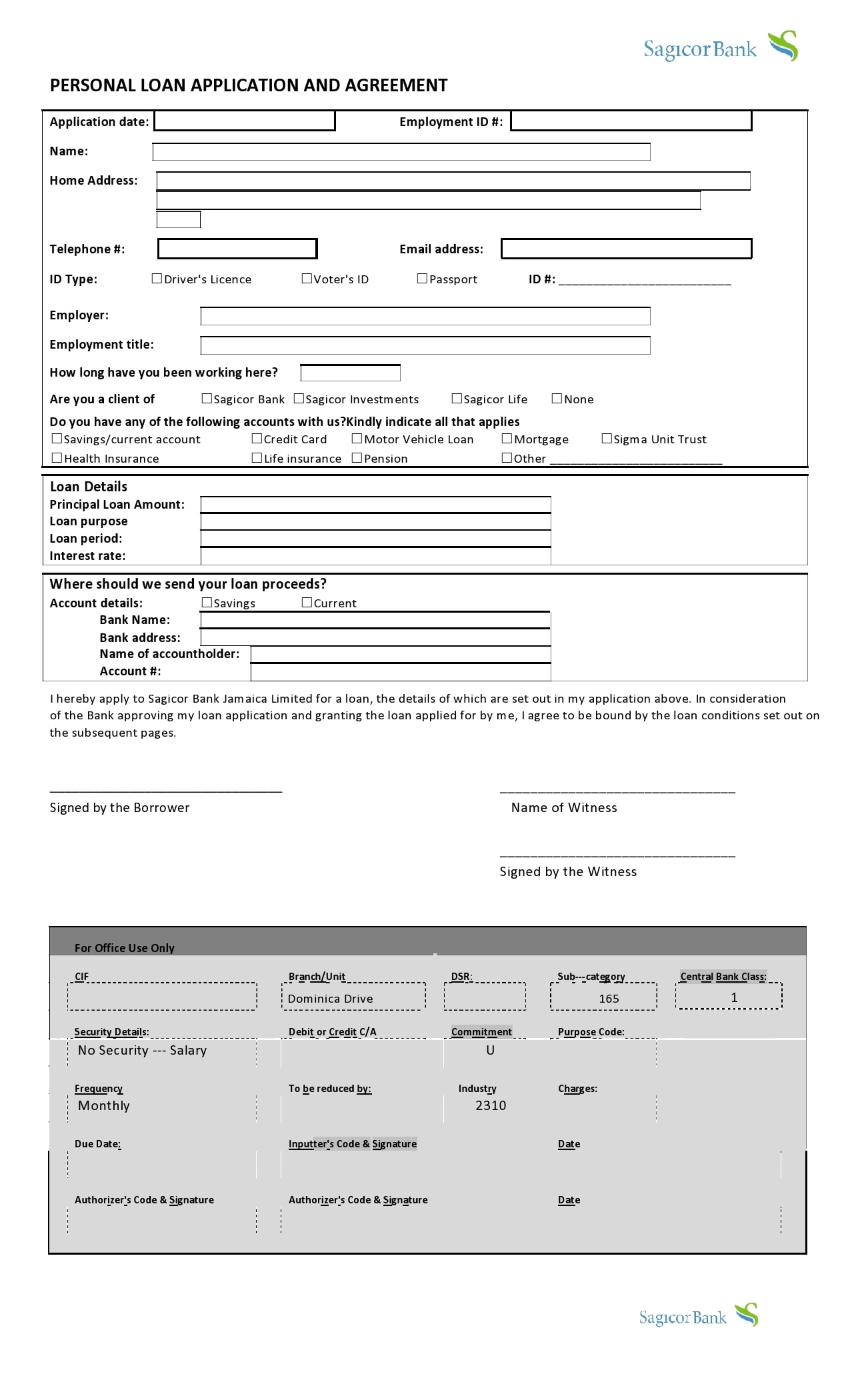

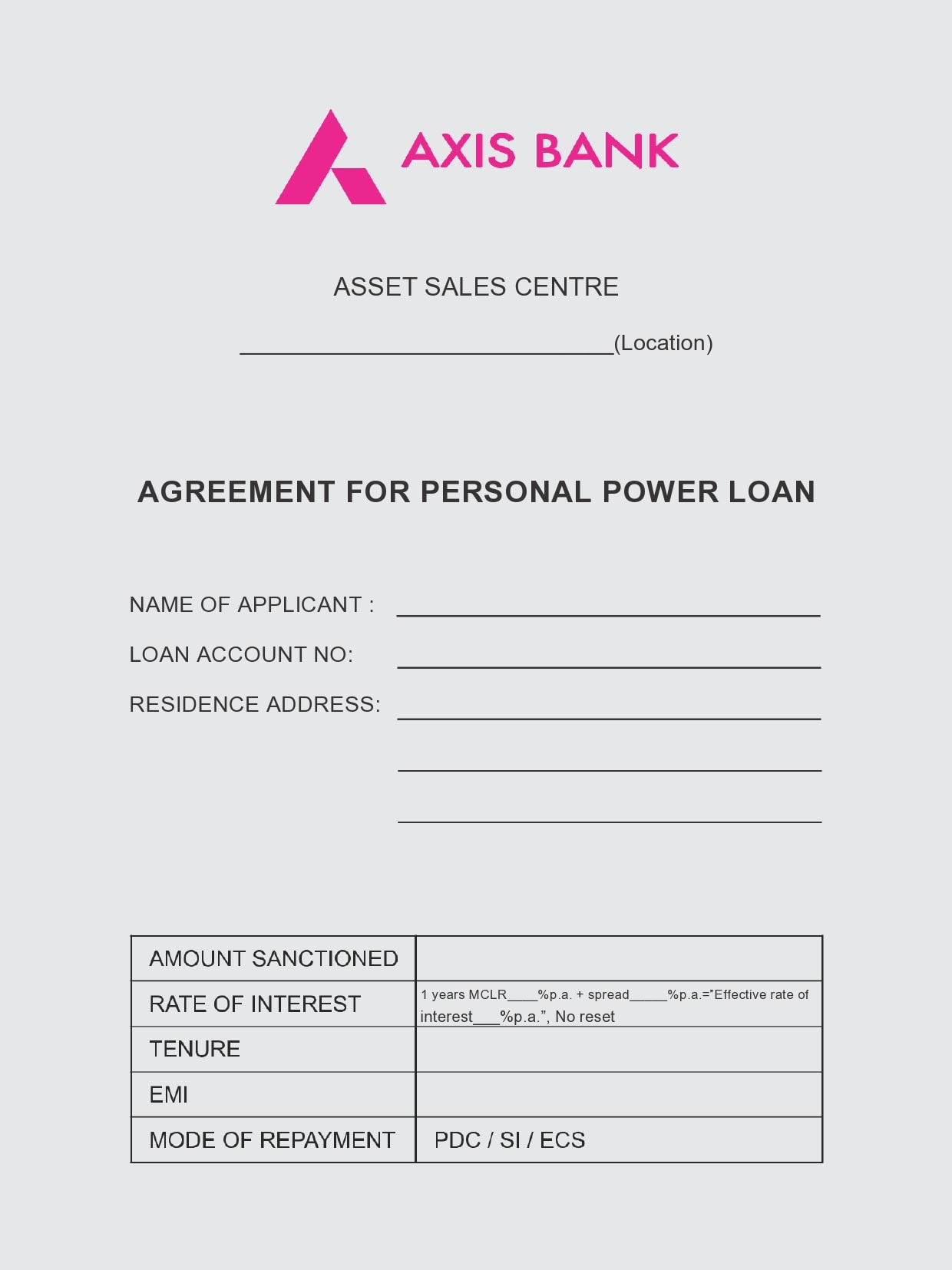

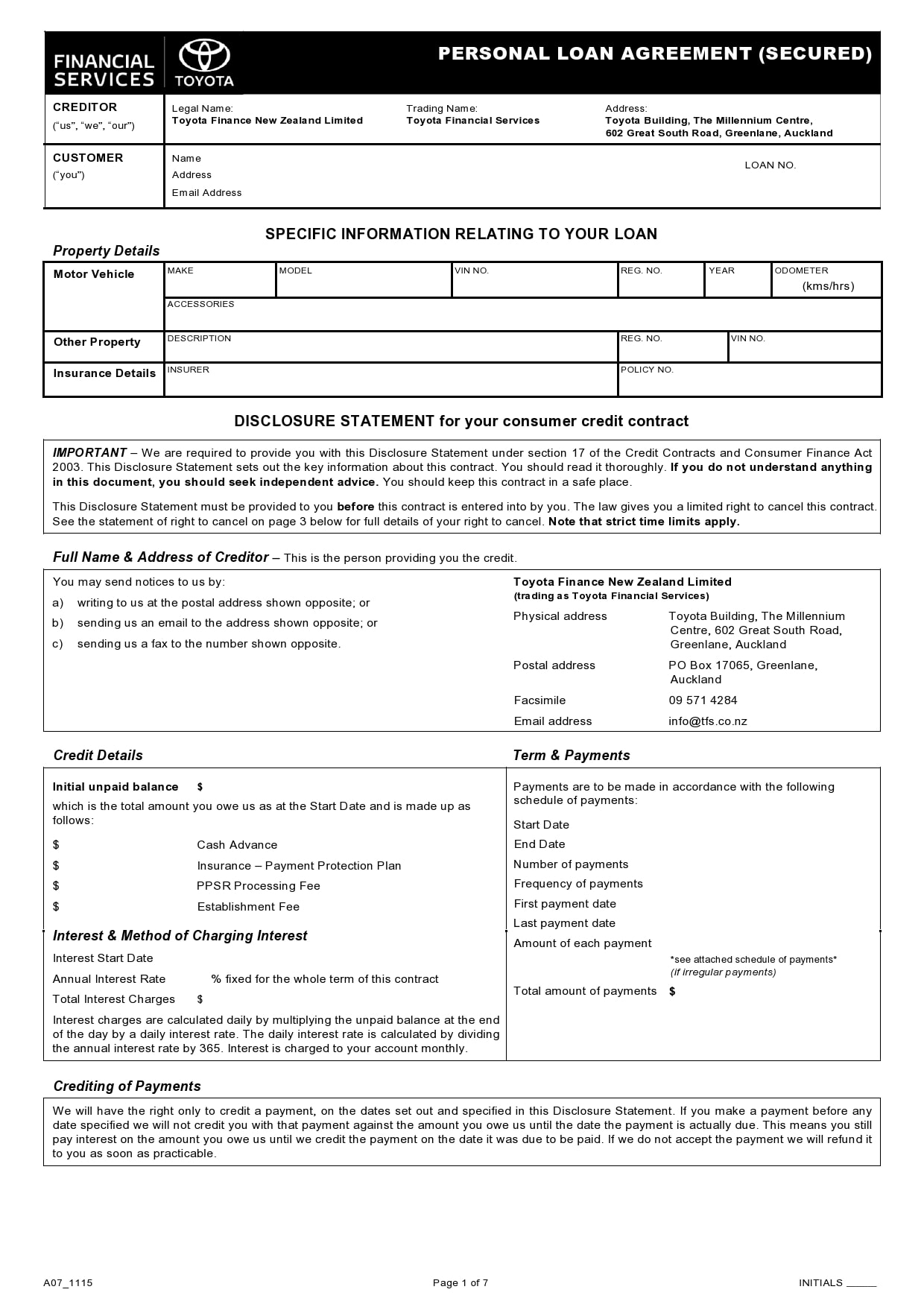

A personal loan template is a legally binding agreement between a borrower and a lender that describes the terms of a personal loan. It typically includes the amount, payment details, and your rights as the lender, should the borrower default on the loan.

This type of loan is generally meant to meet current financial obligations of the borrower. When creating a personal loan format, include the following:

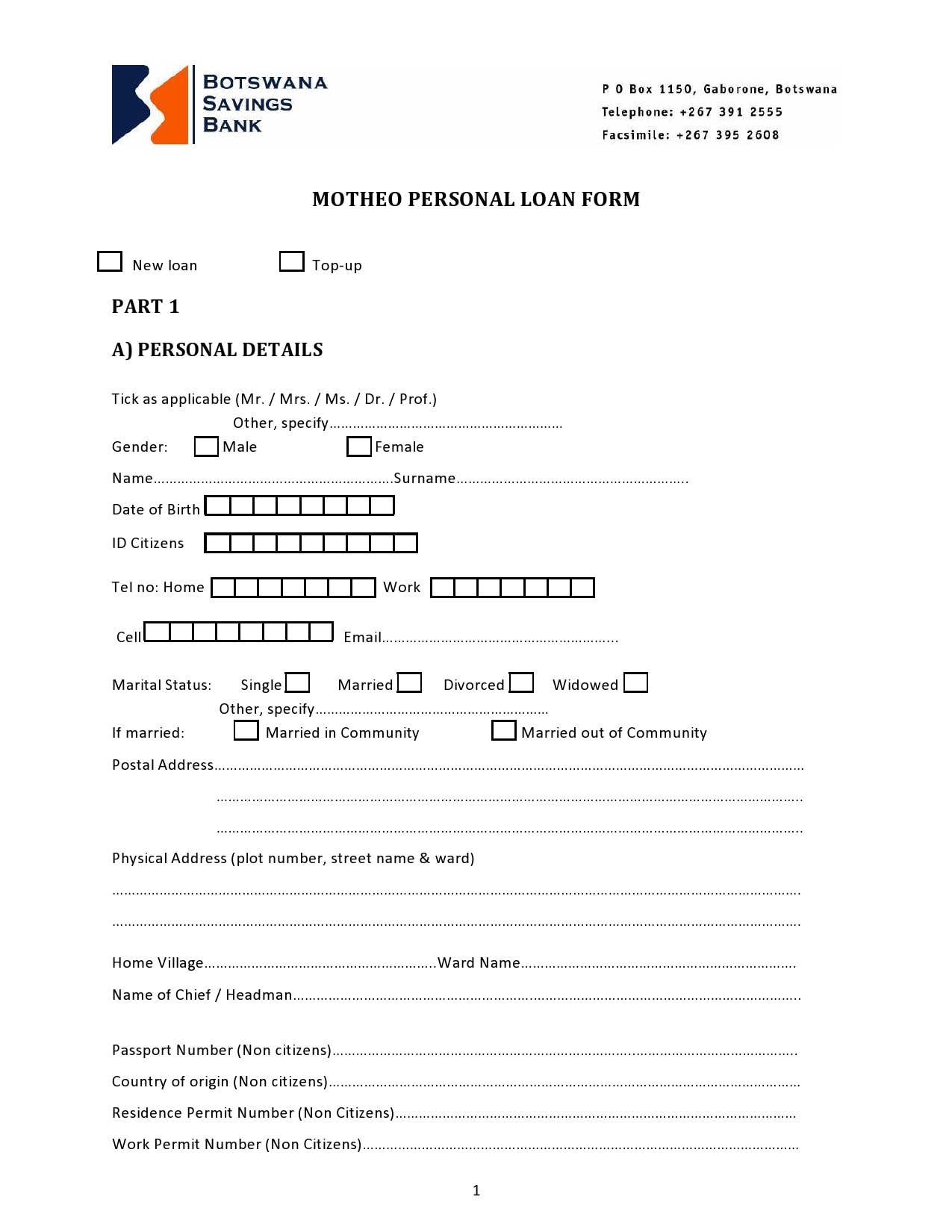

- Personal Details

The agreement must contain the complete names, addresses, and contact details of yourself and the borrower. - Date

The agreement should specify the date when you created it. - Loan Amount

The agreement should indicate the total amount that the borrower loan from you. - Repayment Details

The agreement should specify whether the borrower will pay you back periodically or with a lump sum. - Interest Rate

The agreement should specify the agreed-upon interest rate. - Late Payments and Consequences of Defaulting

The agreement must indicate when you will consider the loan payments late and the implications of these late payments. For example, late payments could result in late fees – and you should specify the amounts. The agreement should also specify what happens if the borrower violates any terms of your agreement. - Guarantor Details (if applicable)

If the borrower has a guarantor in the agreement, he should also sign the document. The guarantor is a third-party who must repay the loan if the borrower fails to do so. Of course, it is not a requirement for a personal loan to have a guarantor – but it will give you a greater sense of security.

")