Keeping a close eye on your income and expenses help you save money in the long run. One of the most effective ways of keeping an eye on your budget is through the maintenance of a weekly budget template.

Contents

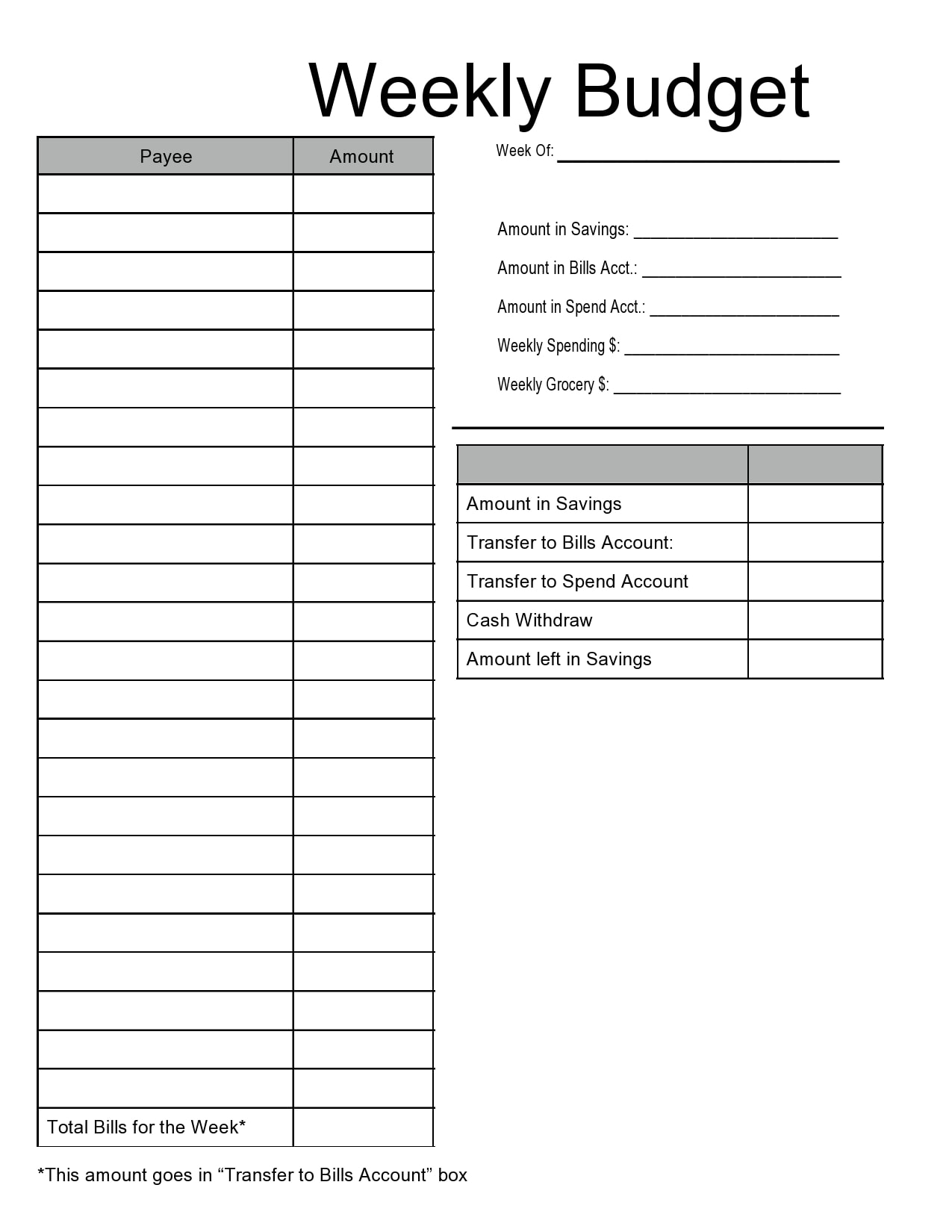

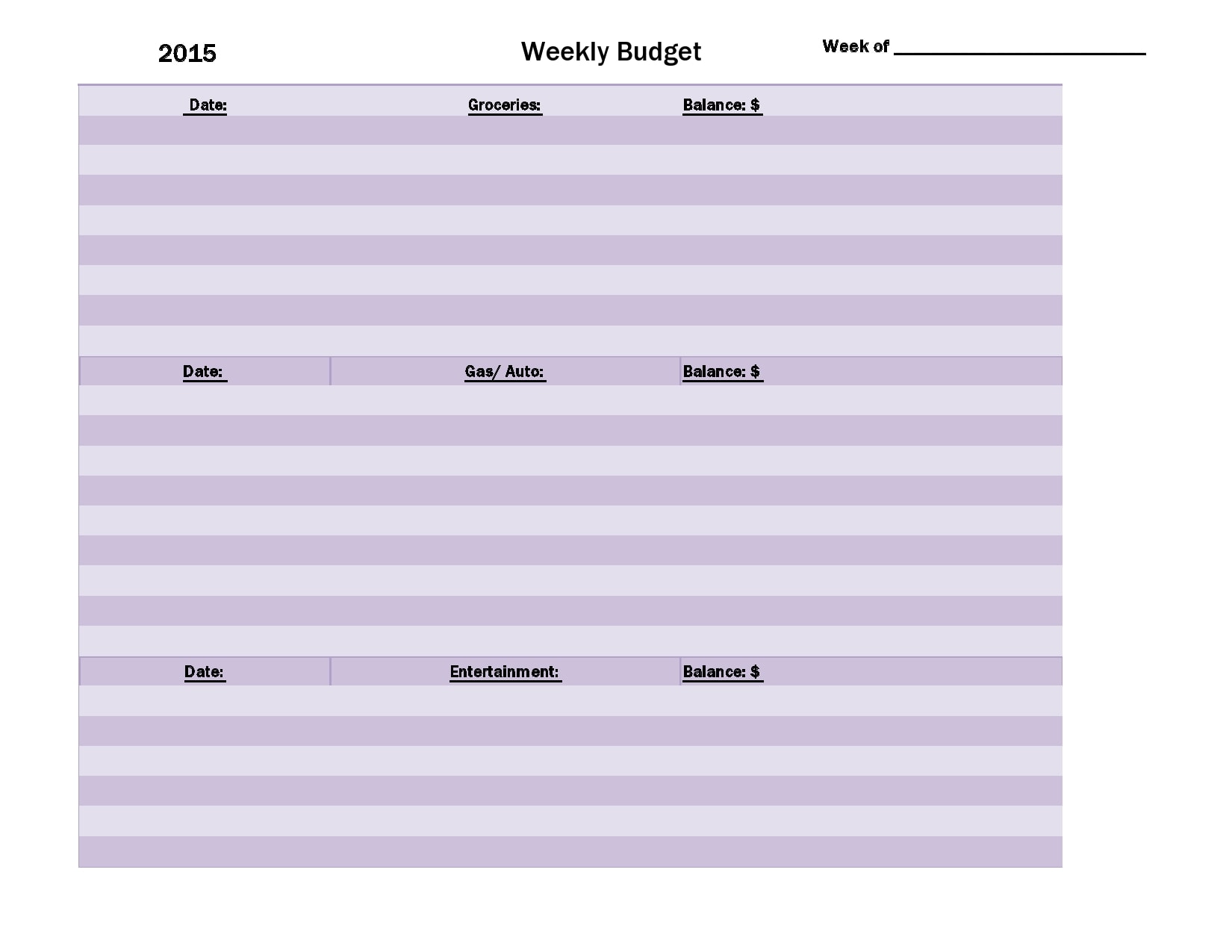

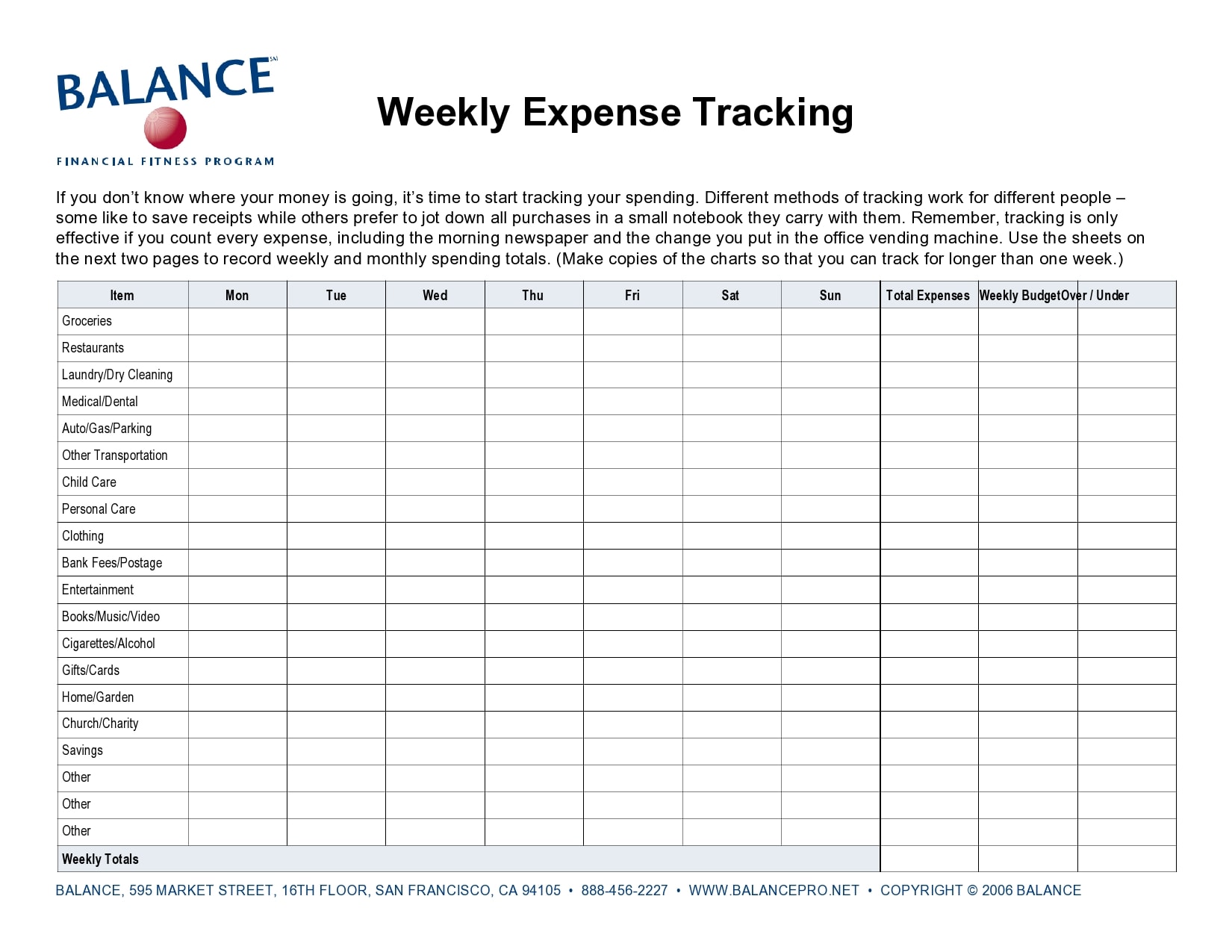

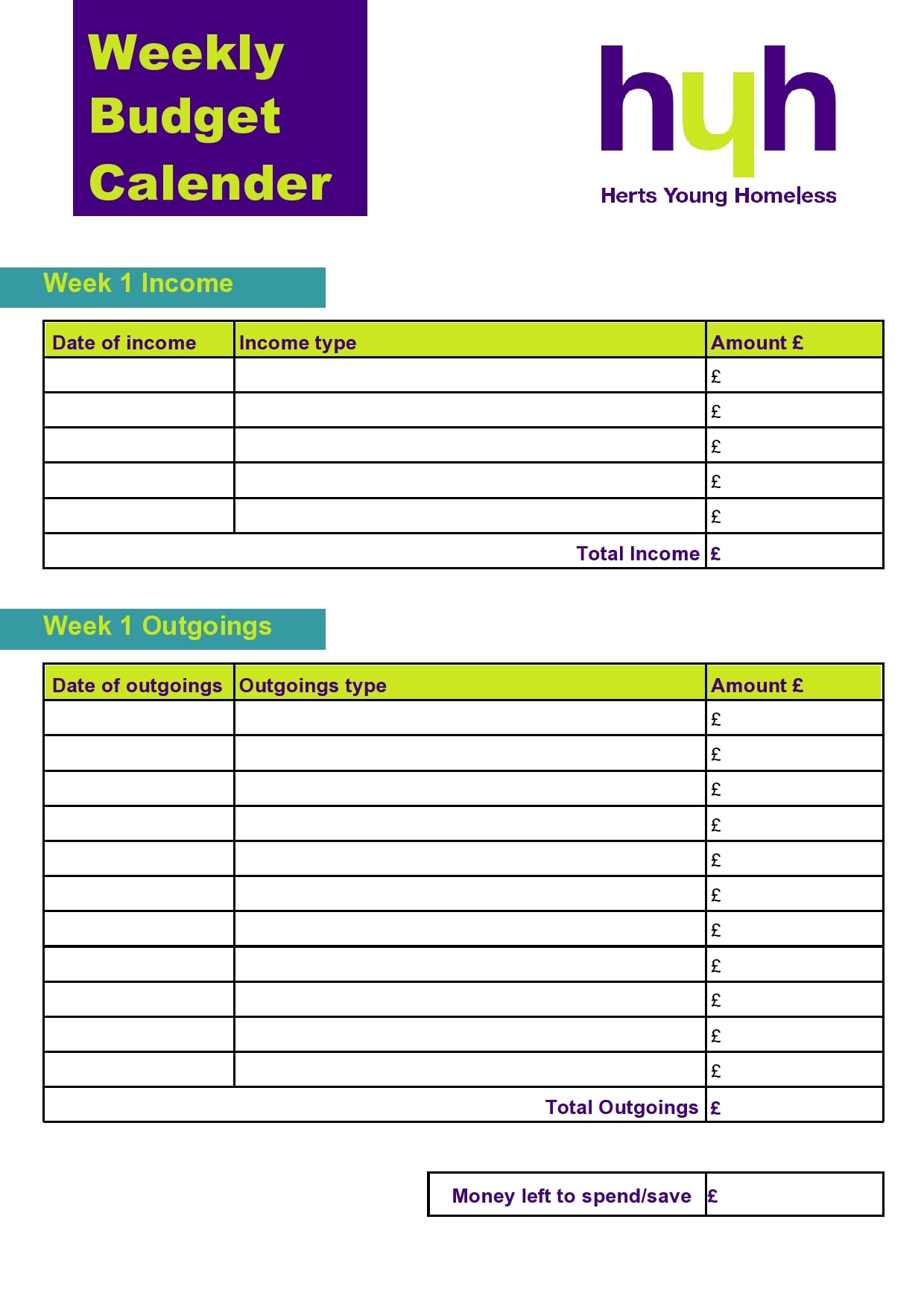

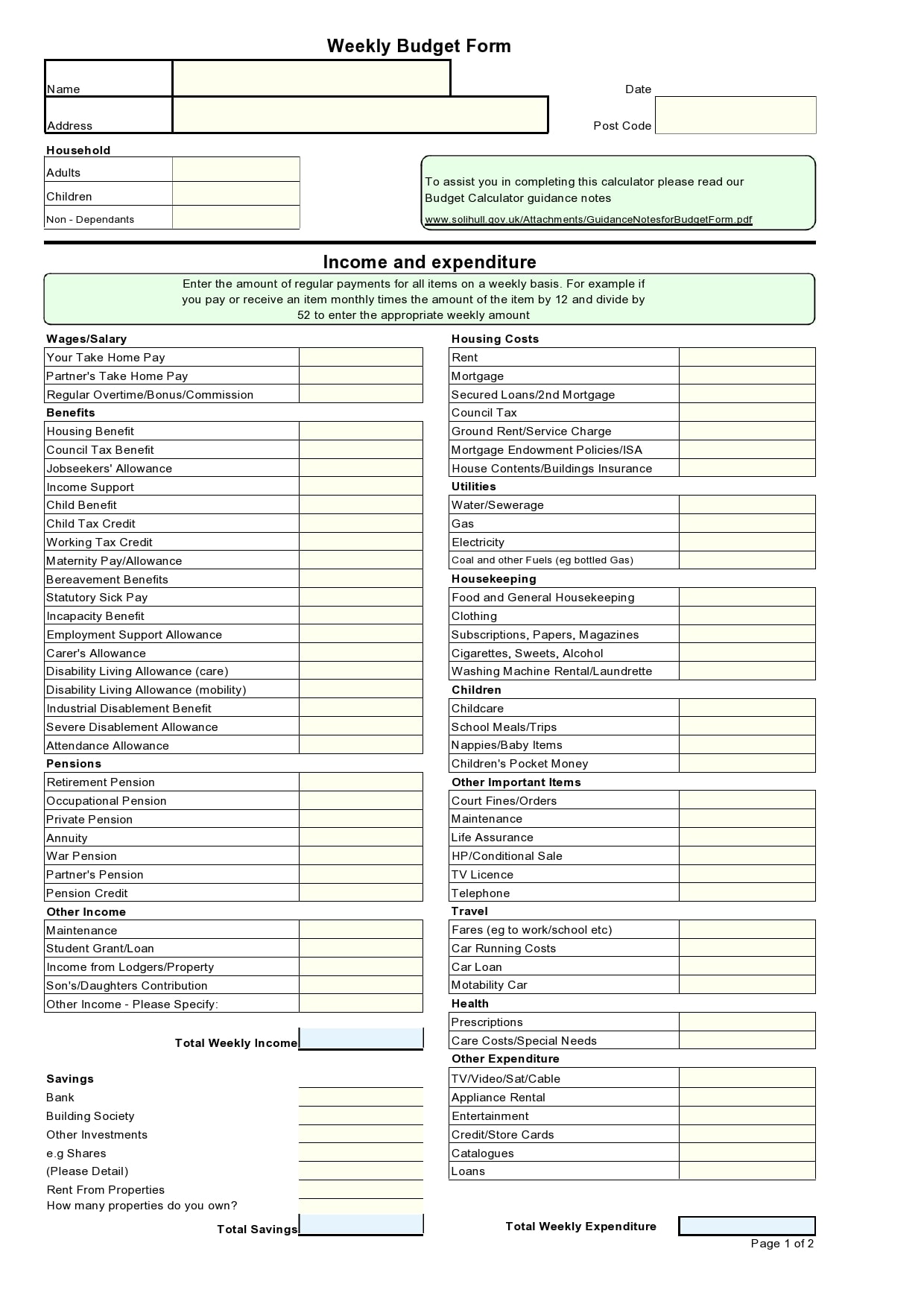

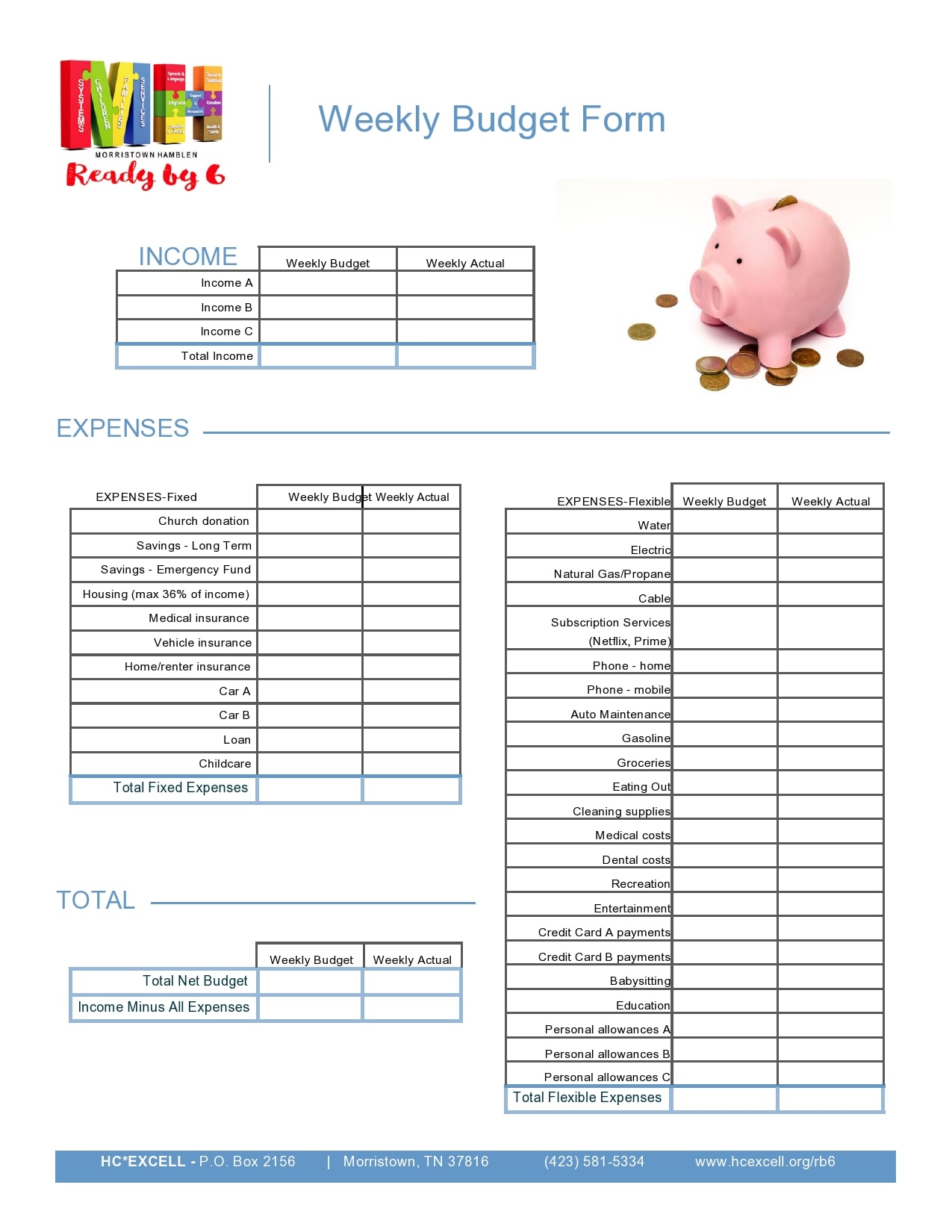

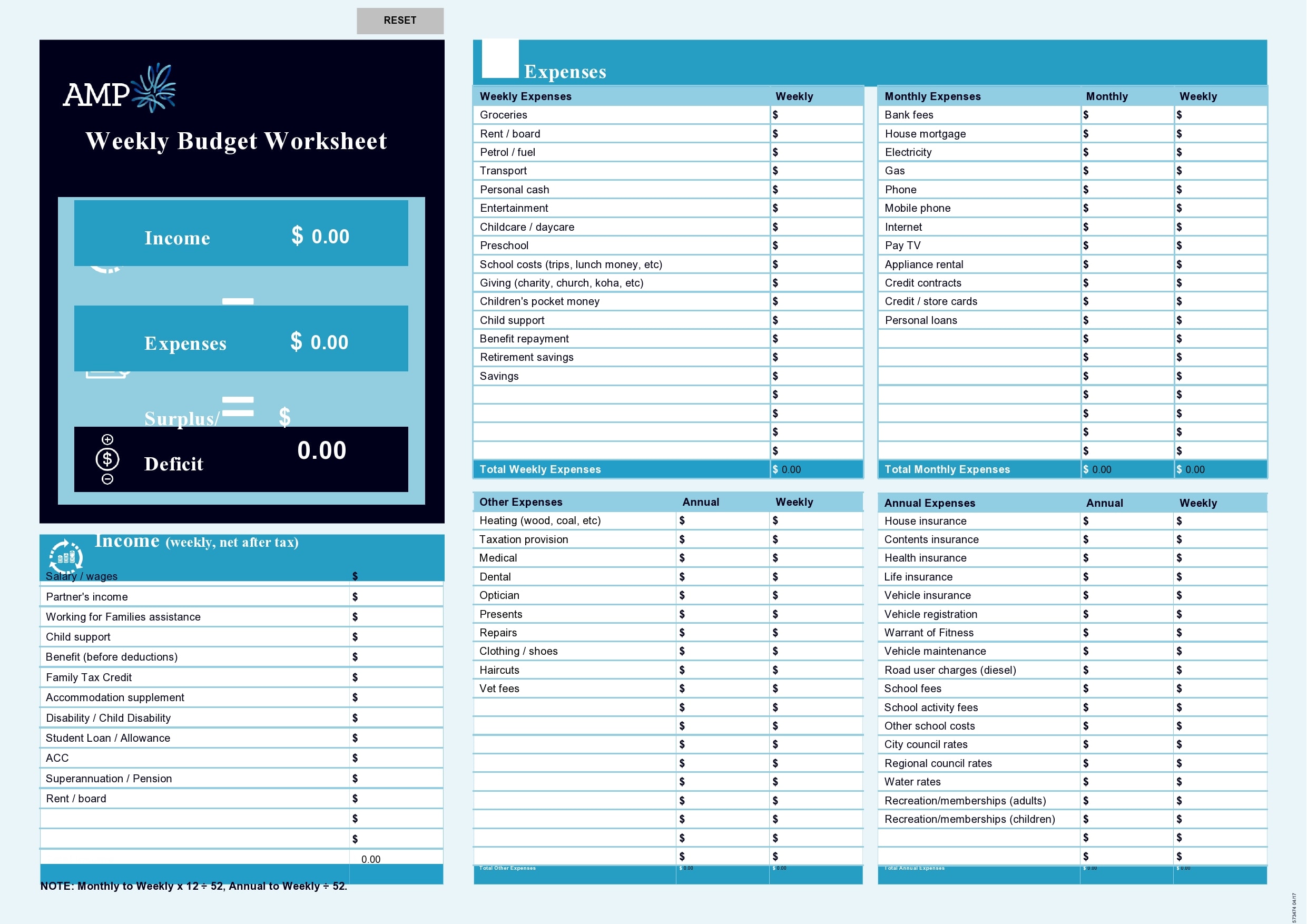

Weekly Budget Templates

Why do you need to make a weekly budget?

With the use of a weekly budget template, you can easily prioritize your expenditures and consequently manage your savings well. Here are some reasons why you need a weekly budget worksheet of your own:

- To control your budget

If you have the capability to keep track of your expenses, you can curb your urge to overspend. - To focus on saving

Using a budget template as a guide gives you a good idea of whether you’re on the path towards meeting your goals or not. - To control your expenditures

With this template as your constant reminder, you will control your expenditures better because it will provide with you an overview of your income and expenses.

By maintaining a weekly or bi-weekly check on our expenses and income, this greatly helps in the prioritization of your wants and needs. Moreover, the budget also helps you keep track of your finances.

Monitoring and planning your budget on a weekly basis enable you to identify and possibly eliminate unnecessary expenses. This makes it easier to achieve your financial goals. In addition, a weekly or review of expenditures reduces the stress caused by overspending at the end of each month.

Weekly Budget Worksheets

How do I create a weekly budget spreadsheet?

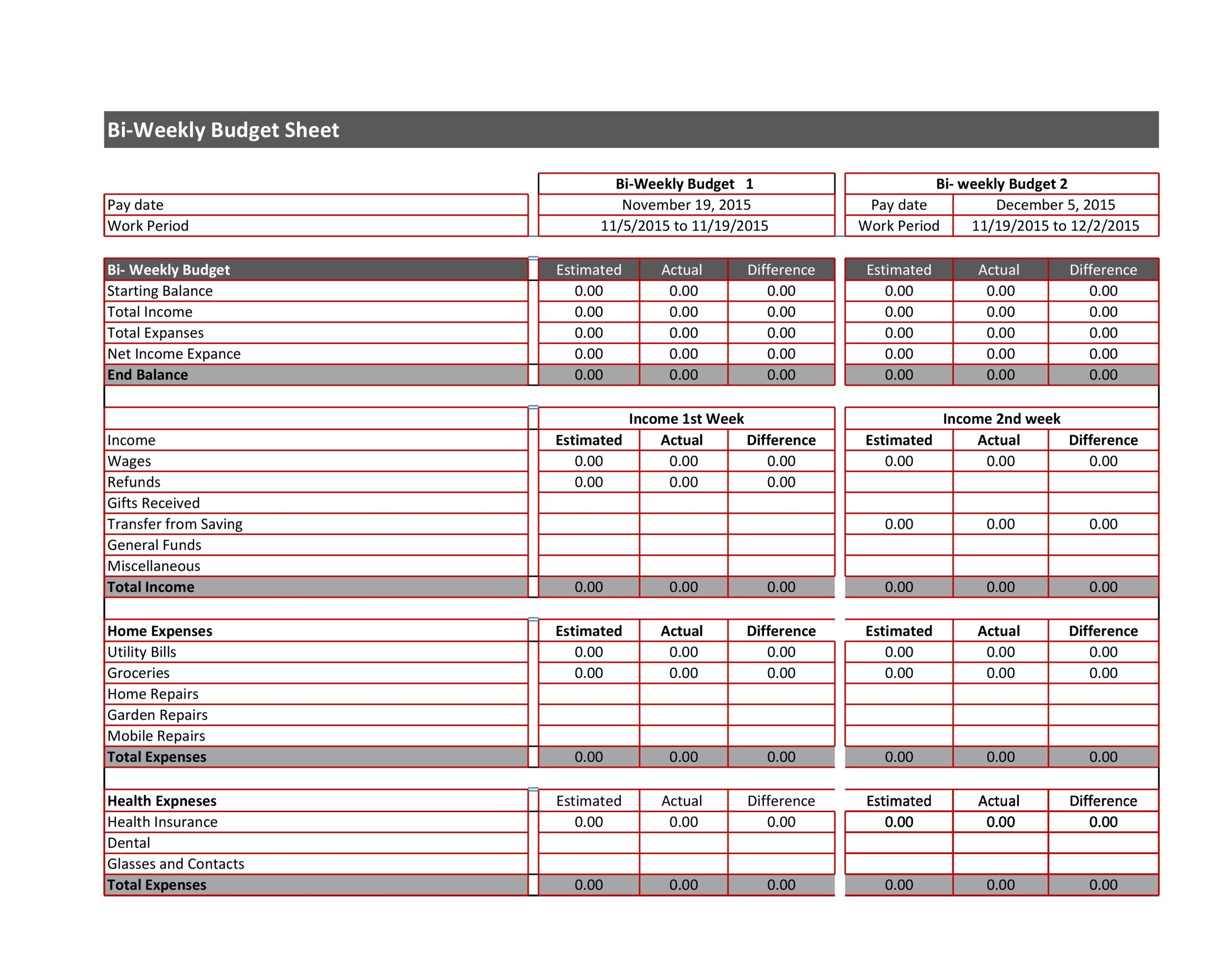

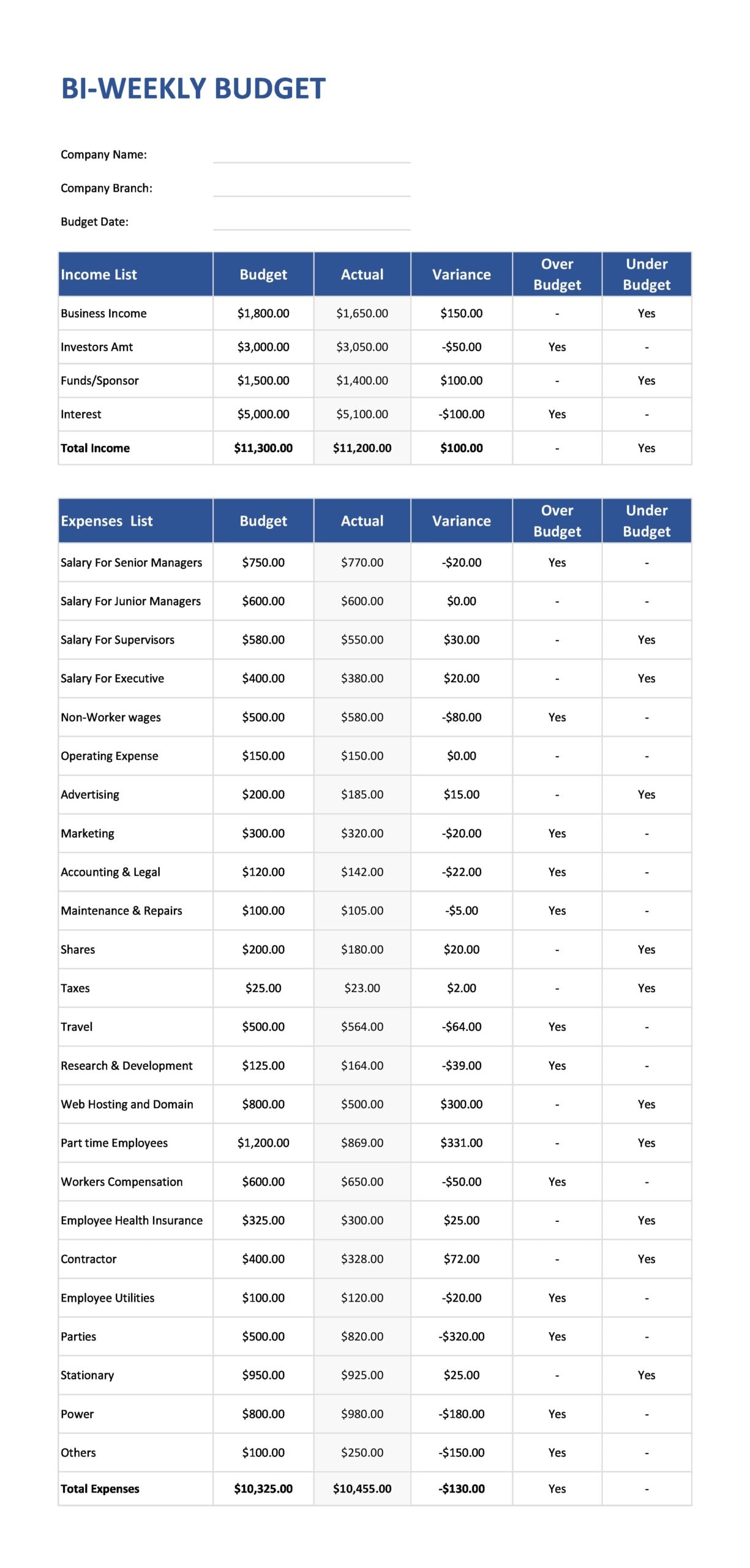

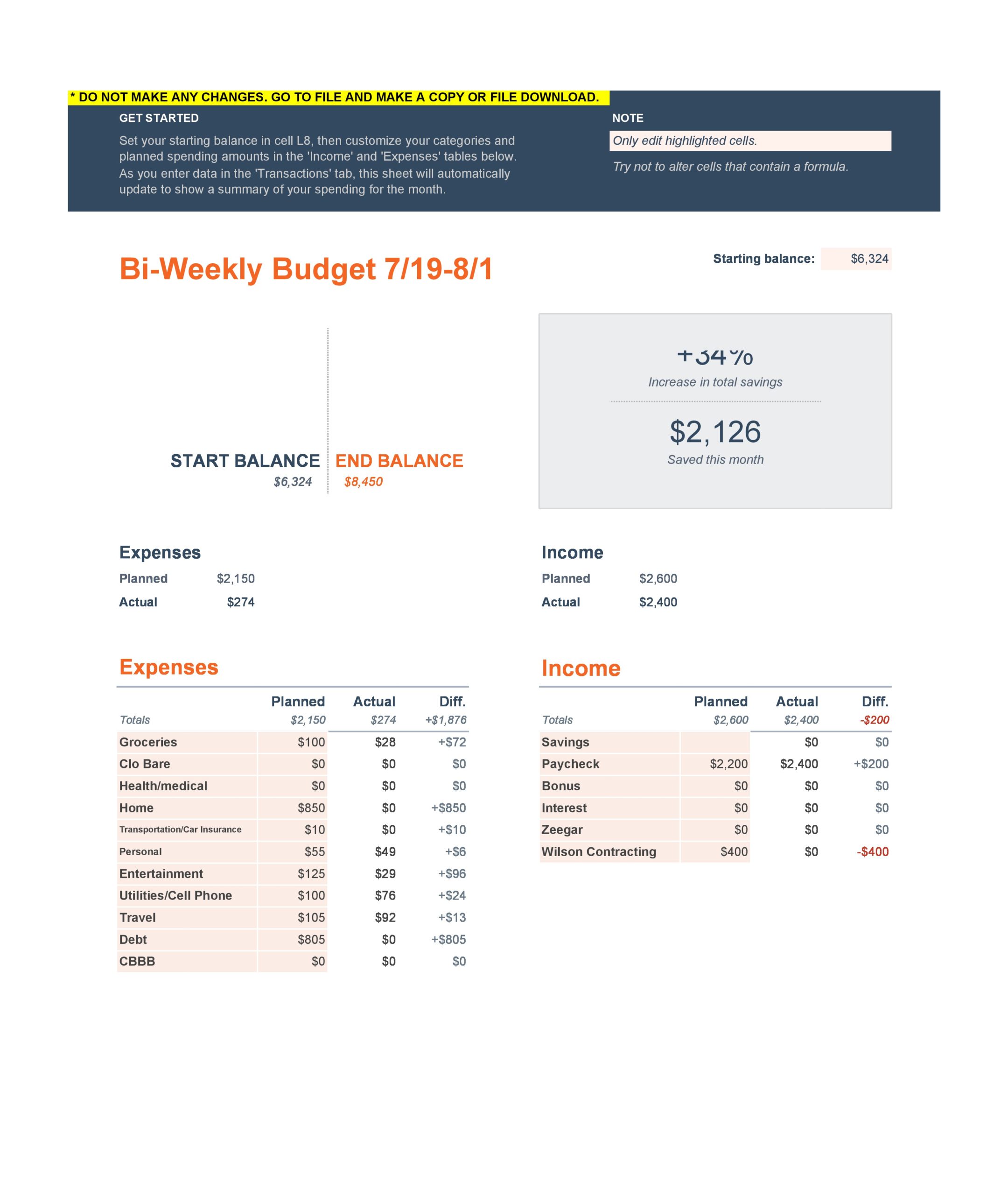

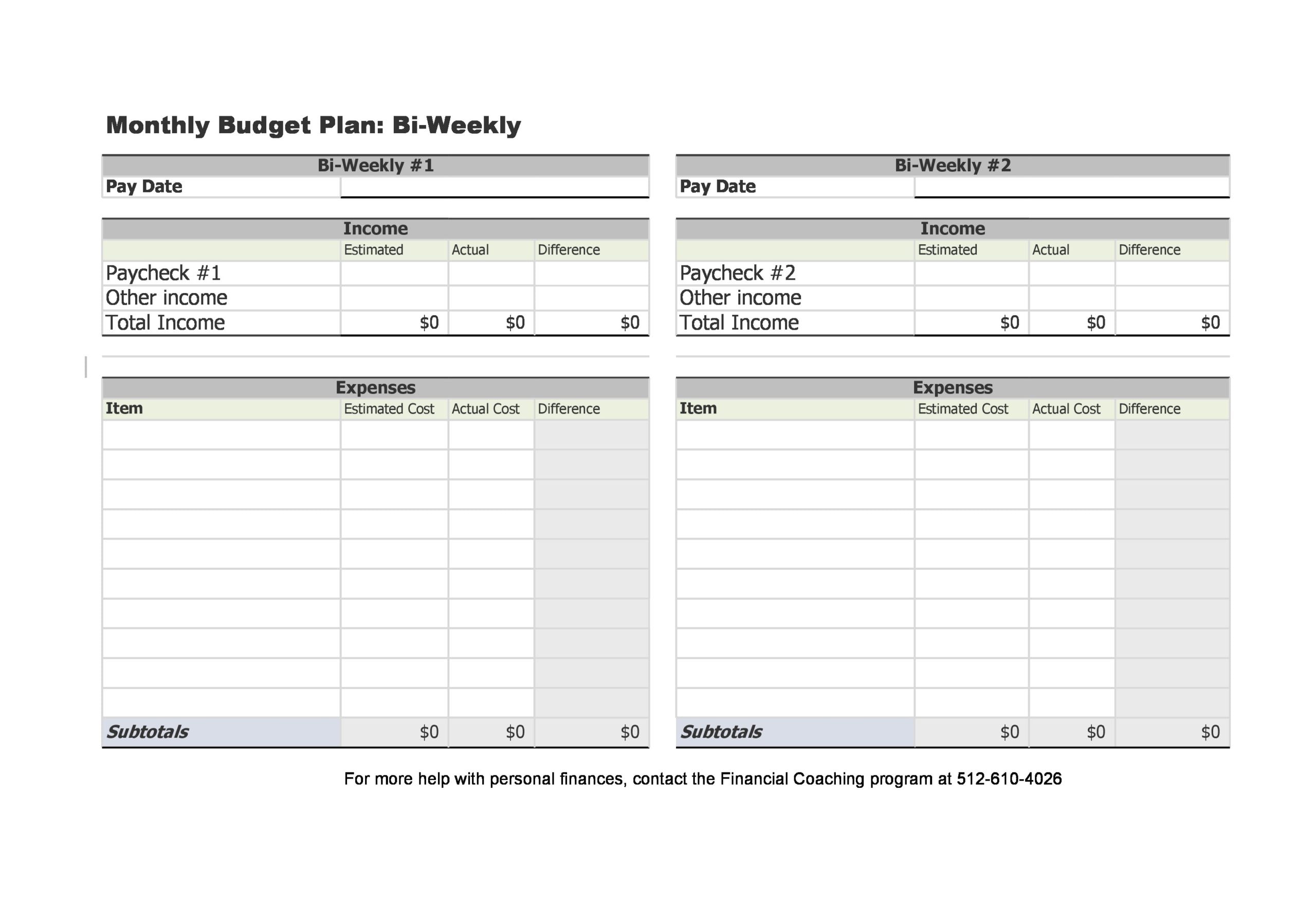

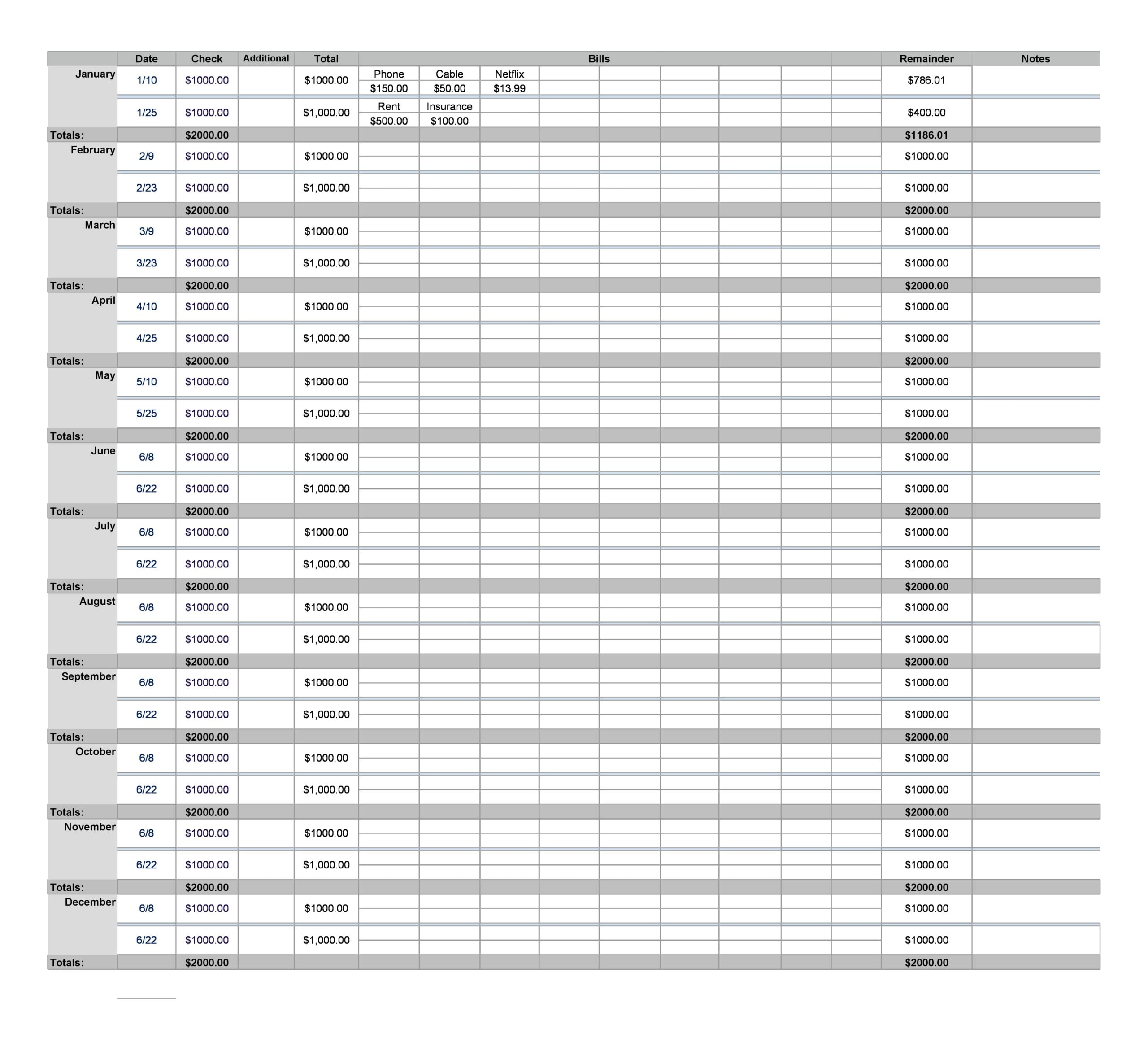

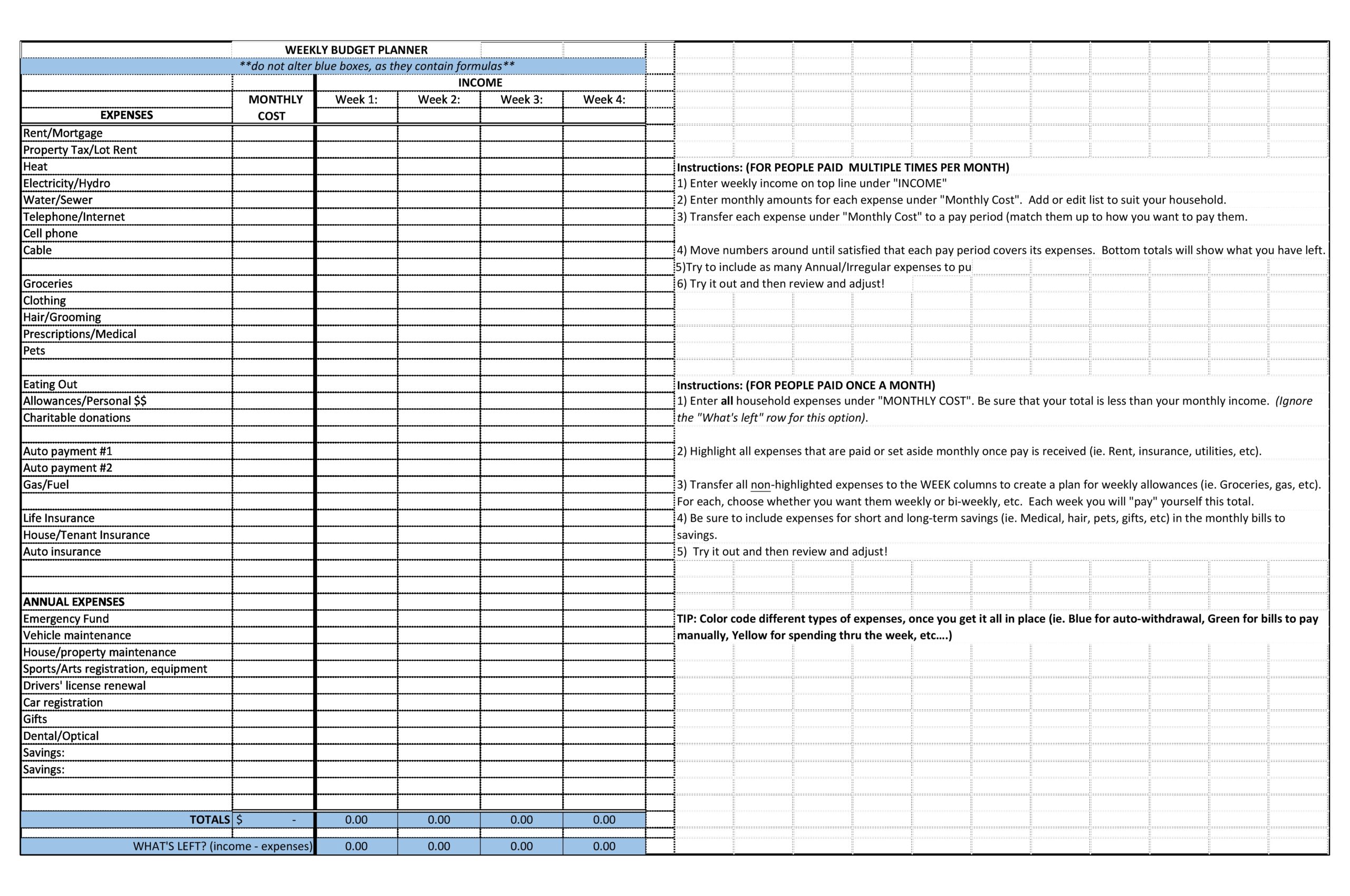

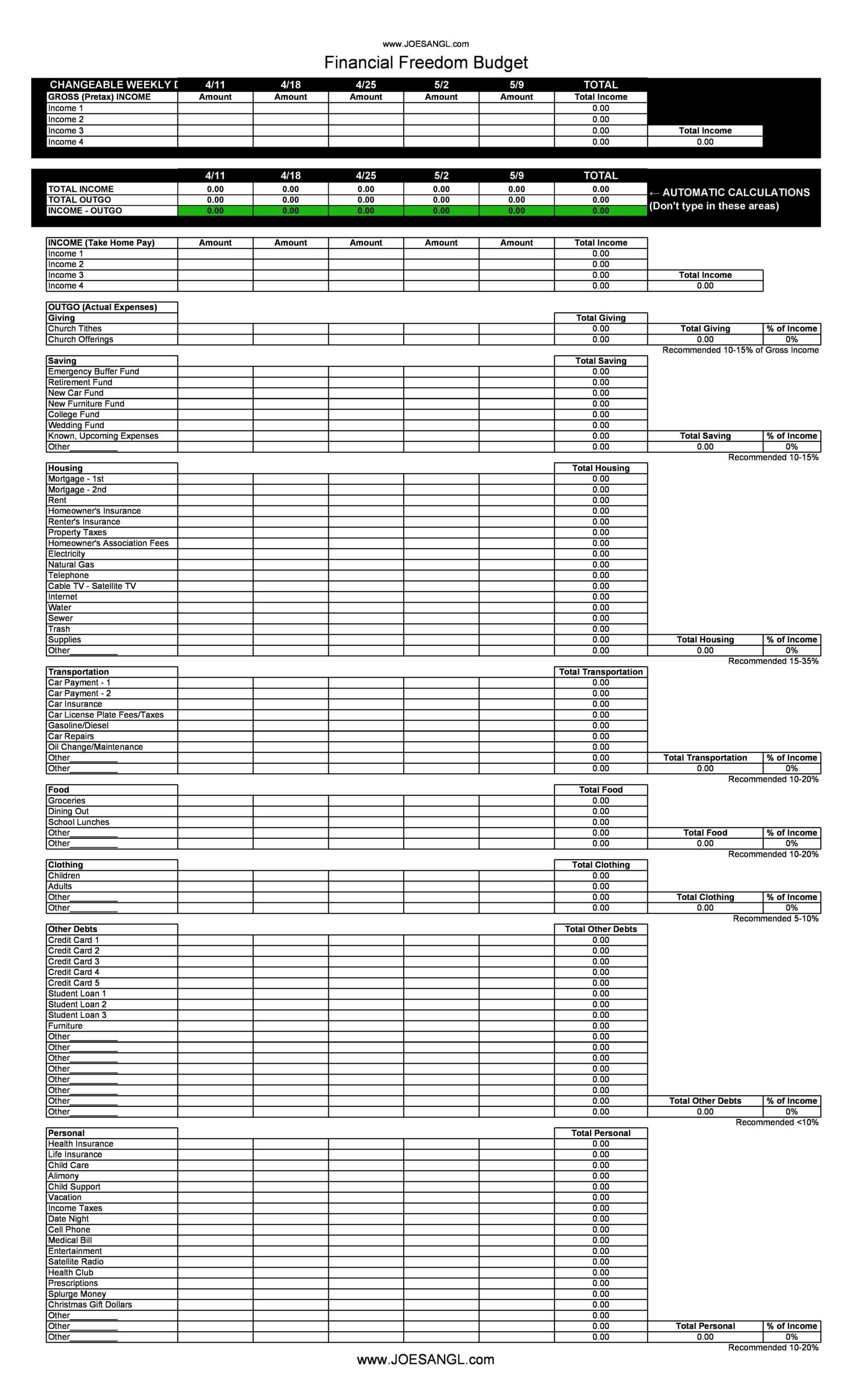

The best way to maintain your weekly budget template is by budgeting your paychecks separately. This way, you will determine what the money from each of your paychecks pays for. This means that it will be much easier to monitor your hard-earned dollars.

To help you create your weekly or bi-weekly budget template while monitoring your paychecks, follow these steps. Launch Excel and create a column for each the following:

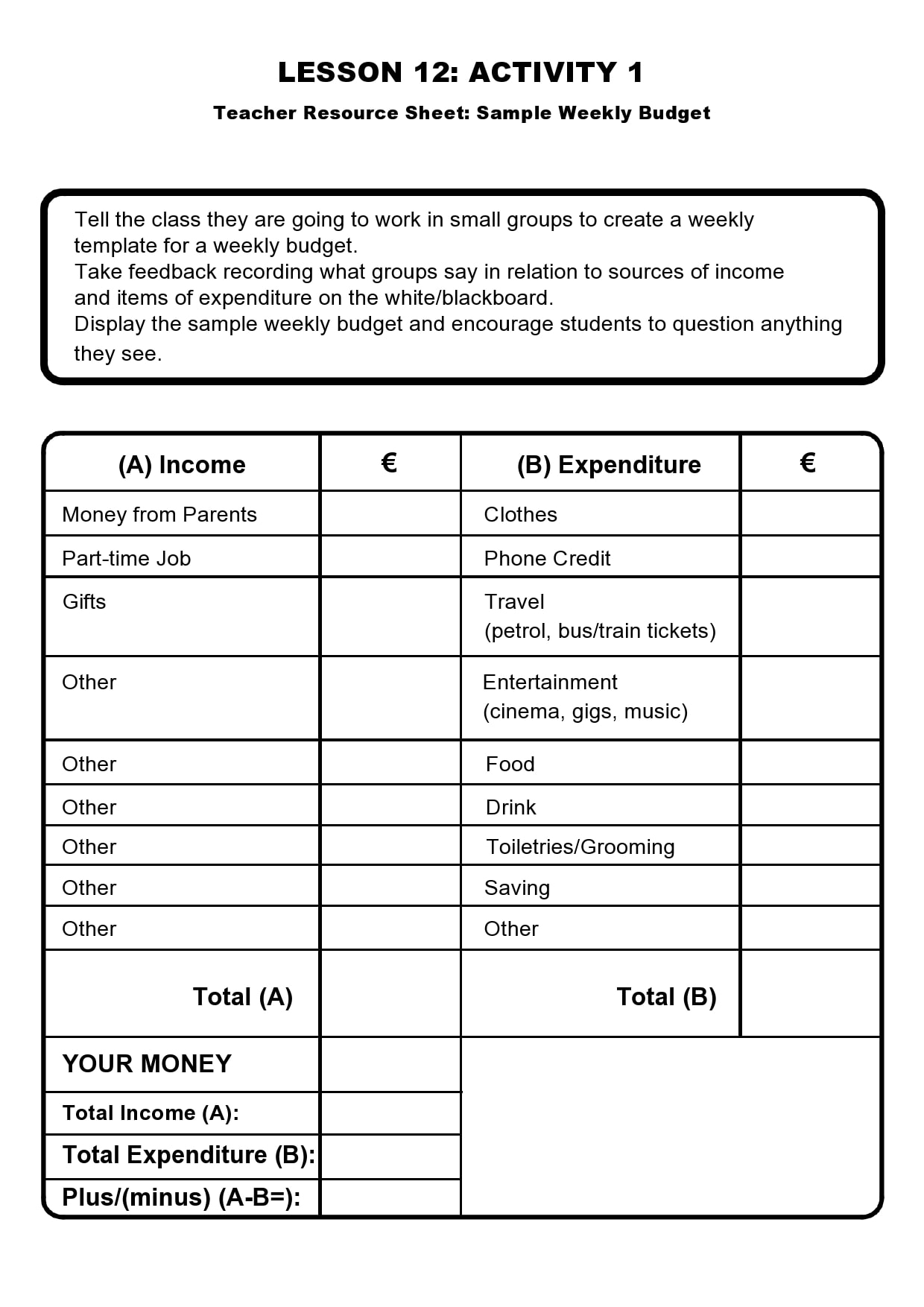

- In the spreadsheet, create an “income” column then input your expected income. List each of your paychecks separately in the different sections.

- Now, create an “expenses” column and write down all of the categories you usually spend your money on. Be as specific as possible. Entering vague categories makes it harder to monitor your expenses. When it comes to budgeting, here are some categories you may include:

Fixed Expenses:

Auto Insurance

Electricity

Health Insurance

Internet

Life Insurance

Mobile Phone Bills

Mortgage or Rent

Other Insurances

Subscriptions

Utilities

Variable Expenses:

Clothing

Date Night

Entertainment

Gas

Gifts

Groceries

Grooming or Haircuts

Household

Personal Allowance

Restaurants

Miscellaneous Expenses

This refers to a category for an expense that only occurs in the month you’re presently budgeting for or expenses that don’t occur regularly. - After listing your categories, input the amount that you estimate to spend for each of the categories in your “budgeted” column.

Weekly Budget Planners

How do you calculate weekly budget?

Making a weekly budget template has become an important part of our life to ensure that our finances are always kept in order. If you’re making a weekly budget planner for the first time, here are four helpful tips to make things easier for you:

- Try not to overcomplicate things

For some, making a budget is too tedious, especially if you think about how much math you have to do. While it is true that you need some level of math, you don’t have to be an expert in calculus to create and maintain an effective, working budget.

Start off with a simple, easy-to-follow formula – deduct your expenses from your take-home pay. The difference that you get from the take-home pay and the expenses will be your leftover that you may spend on leisure expenditures like watching movies, dining out, traveling, and so on.

However, if the difference turns out to be a negative value, this is a sign that you have to eliminate certain expenses to keep yourself in the positive. As soon as you have set up this simple formula, you may break it down and detail it as much as you need or want to. - Savings should be an automatic part of your budget

In many cases, people think of several excuses or reasons as to why they could not or did not set aside a specific amount every month into an account meant for savings. Whatever reason they have, whether they just “forgot” to or there was not enough money left, their savings account will never grow.

But if you want this account of yours to grow, set a part of your paycheck deposited into a savings account automatically. If your company has a retirement savings plan for employees, take advantage of this. Then make sure to contribute to it as much as you can, especially if your company matches a percentage of your monthly contribution. - Always pay your bills on time

To avoid sky-high interest rates on your outstanding debts, you should make sure to pay your bills on time each month and in full. This also helps you keep a healthy credit rating. Keep in mind that the lower your credit rating is, the harder it will be for you to get approval when applying for loans, including car loans, mortgages, and others.

You may also want to consider setting up a billing account on auto-pay so that there won’t be a need for you to remember when to make your payments and for which bills. Another option is to try out an app or tool for account management that reminds you when you have a due date for a bill coming soon. - Get an accurate estimate of your monthly expenses

Obviously, it would be very difficult for you to know just exactly how much you are actually spending if you do not add up each cent that you spend every month. It is a lot easier to determine how much you’re bringing home each month than how much you spend for the same period of time.

The latter requires far more work than the former. One way to determine how much you spend each month is by keeping every bill and receipt you get then input these numbers into a simple budgeting template or a budgeting spreadsheet. Doing this helps you visualize everything you spend and whether your take-home pay will cover all of your regular expenses or not.

")