Some people take out loans or borrow money and at times, forget their obligations while there are those who intentionally miss their payments. As a debt collector or the official representative of a debt collection agency, you would create a collection letter template and send it when asking for payment for an obligation or in case of overdue bills.

Contents

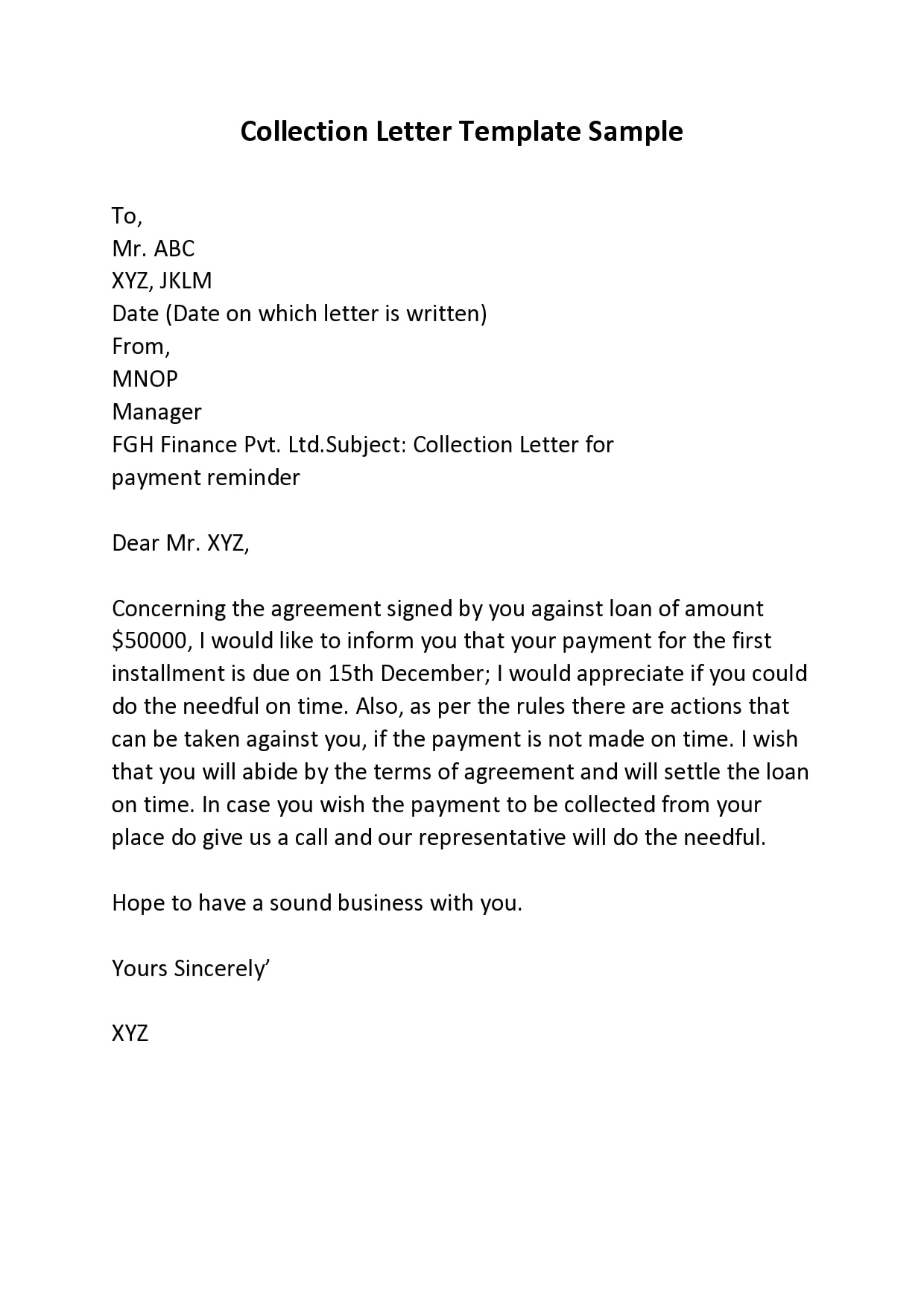

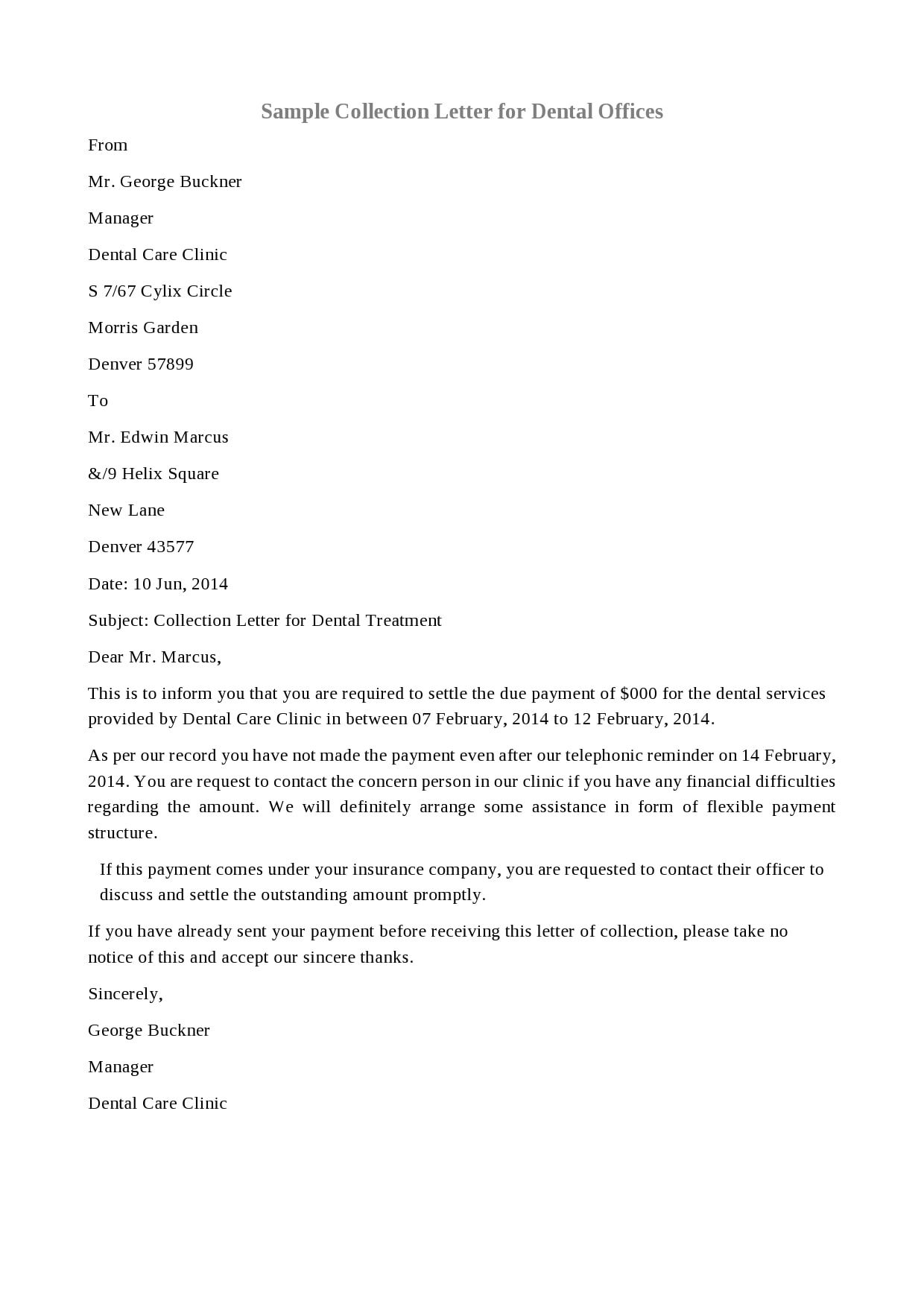

Collection Letter Templates

What is a collection letter?

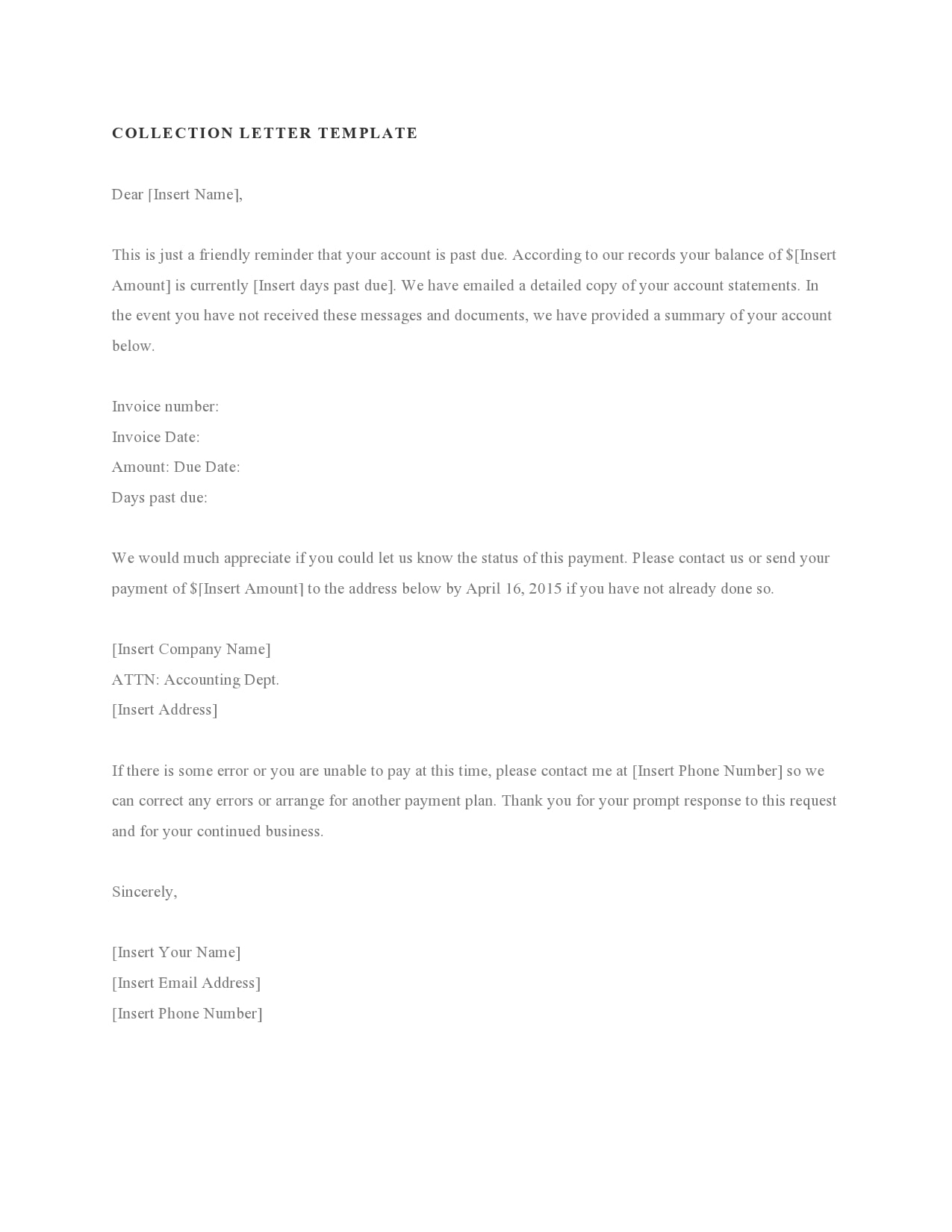

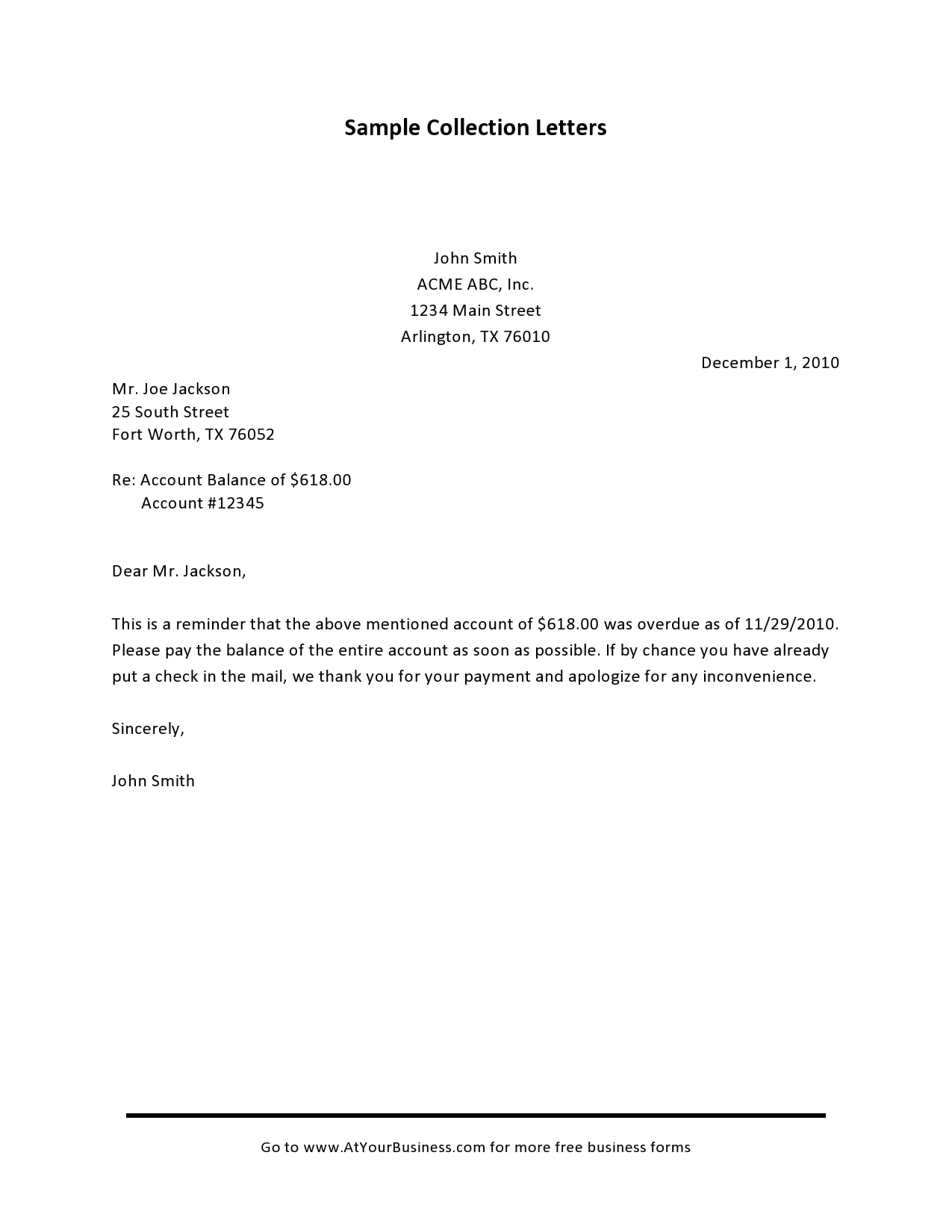

A payment collection letter is a document sent in writing that informs a client of their payments that are already past due. The main function of this letter is to serve as a reminder to a debtor of their delinquent payment owed to a creditor.

Some delayed payments may occur because the customers forgot these payments and as such, a collection letter template becomes the best method for early recovery of debt as it produces positive results and it’s cost-effective. You would issue these letters consecutively with serial reminders.

How many letters you issue depends on your agency’s policy of recover procedures. It’s standard procedure to send a letter when the debtor’s invoice has passed the due date. Financially, this could mean that the debtor has fallen behind their regular remittances and owe a specific amount to their creditor.

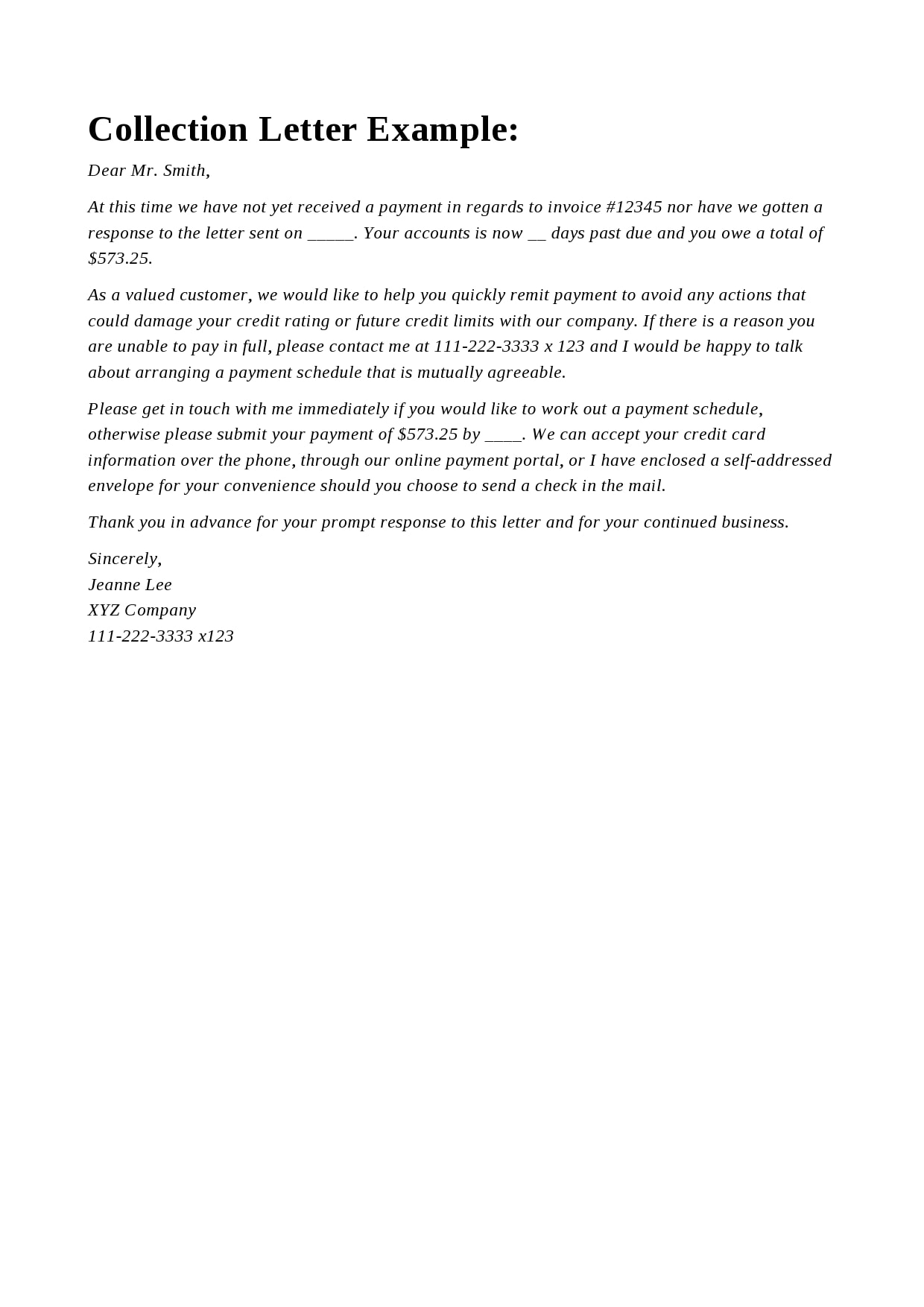

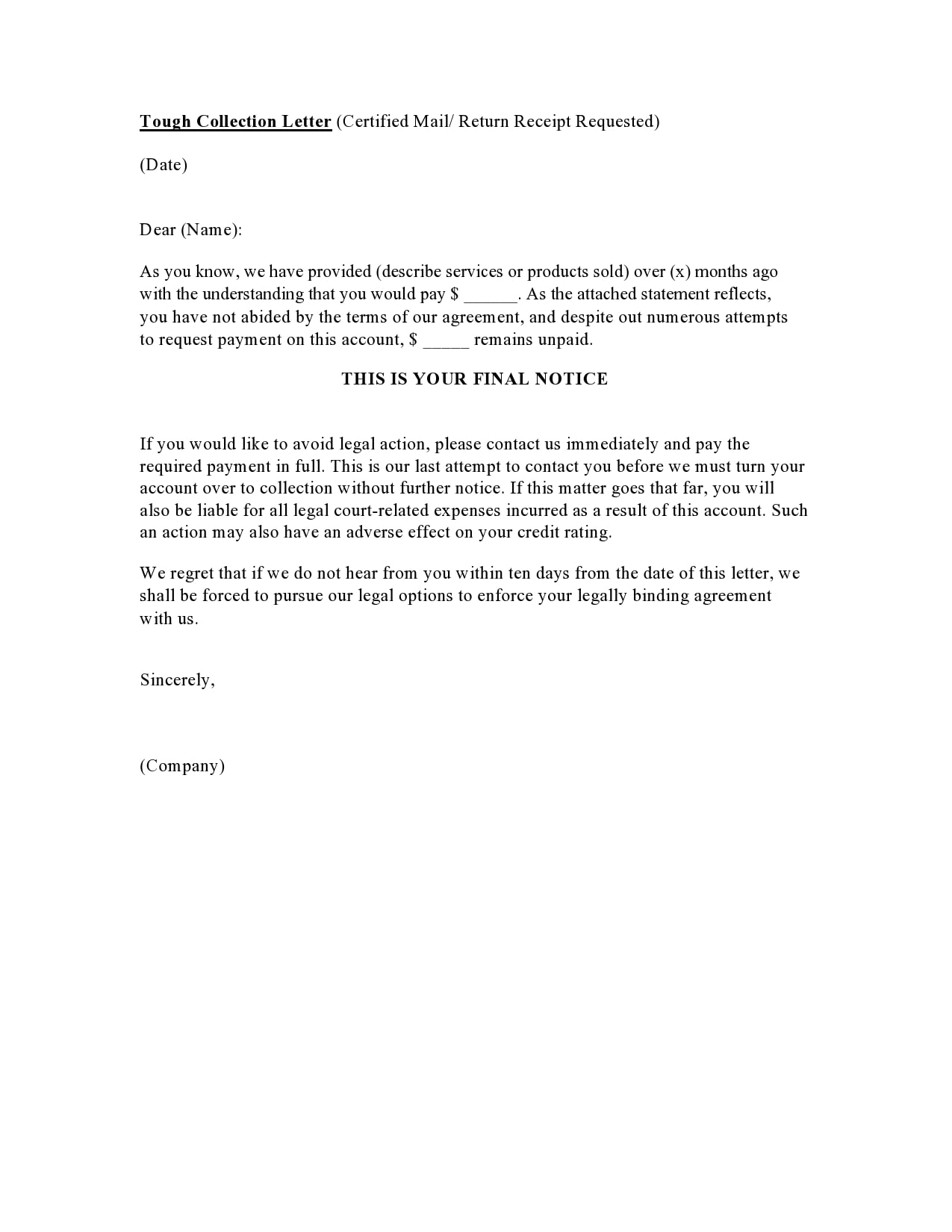

Past Due Letters

Types of collection letters

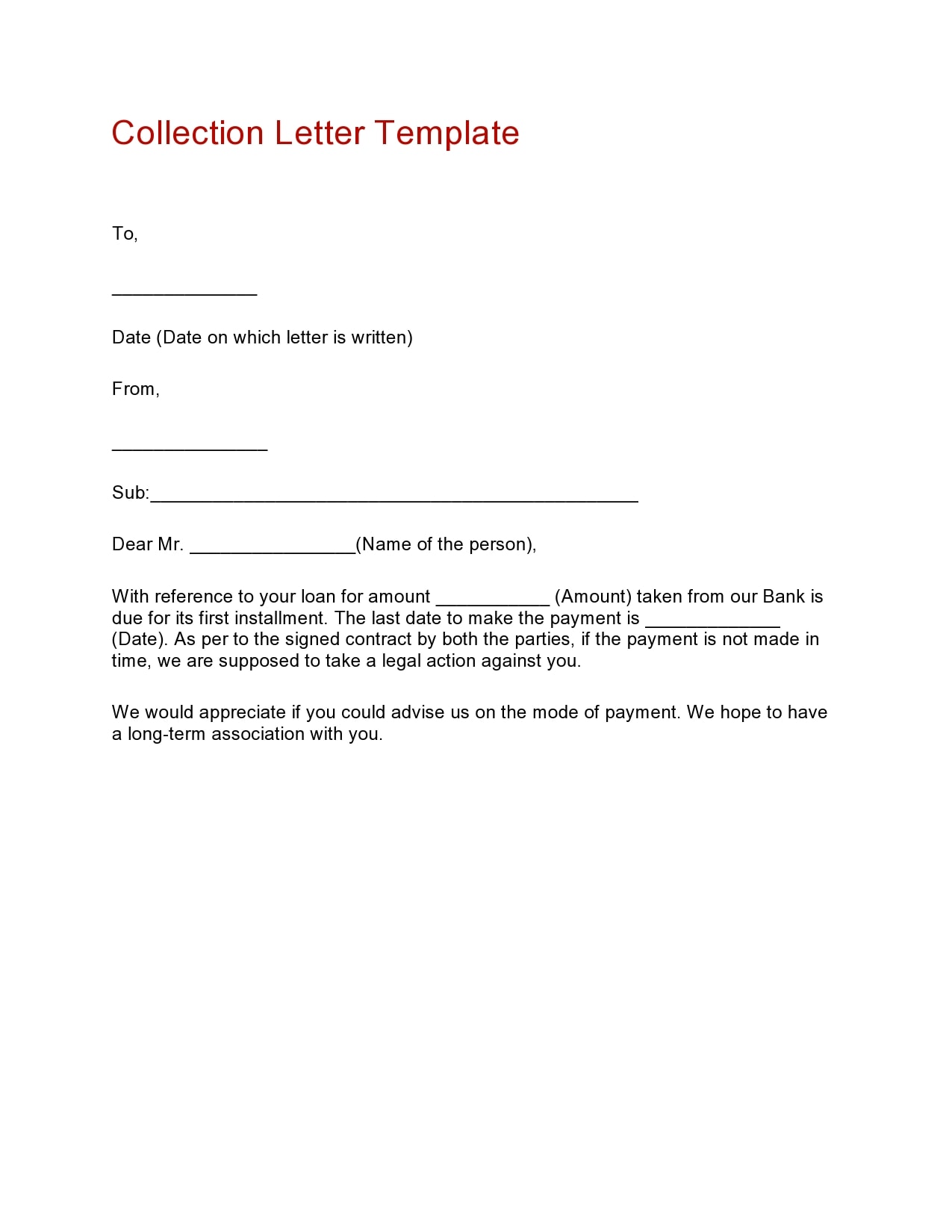

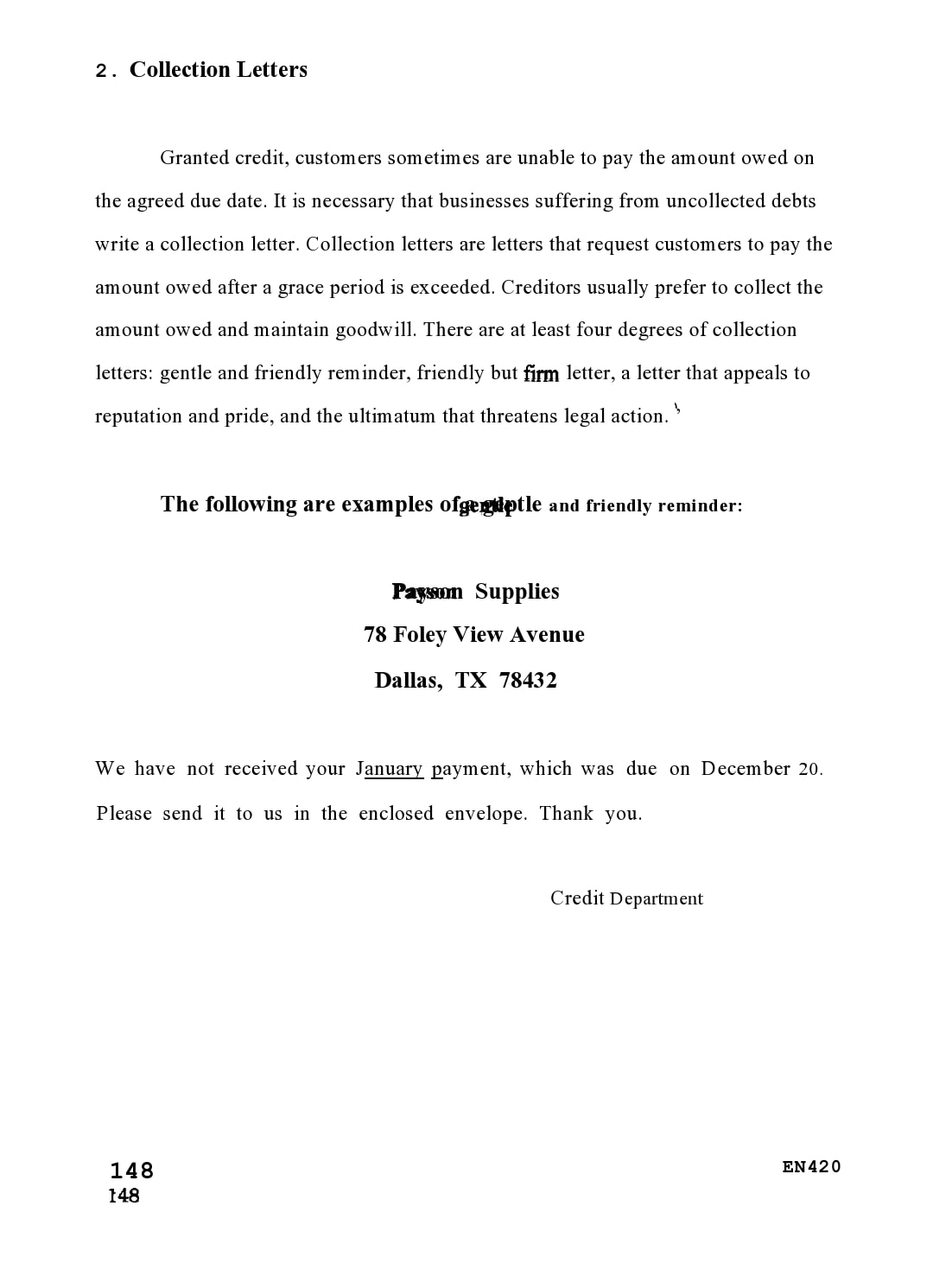

There are four types of collection or past due letter templates that you can send to your customers. When there is a response from your customer after you have tried calling or sending them collection notices, there will no longer be a need to send more letters.

That is unless they fail to meet another payment deadline. Here are the different types of collection letter templates you can create:

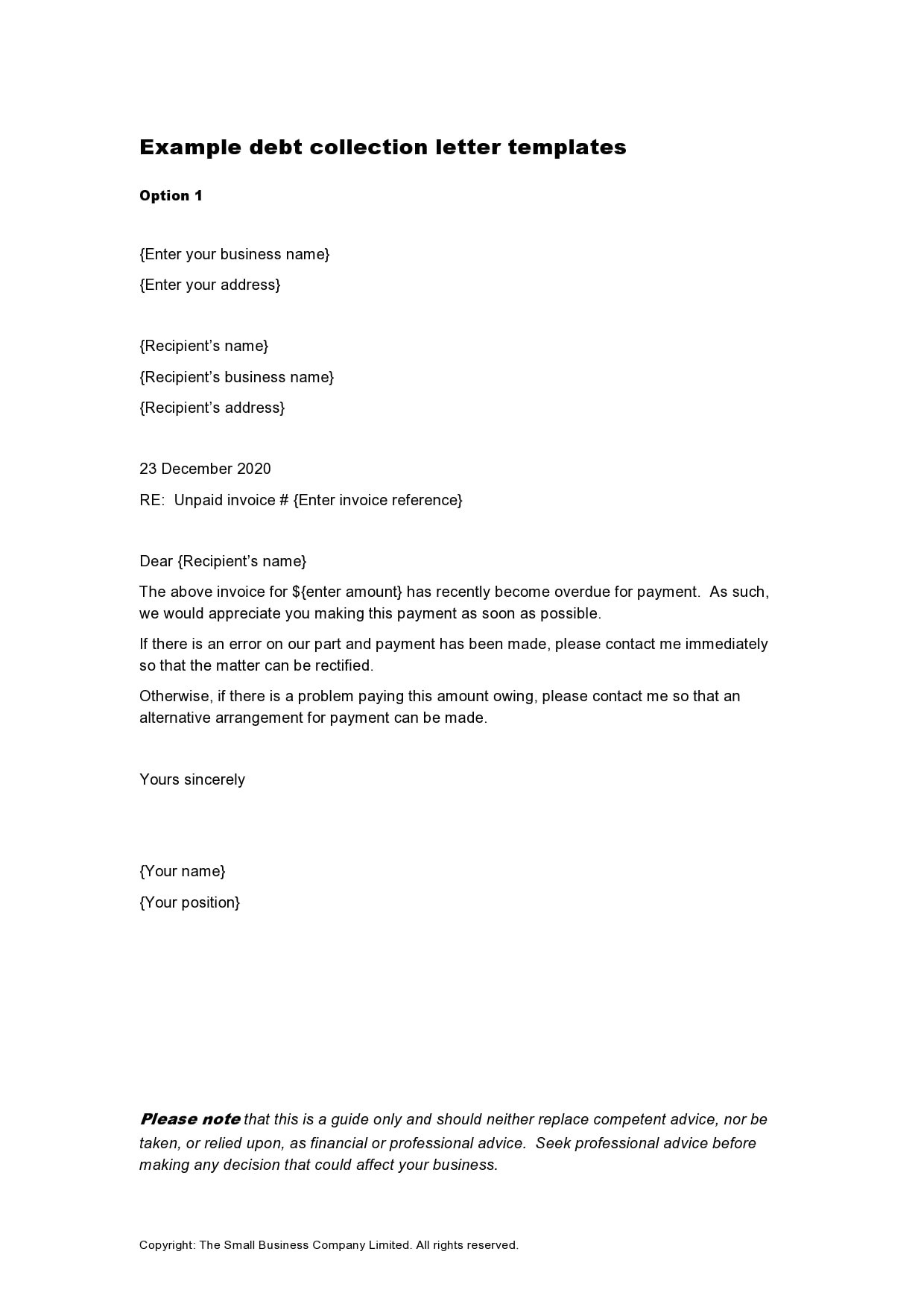

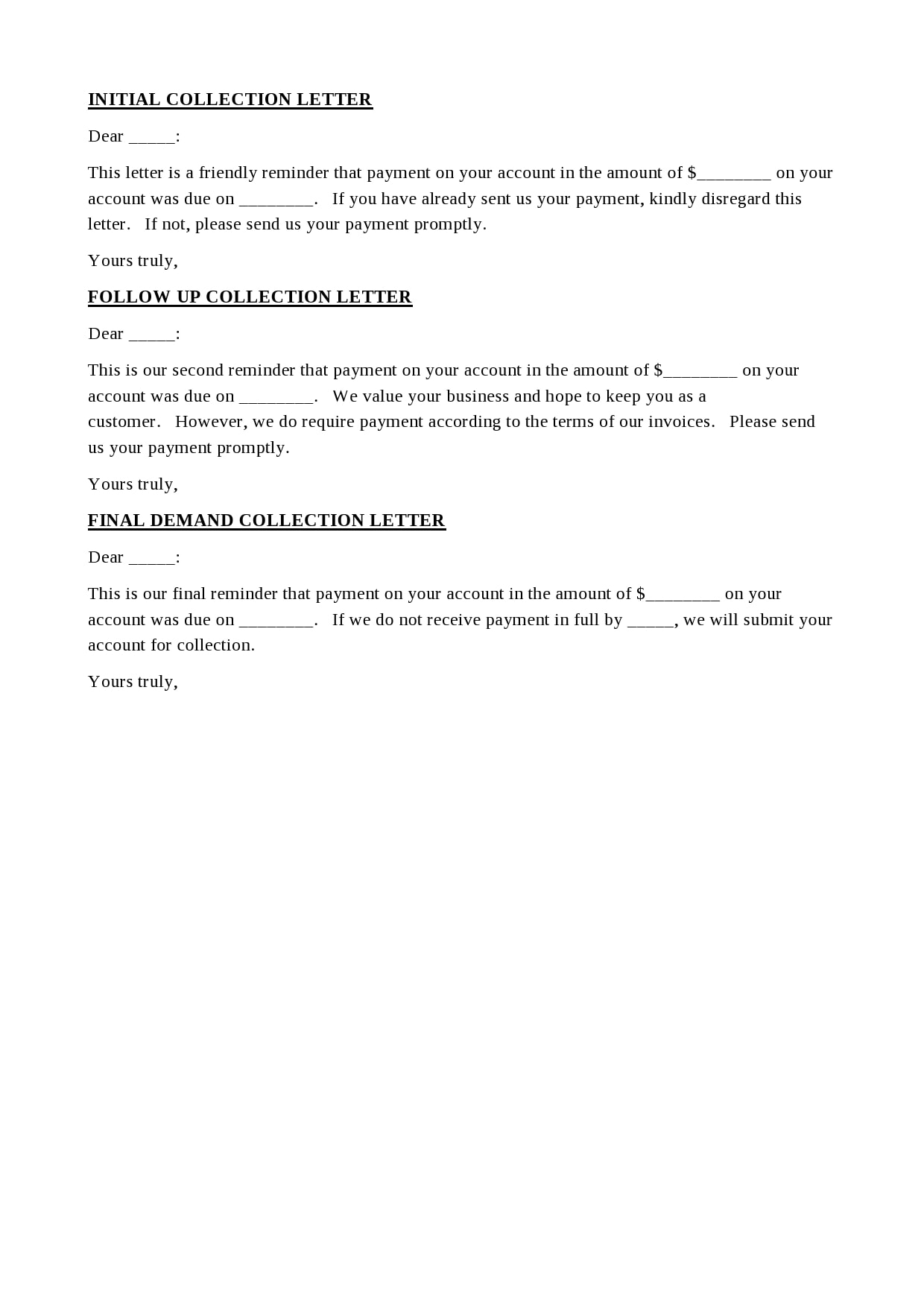

- First Collection Letter

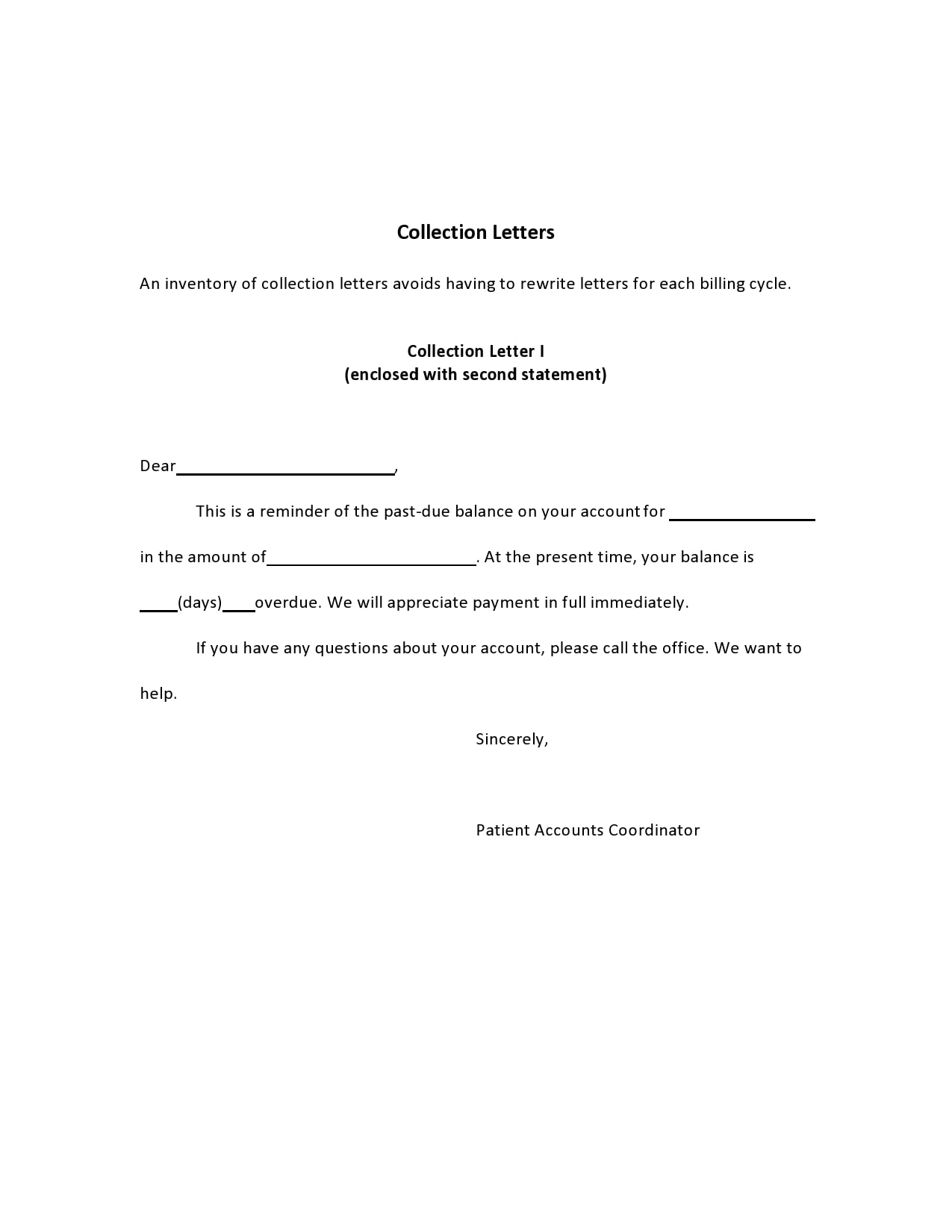

If a customer doesn’t respond when you call or send an email, you should send the first past due letter. If you’re using accounting software, you can choose to send email reminders to your customers automatically. - Second Collection Letter

Try reaching the customer again through email or phone before sending the second collection letter. There is always the possibility that they have already made the payment or received your first letter.

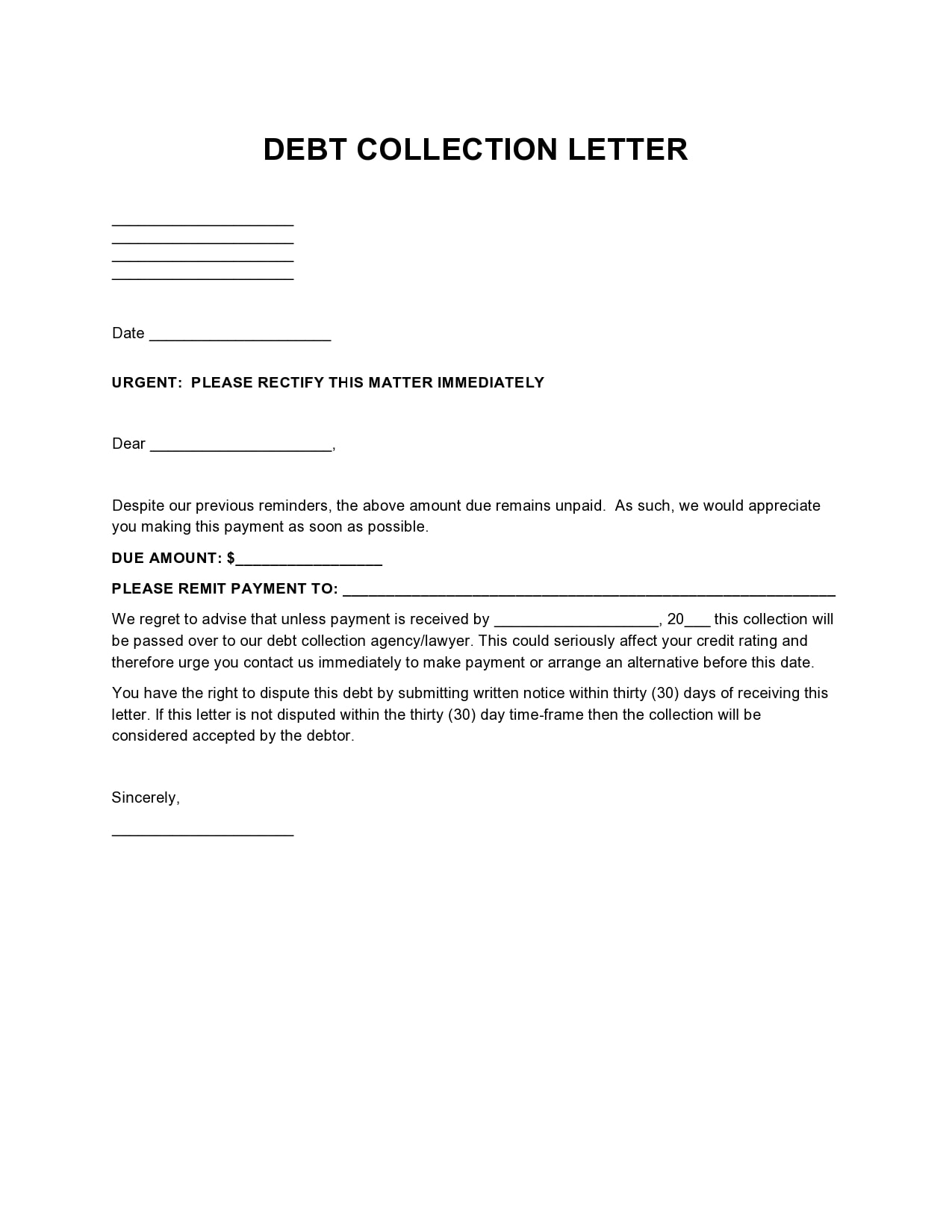

If your attempts are still unsuccessful, sending the second letter becomes essential. Indicate in the letter that you have tried to reach them through the first letter. - Third Collection Letter

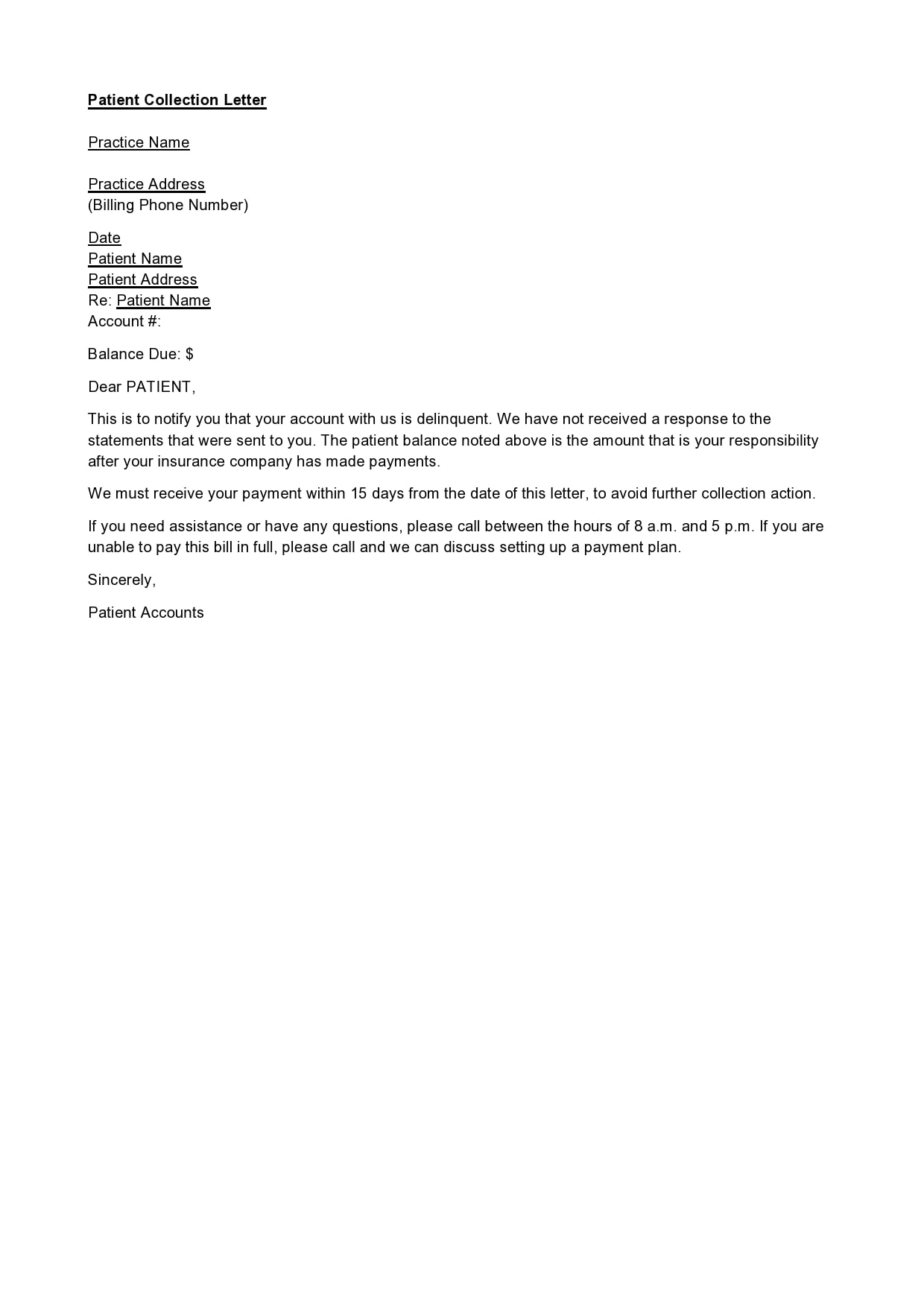

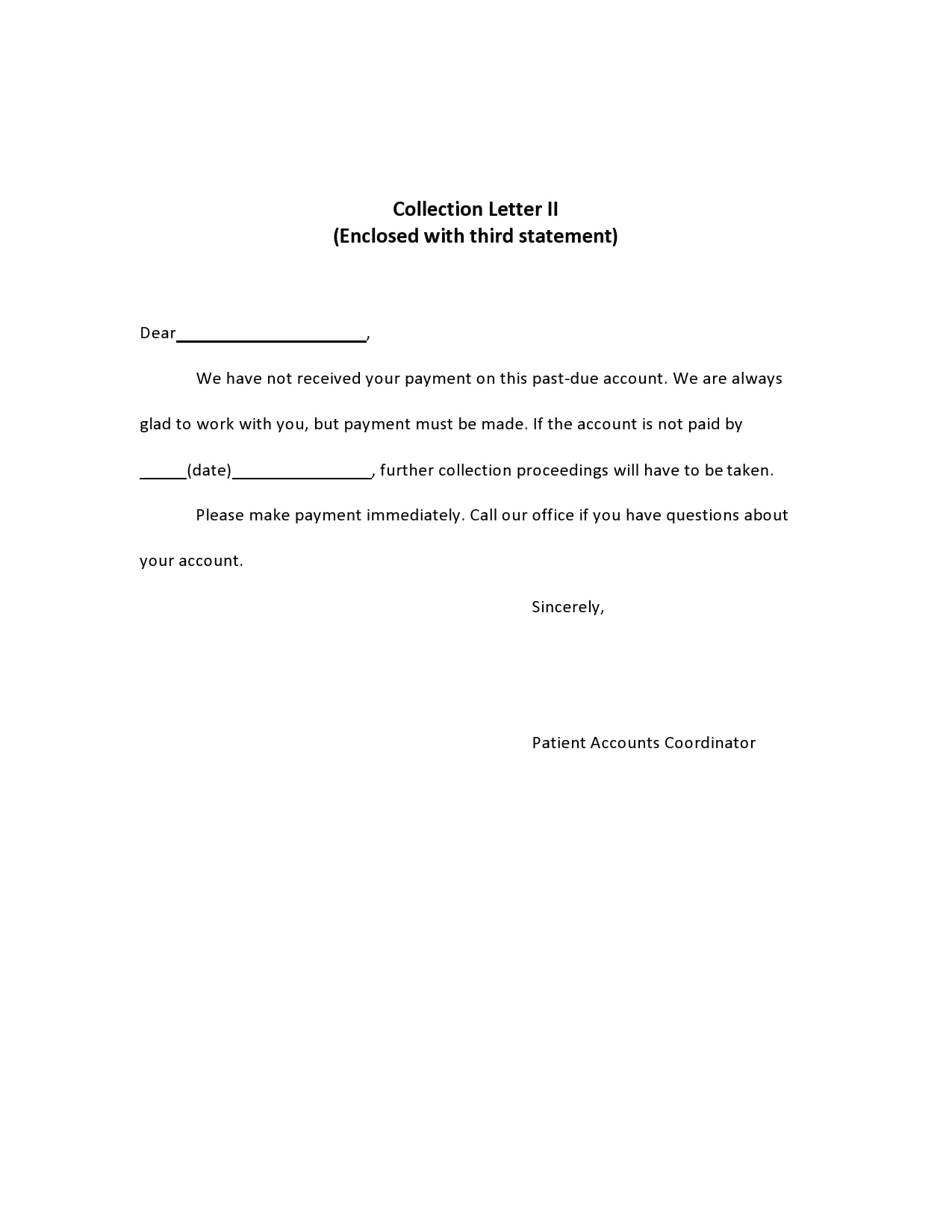

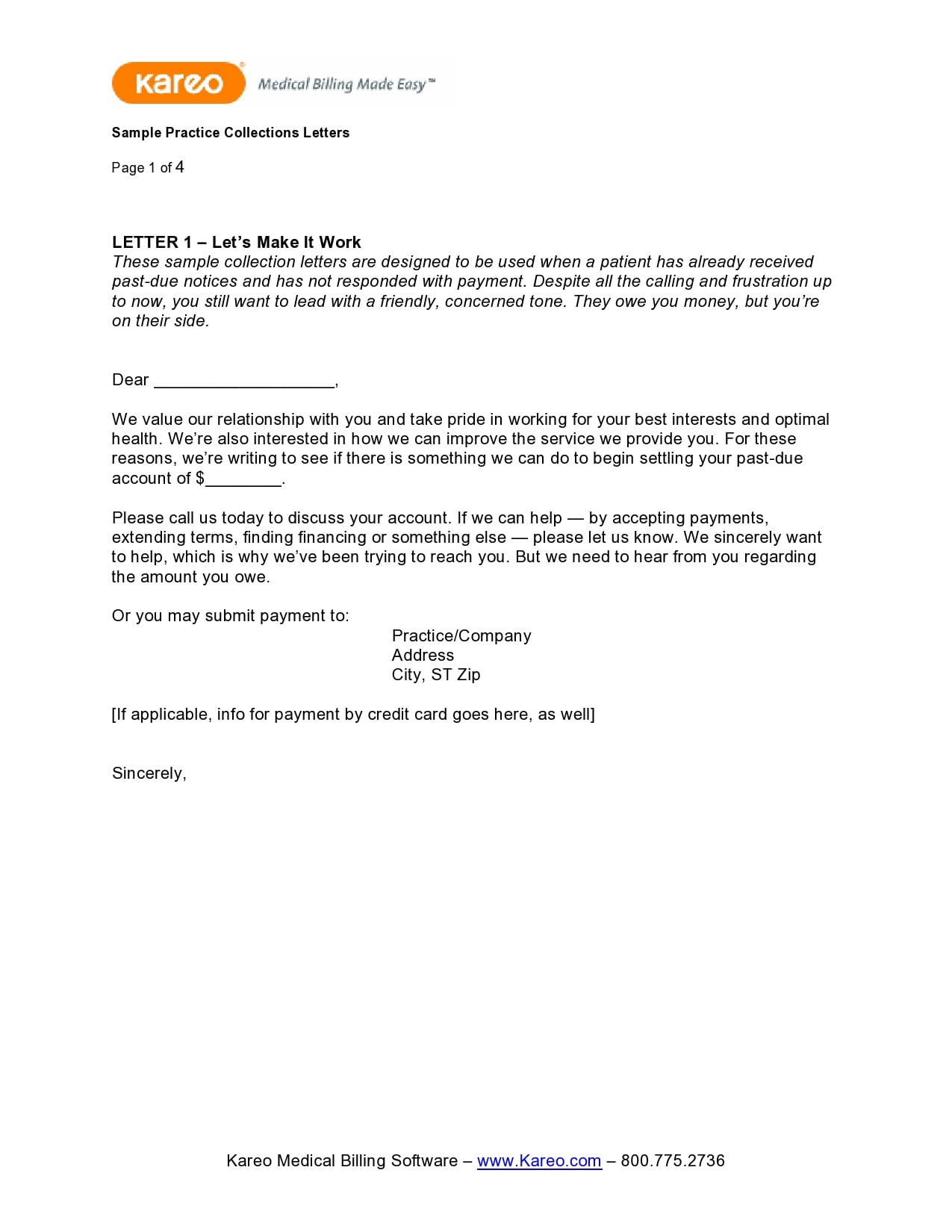

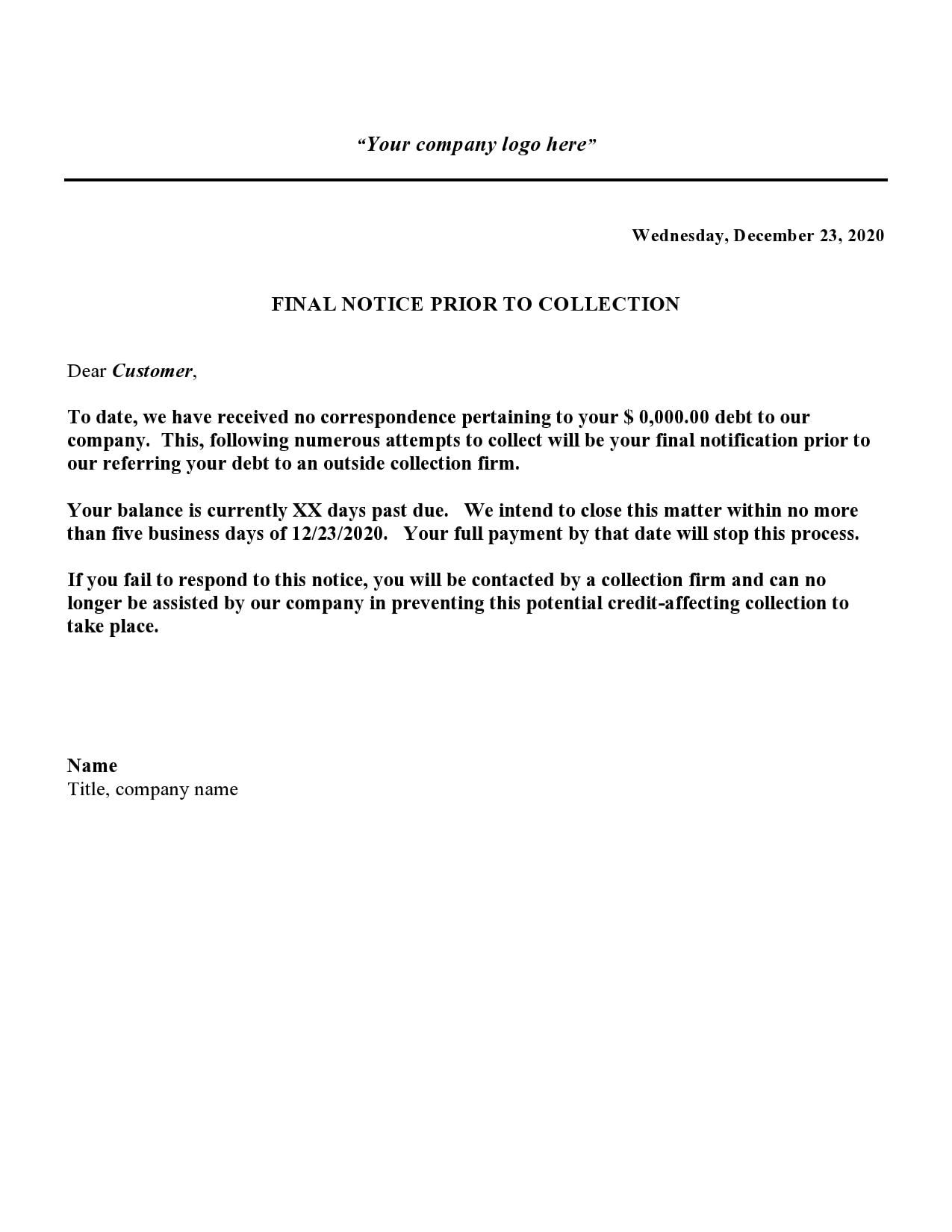

If you still don’t receive any response after the second letter, try calling the customer again. But if you still cannot reach them after a couple of weeks, it is time to send the third letter. Here, you will explain the several attempts you tried to contact them through phone, email, and letters, but with no success. For this letter, it’s recommended to send it via certified mail. - Fourth Collection Letter

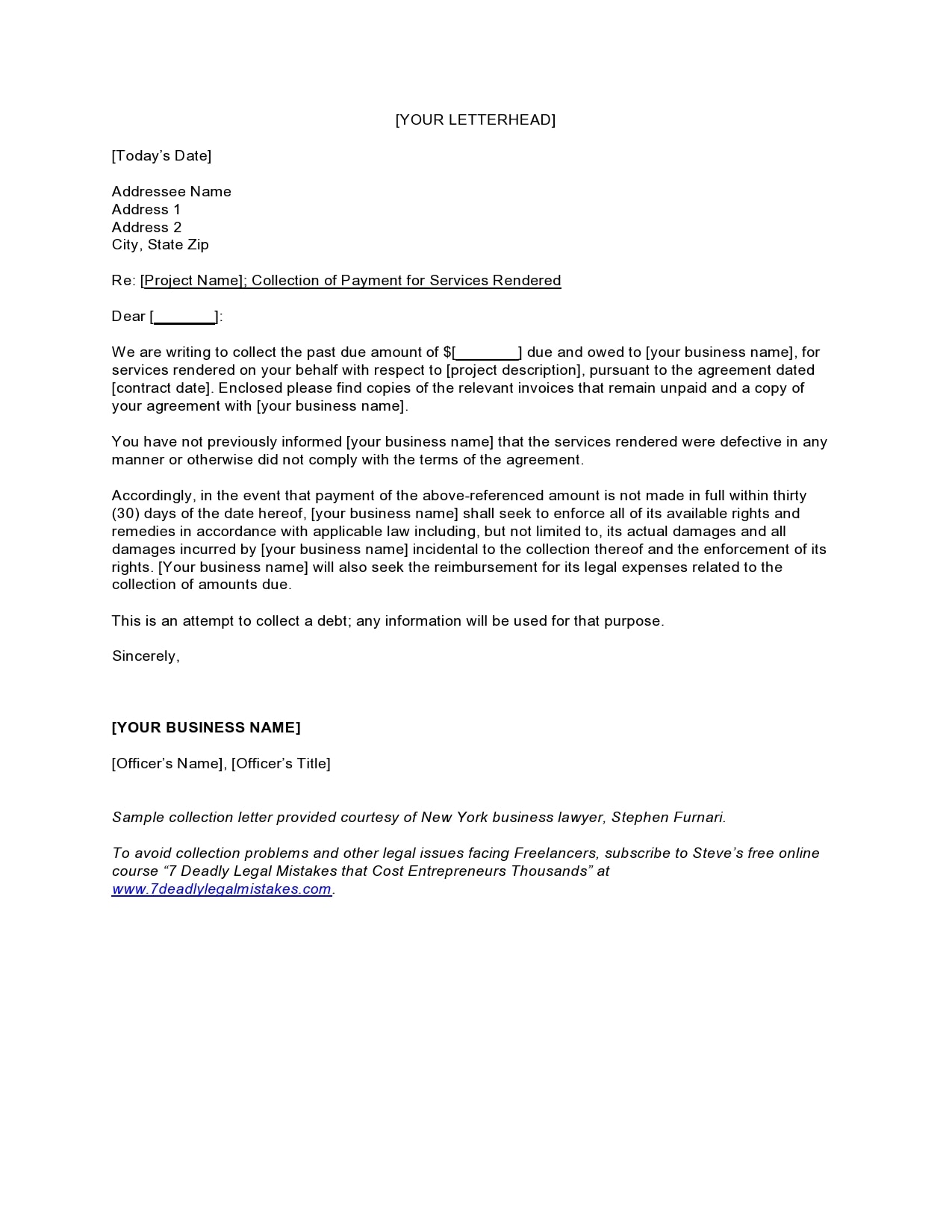

In most cases when it comes to sending the fourth letter, one can already deduce that the customer either isn’t willing or isn’t able to pay their debt. In this letter, you use more assertive language while staying professional. You should also send this via certified mail.

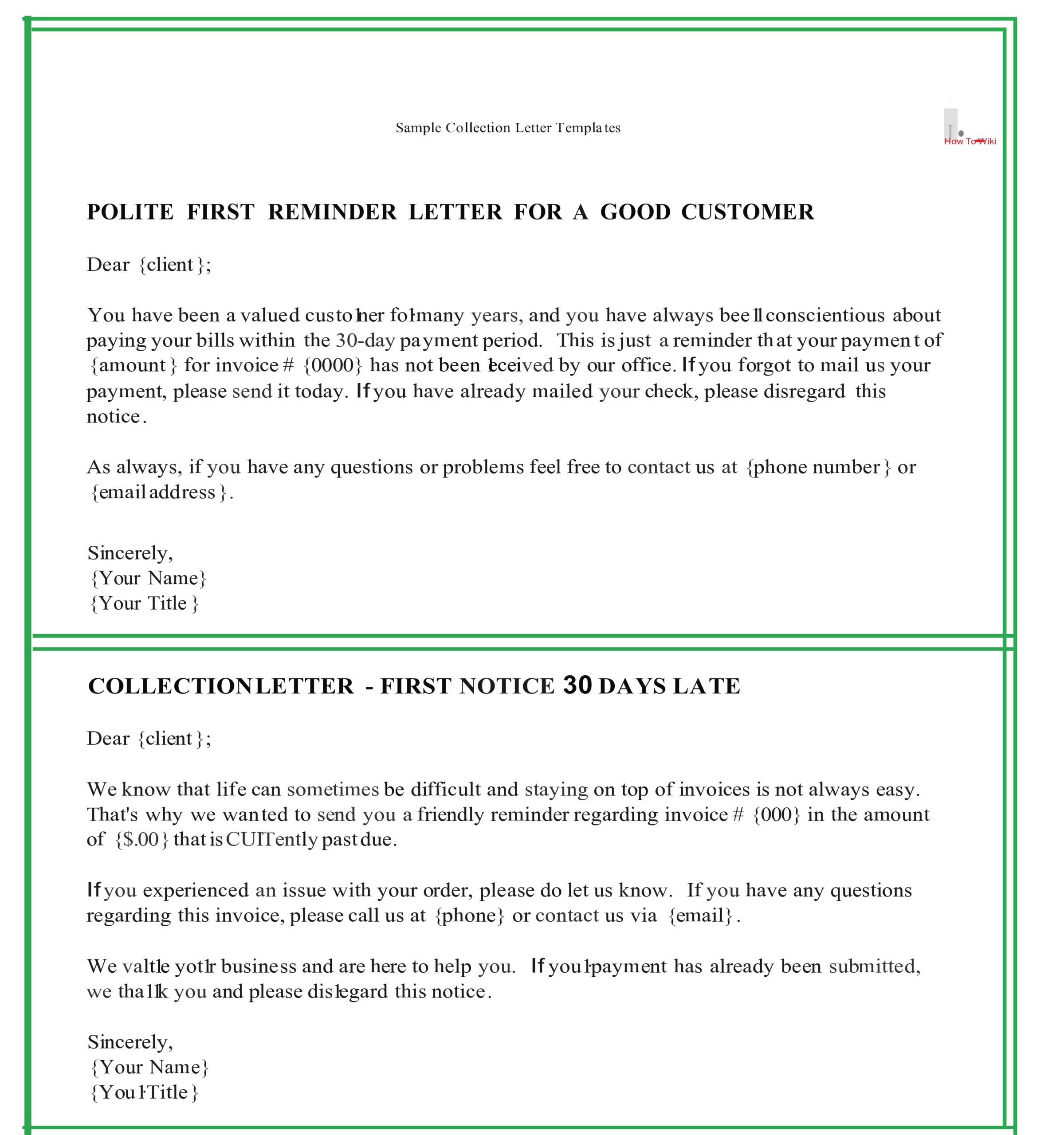

How do I write a collection letter?

In order to maintain good relations with your customers, the collection letter template you create should be as professional as possible. You have to make them realize that you’re serious about collecting payments while at the same time preserving the relationship.

The following are pointers to consider when making a collection letter template:

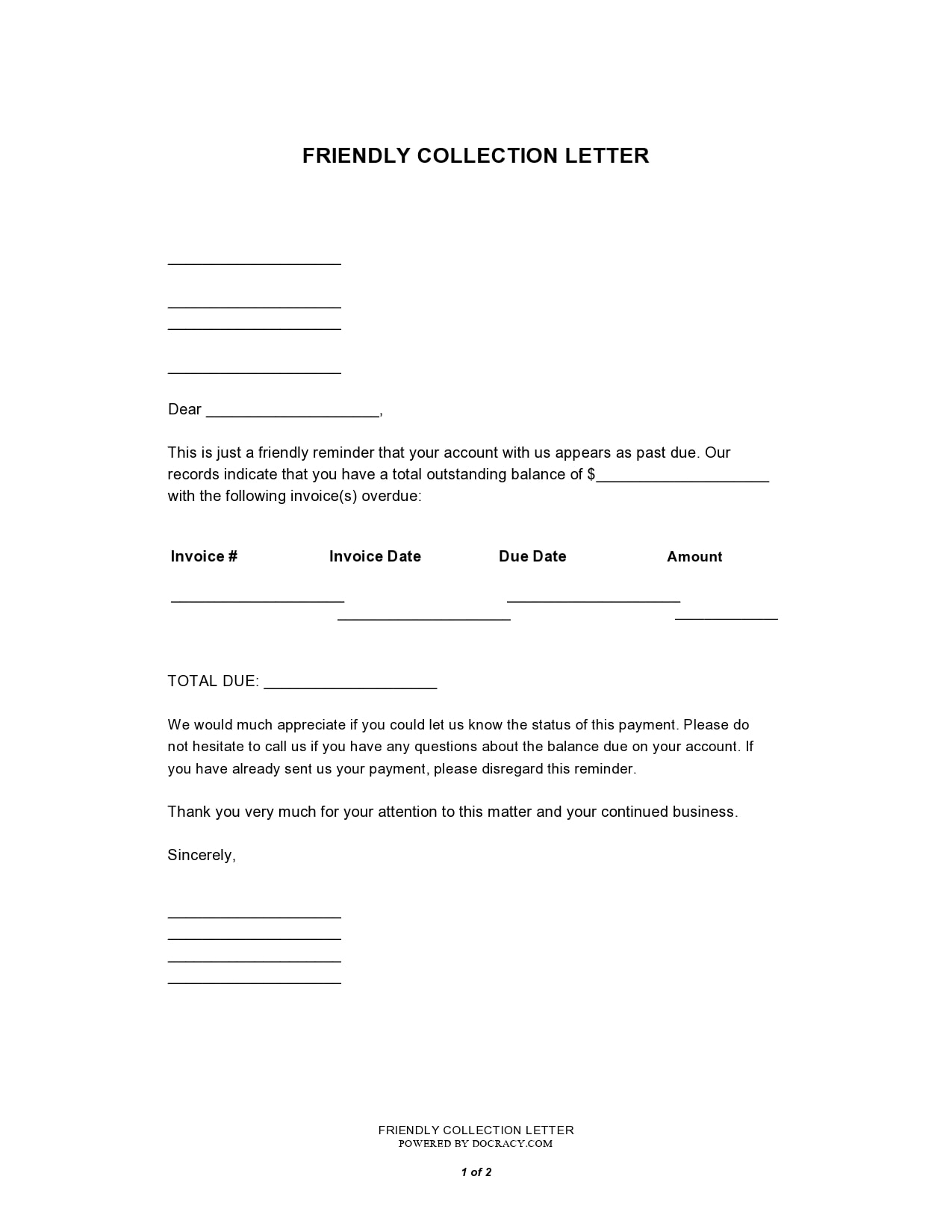

- Keep the letter short and to the point without using complex language.

- Type the letter – don’t handwrite it.

- Use your company letterhead.

- Include copies of the invoices or a summarized statement if the customer has several outstanding invoices.

- Specify all relevant dates and deadlines.

- Include the payment methods you accept.

- Also, include your contact details for the customer to reach out to you as needed.

- Mail the letter in a postage-paid envelope or through certified mail.

Debt Collection Letters

How to write a dispute letter to a collection agency?

Now let us consider the situation when a client receives a debt collection letter from you or some other debt collection agency but they don’t believe that they owe anything or the amount you’ve written down in the letter isn’t accurate.

In such a case, the client can dispute your past due letter by composing a letter that formally declares that they’re disputing the debt. Here are the steps to do this:

- The client verifies that the letter came from a legitimate agency

By federal law, credit bureaus should verify the accuracy of the debt then send verification of its validity to the client. In case the debt isn’t accurate, you must remove the item from the client’s credit report.

Aside from verifying their debt, clients should also verify the legitimacy of the collection agency. This is important as there is now an increasing trend of notices from fake collection agencies.

To verify its legitimacy, they can use the Secretary of State or Division of Corporations website in the state where your collection agency operates and search for the name of your agency. - The client may call your agency and speak with your manager or supervisor

The next thing clients do is to get in touch with your collection agency to speak with someone who has the authority to make decisions with regards to collection accounts. Then they will make a request for a verification of their debt then notify your manager or supervisor of their intent to dispute. - The client writes the letter with all of the required information

This information includes:

Their complete name

Their address

The name and address of your collection agency

A request for the amount of the claimed debt

A request for the original creditor’s name

A request for judgment information

A request for proof of your agency’s license.

Their signature

The letter should also include a citation to the Fair Debt Collection Practices Act and a disclosure that they’re keeping records of all communications that your collection agency initiates. - The client sends the letter

Should you or anyone in your agency respond to the client’s letter, it will your burden under federal law, to show proof of the debt’s validity. If it’s not, you should refrain from any further collection attempts. Under federal law, you should also inform each credit bureau of the debt’s inaccuracy if you cannot verify it.

")

")