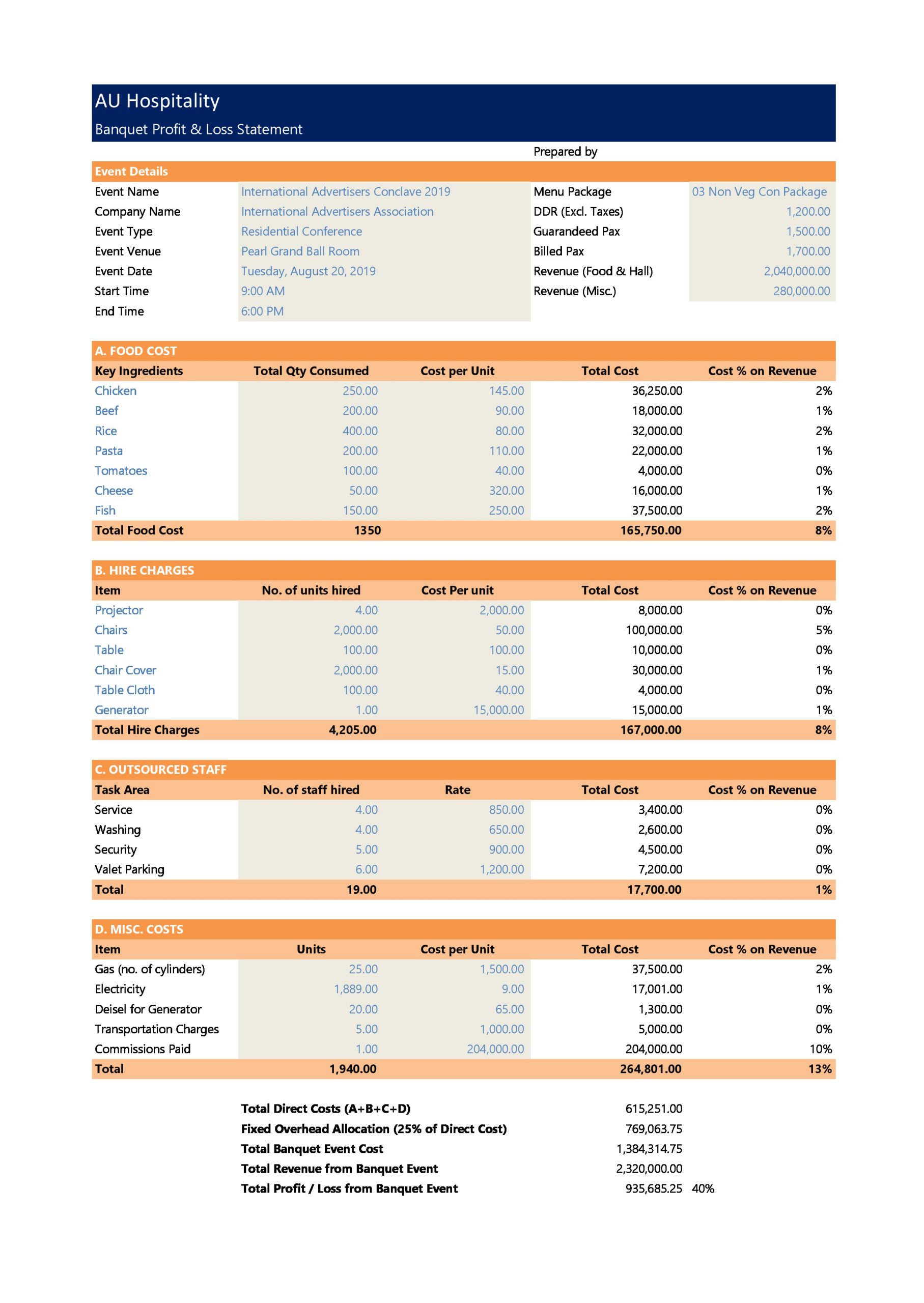

A profit and loss template is a financial document that contains a summary of the costs, expenses, and revenues incurred for a certain period. A profit and loss statement template is a lot like an income statement since it also provides information about the ability (or inability) of a company to generate profit.

Contents

Profit and Loss Templates

What is a profit and loss document?

A profit and loss template which is also known as a P&L template or income statement is a financial document which provides a rundown of a business’ expenses, revenues, and losses or profits over a specific time period. A sample profit and loss statement show the ability of a business to create profits, generate sales, and manage expenses.

You would prepare a profit and loss statement template based on the principles of accounting which include the recognition of revenue, accruals, and matching. Doing this makes this statement different from cash flow statements. The P&L template of a business gets portrayed over a certain period of time, usually a fiscal month, quarter or year.

When creating this template, there are certain categories you should include to make your statement effective. These categories are:

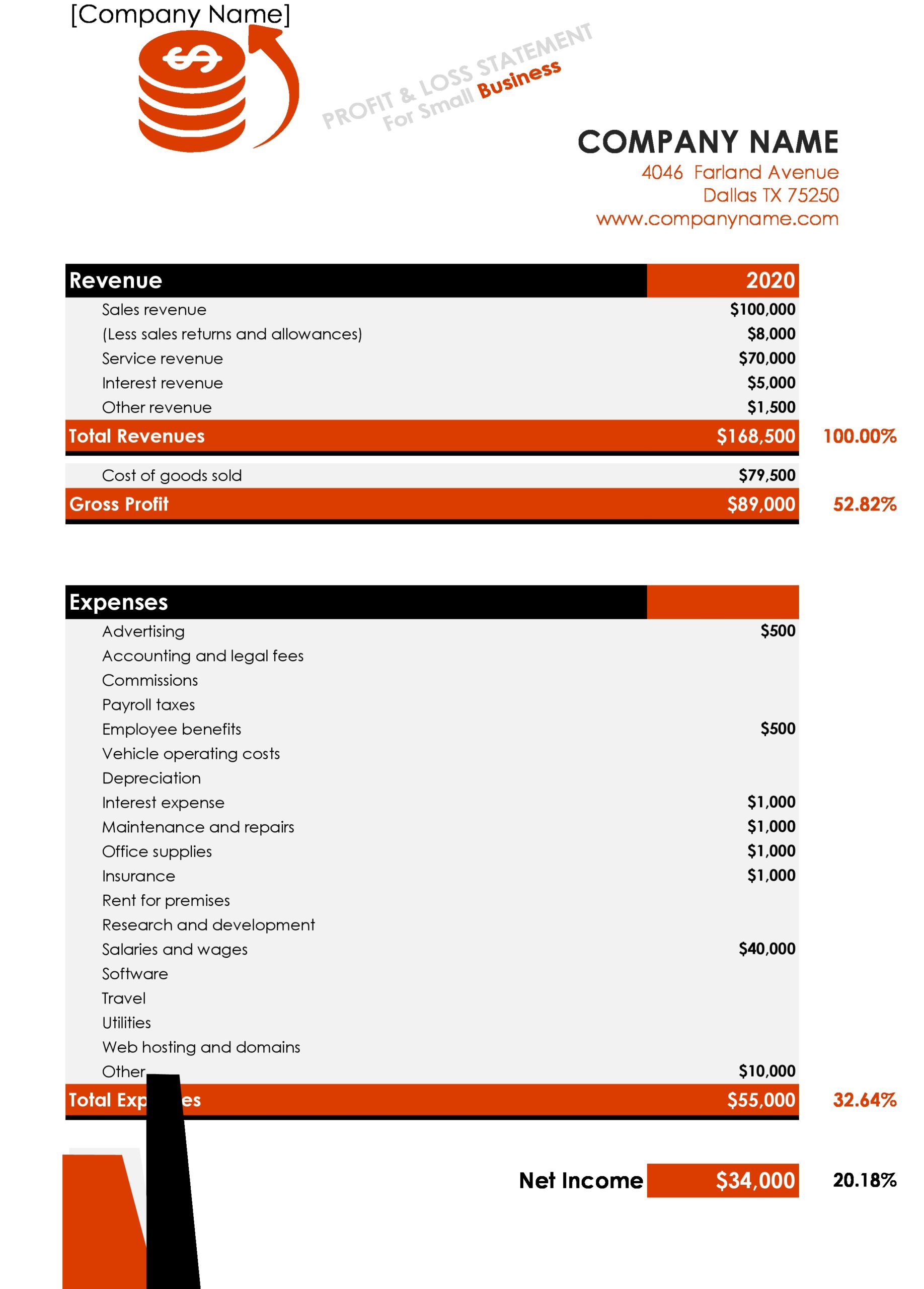

- Sales or Revenue

- Cost of Sales or the Cost of Products Sold

- Selling, General & Administrative or SG&A

- Advertising and Marketing

- Interest Expense

- Technology

- Net Income

- Taxes

Profit And Loss Statements

When do you need a profit and loss template?

Creating a profit and loss template is an important part of any business. There are certain types of templates you can create depending on when you need to make them including:

- Periodic

All companies need to prepare a sample profit and loss statement periodically for their review. Therefore, you should create such a statement at least once every quarter. Reviewing this statement helps businesses make decisions and for the preparation of a business tax return.

A business tax return is another financial document which uses the information from the profit and loss template as its basis for when you need to calculate net income so you can determine how much income tax your business should pay. - Pro Forma

New businesses need to come up with a profit and loss statement template at the startup phase. This type is “pro forma” which means that it’s projected into the future. Businesses may also need this type of statement as part of the application for funding when planning a new business project.

Preparing for your profit and loss template

A profit and loss template show how much profit a company made in a certain period. This is an important document for businesses because it illustrates whether the company made a profit or not – and this is one of the main objectives of most businesses.

A P&L template is also essential for other institutions. For instance, banks would like to find out if the company still generates profits to make sure that it can continue repaying its loan. Also, the government may want to find out the size of a company’s profit for the purpose of calculating taxes.

The document contains a summary of the company’s expenses and revenue for the time period. This is essential for the analysis of how money flows in and out of the business. The statement serves as a measure for the expenses and sales of the company during a specific time period.

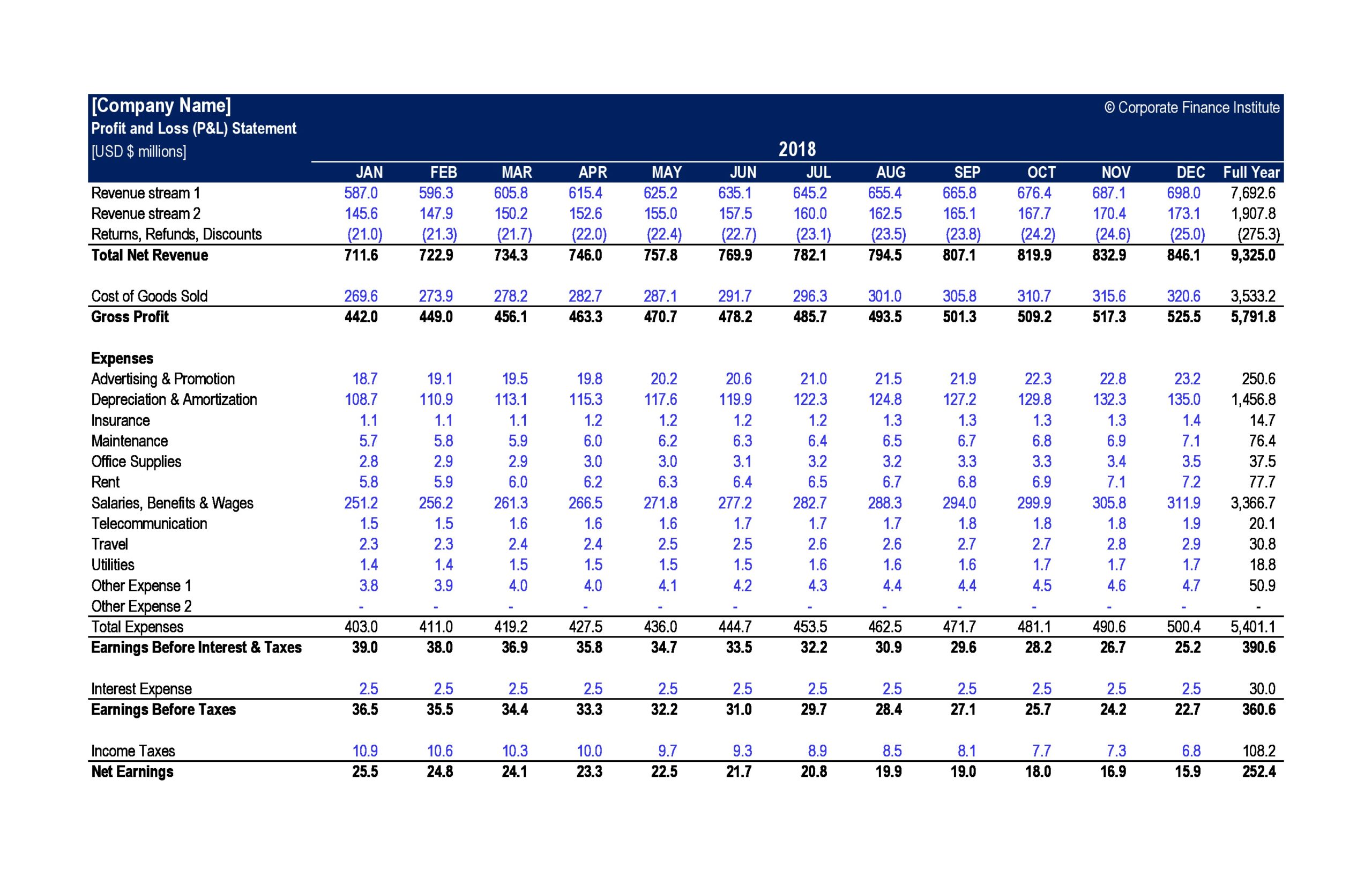

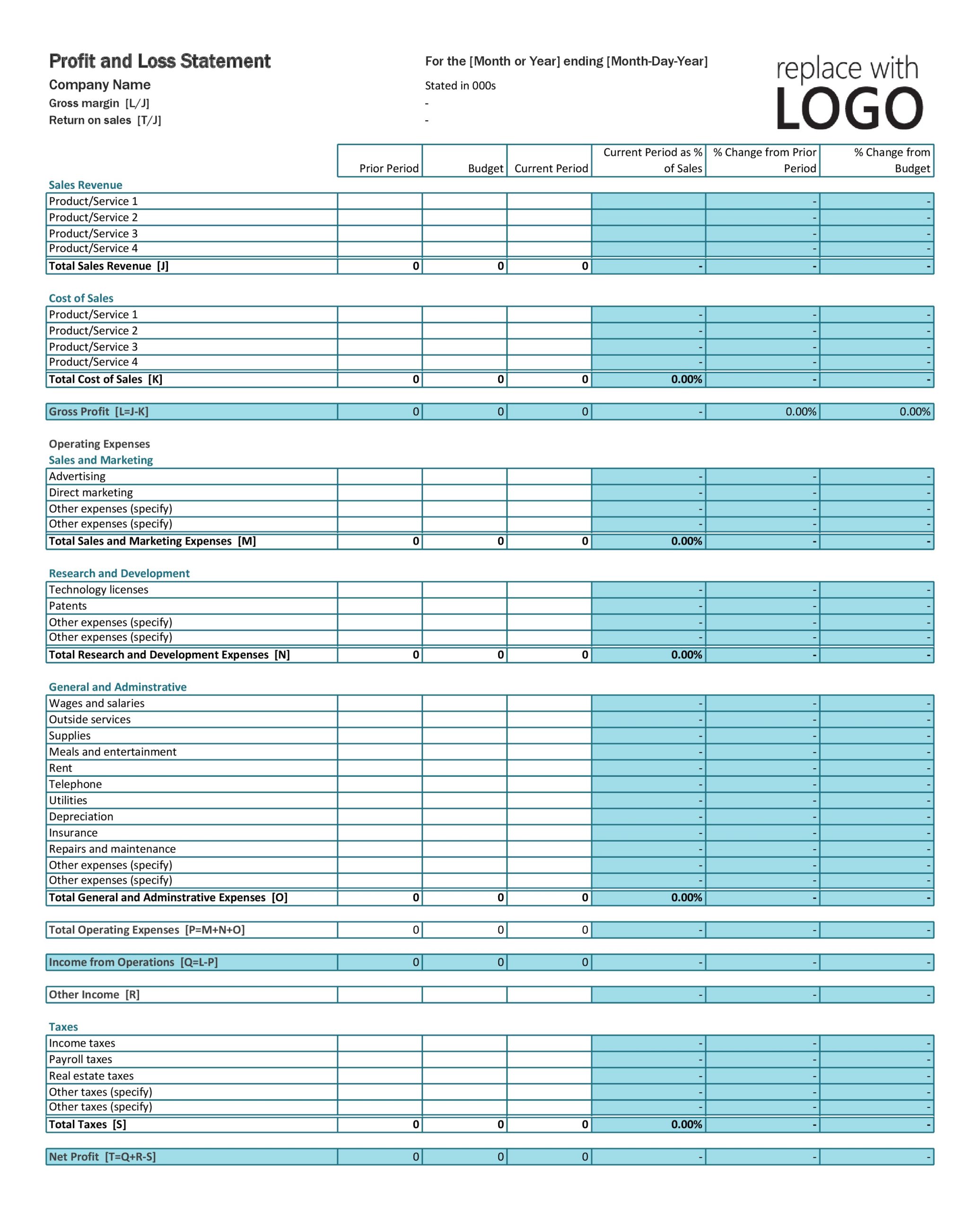

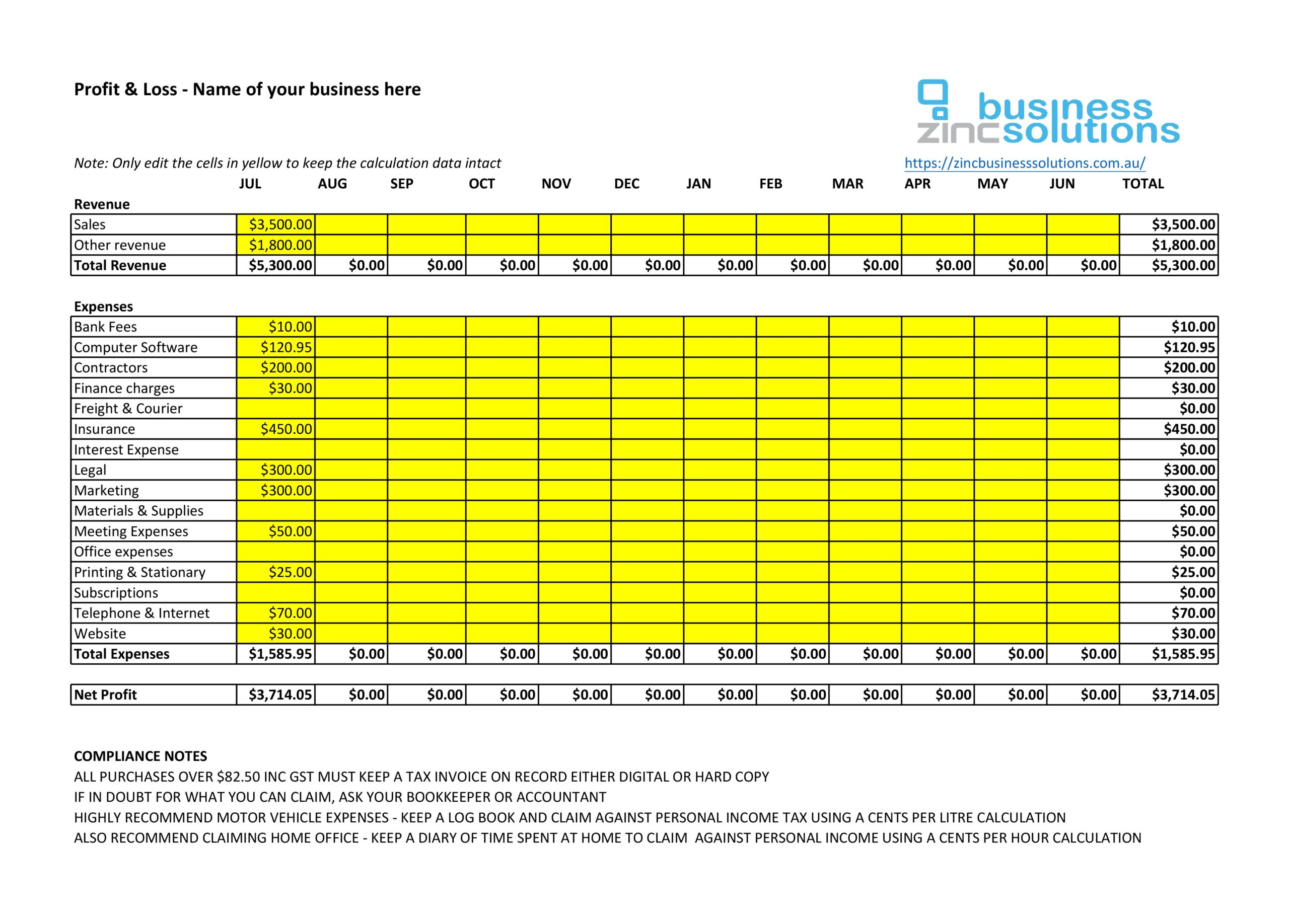

The function of this statement is to come up with a total number for all revenue sources then subtract all of the revenue-related expenses. It shows the financial progress of the company over the time period it covers. Because of this, the person in charge of creating this document must be very careful as it deals with financial information.

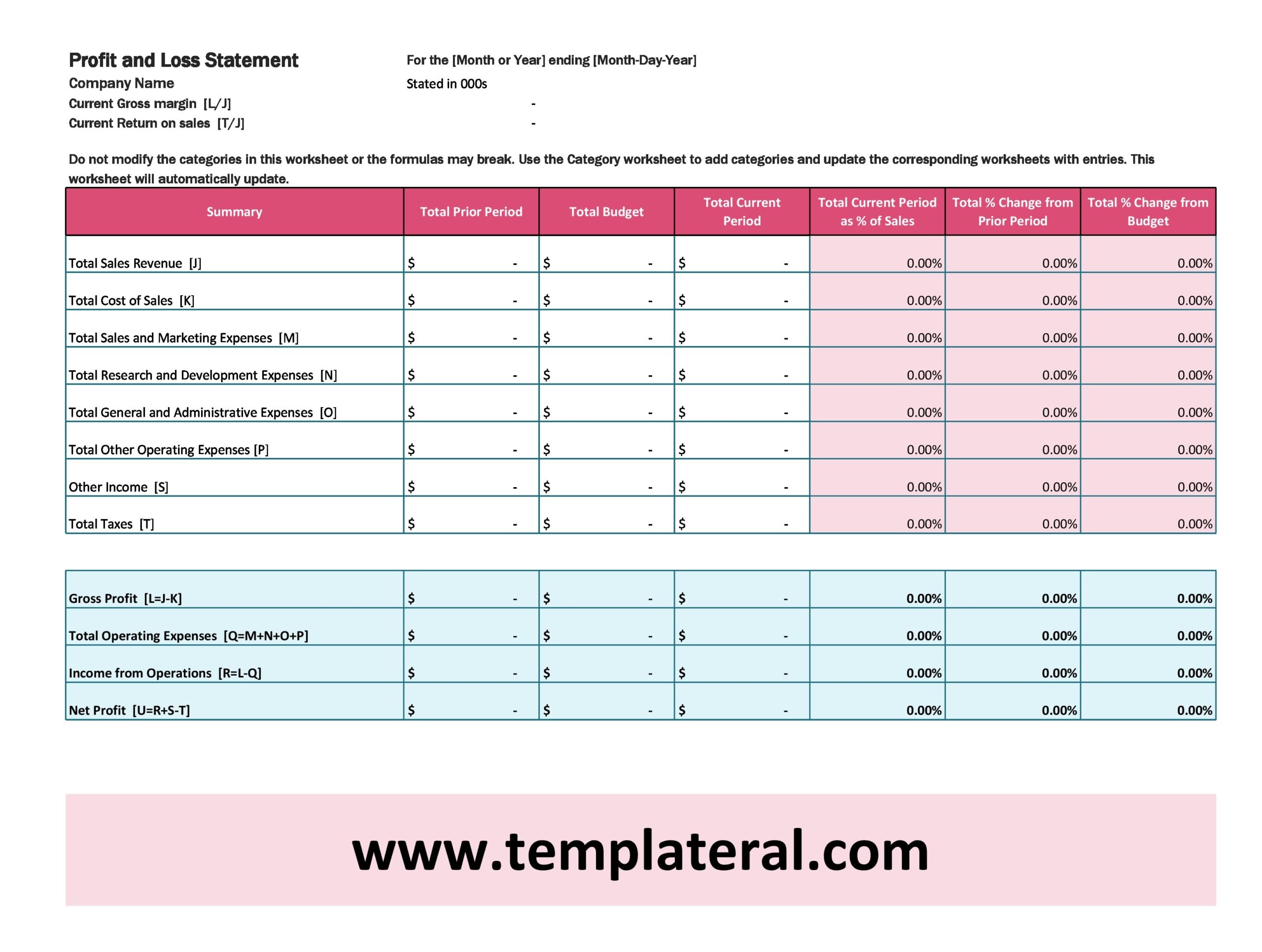

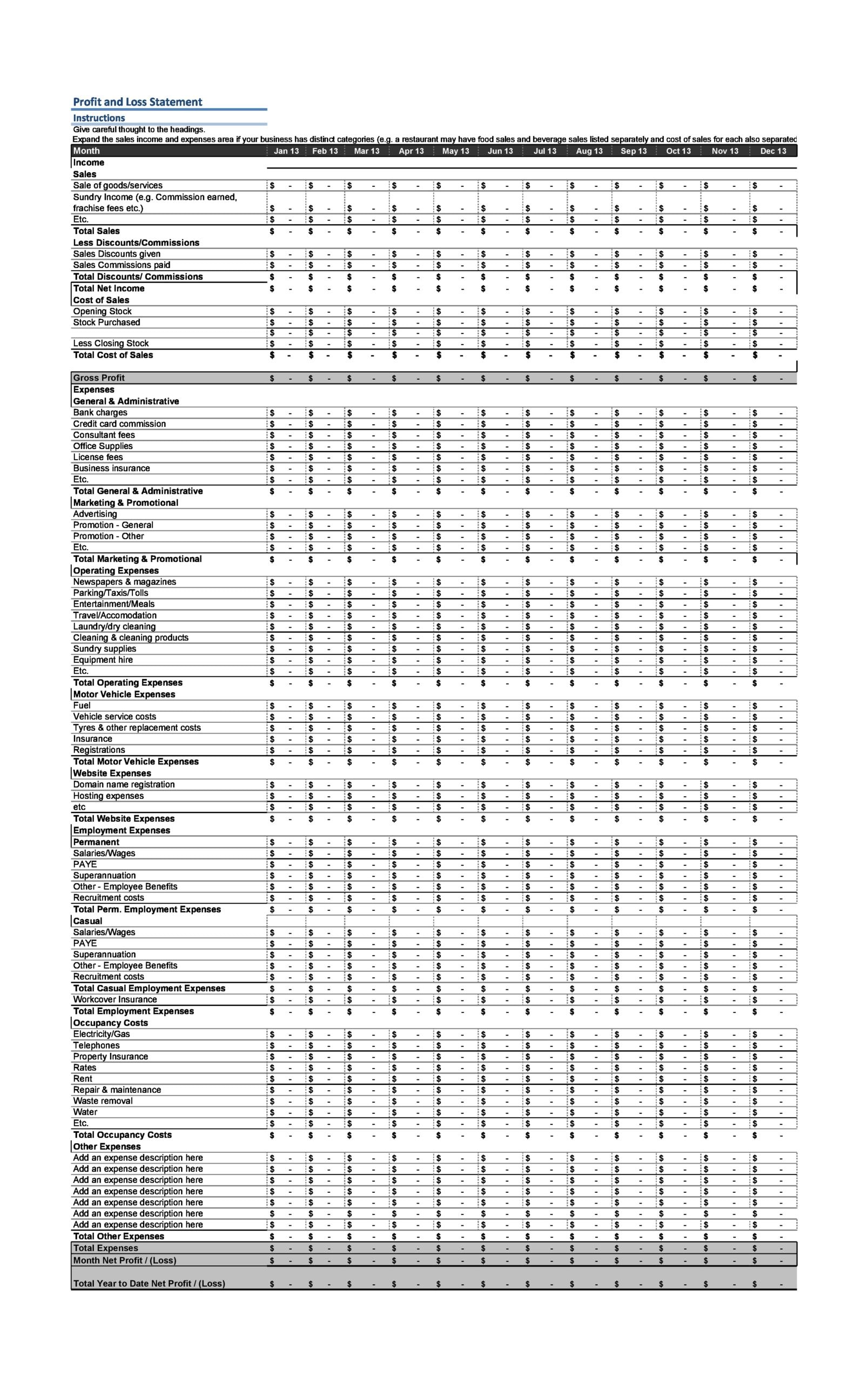

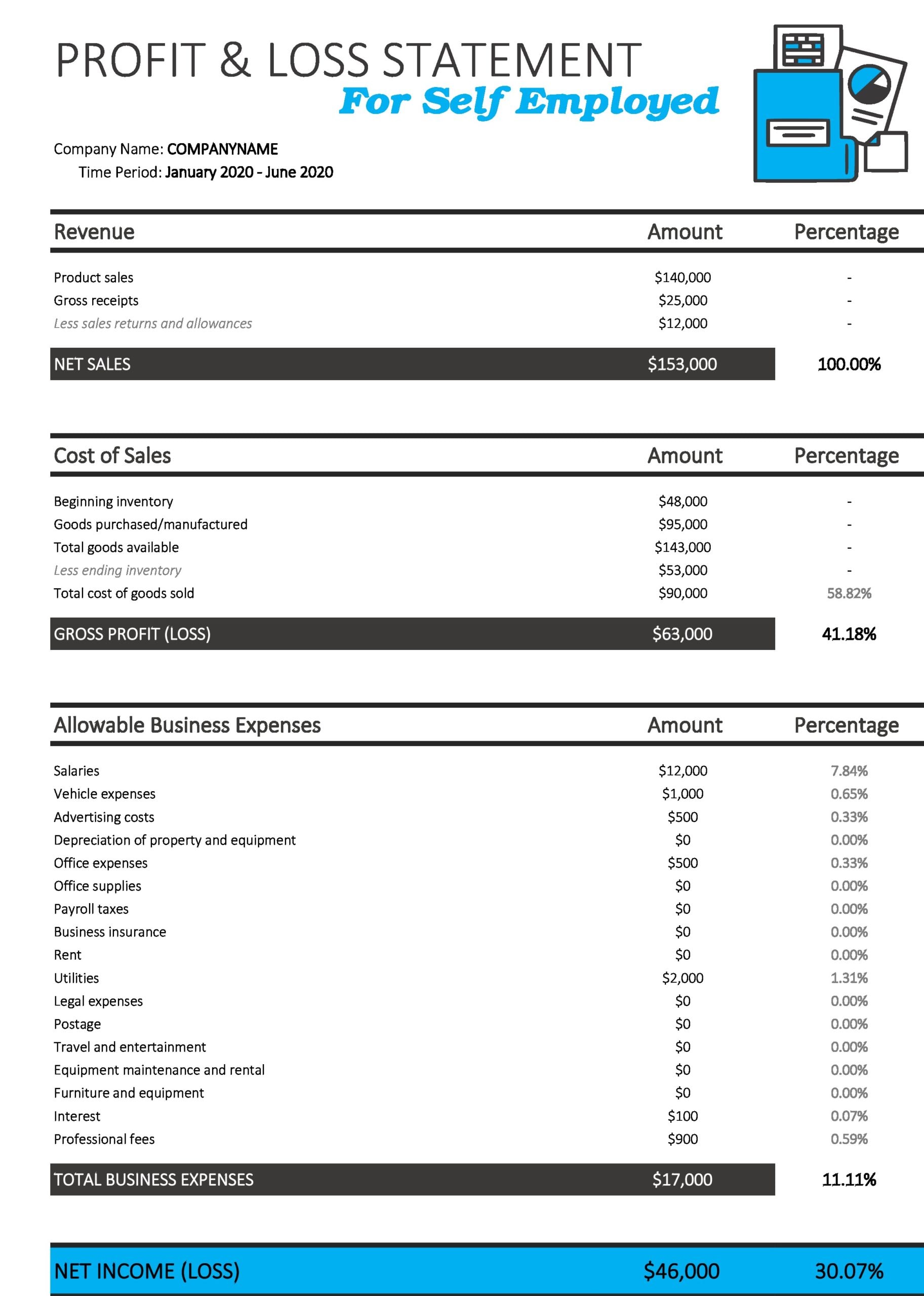

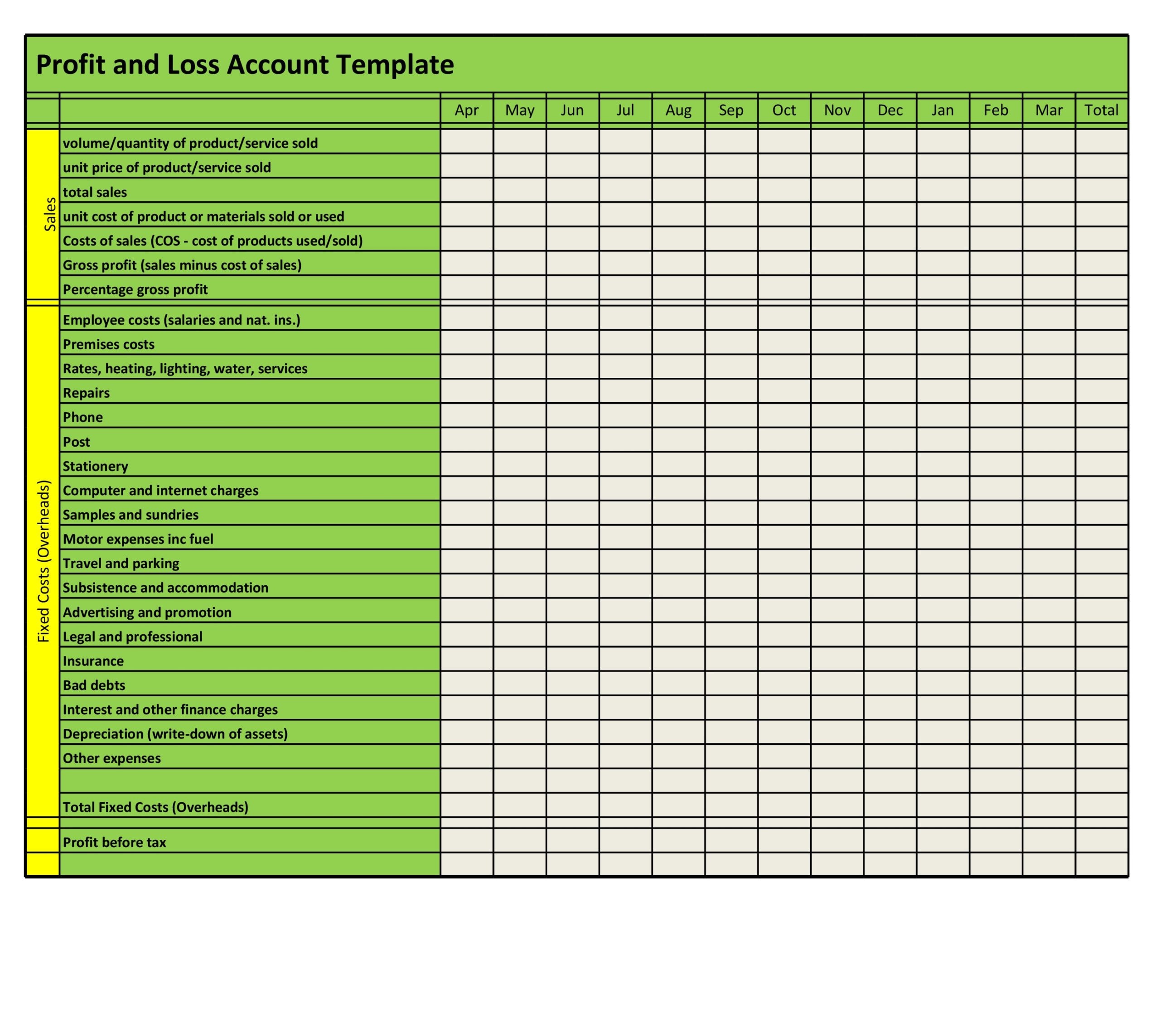

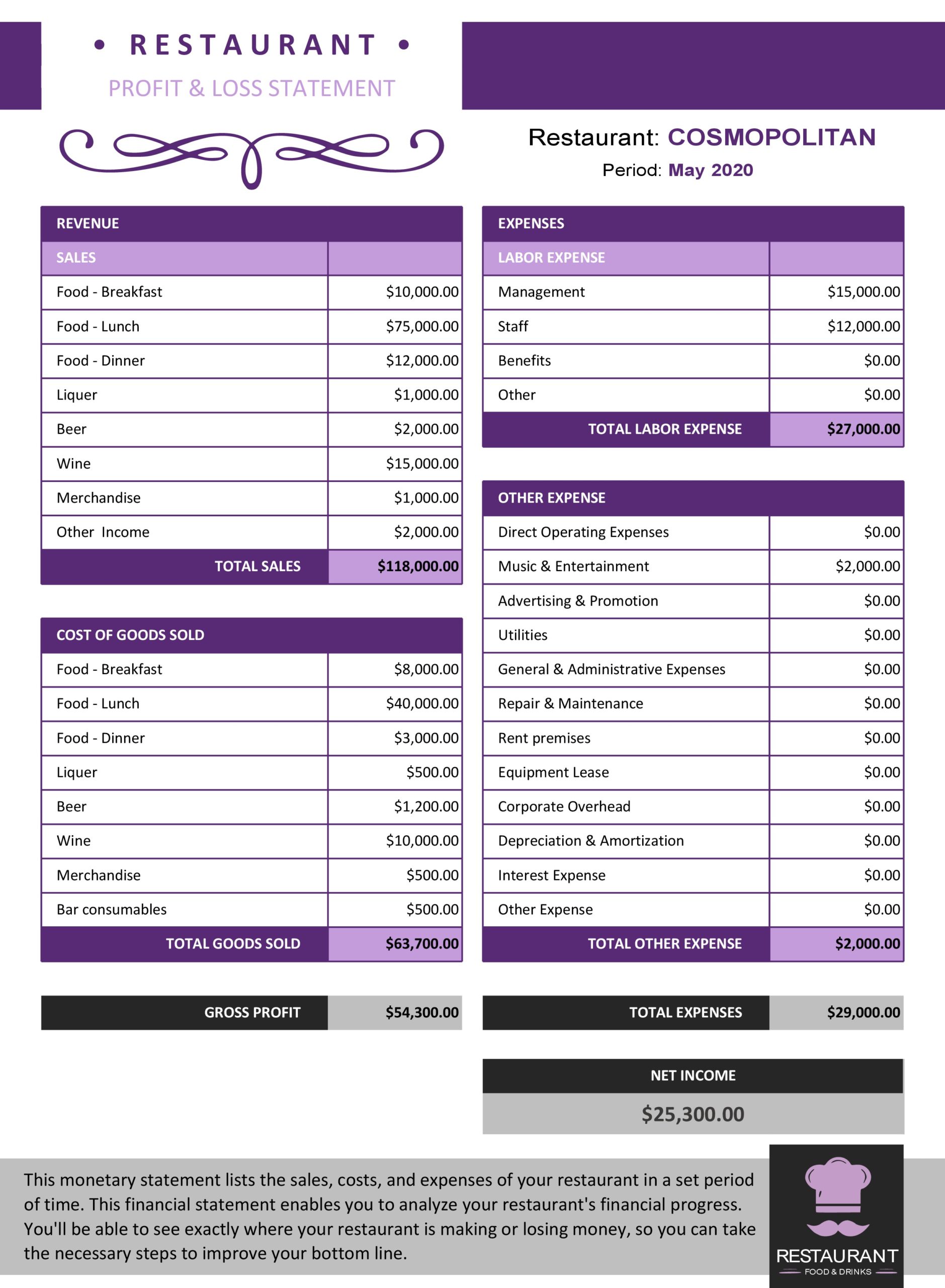

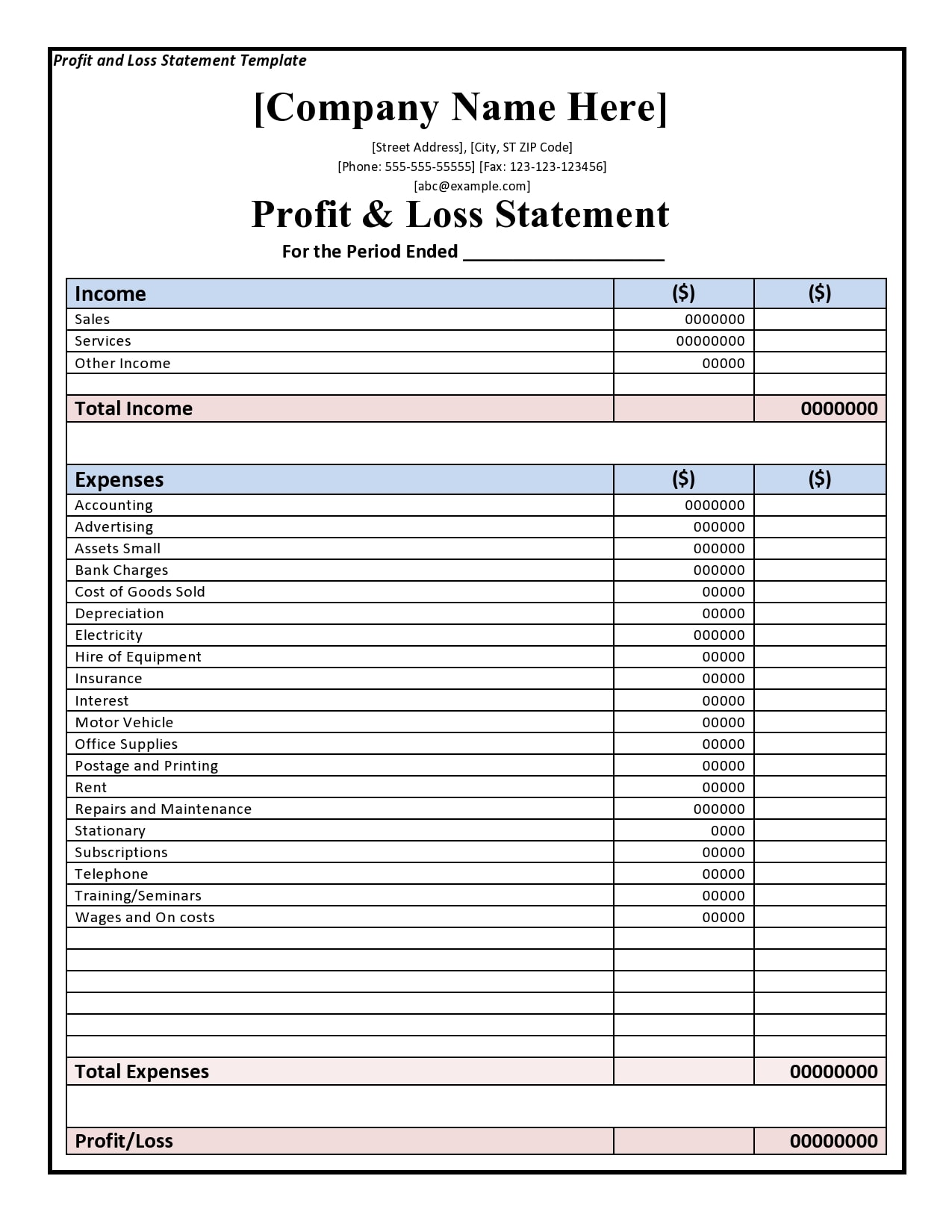

The statement includes uniform categories of expenses and sales. These categories include costs of products, net sales, administrative and selling expense, net profit, and gross margin. It’s important to use these categories when constructing the statement to ensure its effectiveness.

A sample profit and loss statement also give you a better idea of the cash flow of your business. Before creating this document, you need to prepare all the information needed for it. That way, you would have all the required information on-hand to make the process flow smoothly from start to finish.

If you want to create an effective profit and loss statement template, you must make sure that the reported expenses and revenues during the specific given time period should match. That way, even the IRS will accept your document.

This means that the expenses your company incurred for the generation of your product’s sales must relate to the actual sales during the given accounting period. Although you may download a template to make the job easier for you, there are some questions you may want to ask yourself first. These questions are:

- Does the inventory method of your business allow you to come up with a reasonable calculation or estimation for the cost and quantity of goods sold during the given time period?

- Does your company possess any records of administrative and general expenses?

- Is it possible to separate the expenses related to selling from other kinds of expenses?

Profit And Loss Sheets

Creating your profit and loss template

Even if your new business doesn’t require money for the startup from a lending institution such as a bank, you still require a number of financial statements which can help you make the right decisions. By far, one of the most important financial statements to create is the profit and loss statement.

The P&L template shows the business’ expenses and revenues along with the resulting loss or profit over a fiscal month, quarter or year. Most of the data to include in this statement would come from the monthly budget or cash flow statement of your company’s first year.

The information may also come from estimated depreciation calculations which you can acquire from a tax advisor. In particular, you need:

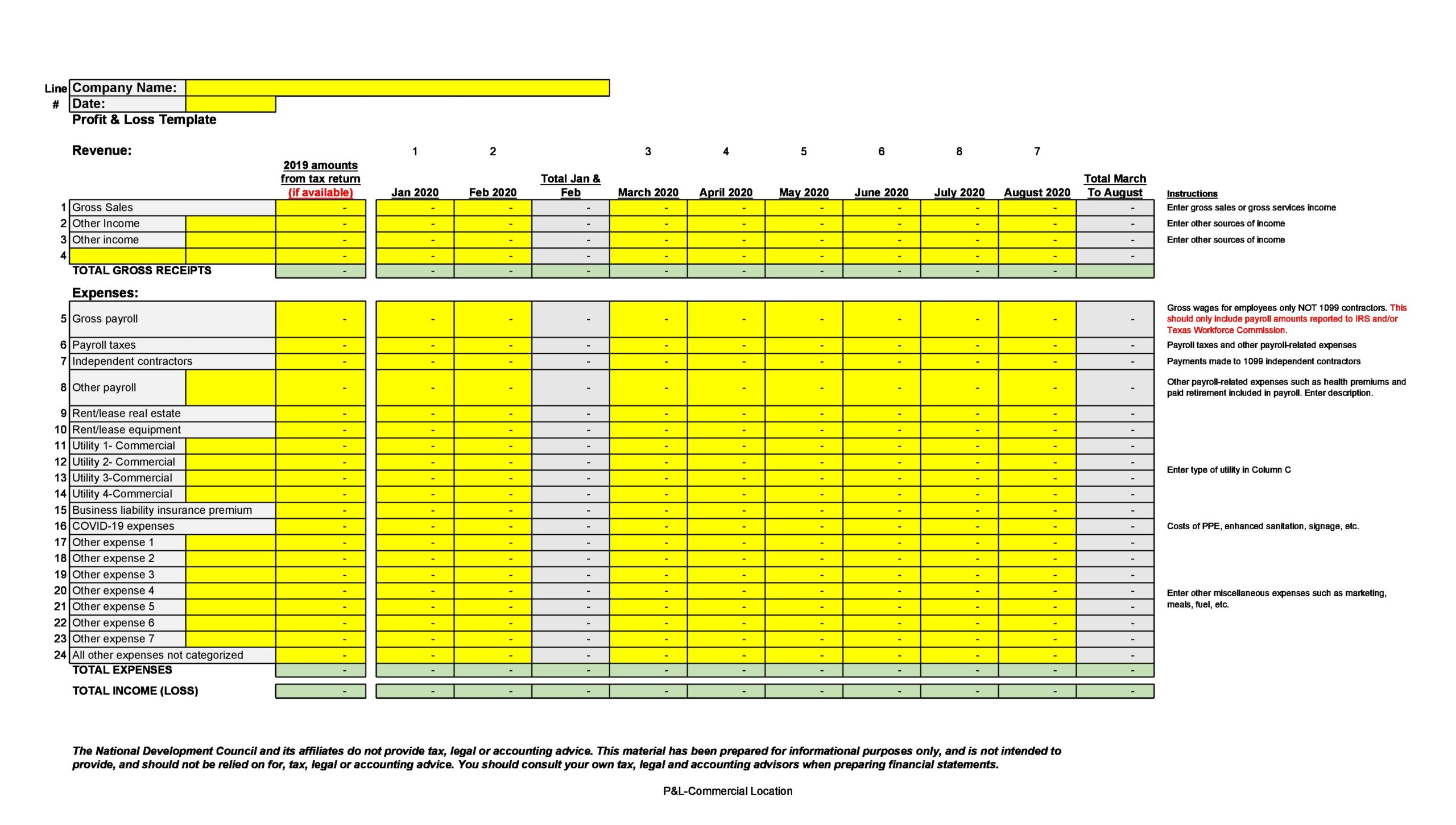

- The company’s transaction listing which contains all of the transactions of your company’s checking account along with all of the purchases you made using your company’s credit cards.

- Any other cash transactions along with petty cash transactions for which you possess the receipts.

- For the income information, you need a list of all your company’s income sources like credit card payments, checks, and so on. You can find all of this information on bank statements.

- You also need information about any sale reductions like returns or discounts.

If you plan to use a business accounting software, you can find this template under the standard reports. But even if you already have this statement in your company’s system, it’s still important to know what information you need to prepare it.

Make sure to include all cash transactions, both expenses, and income. If you use accounting software, you might still need to manually enter these cash transactions, including those for income and petty cash. Each time customers give you cash, use an invoice or a cash transaction form.

For any cash payments, make sure that you save each receipt. This is especially important for business meals and business driving expenses. The process of preparing for and gathering the information needed to make this statement is the same no matter what type of statement you need. Here are some steps to do this:

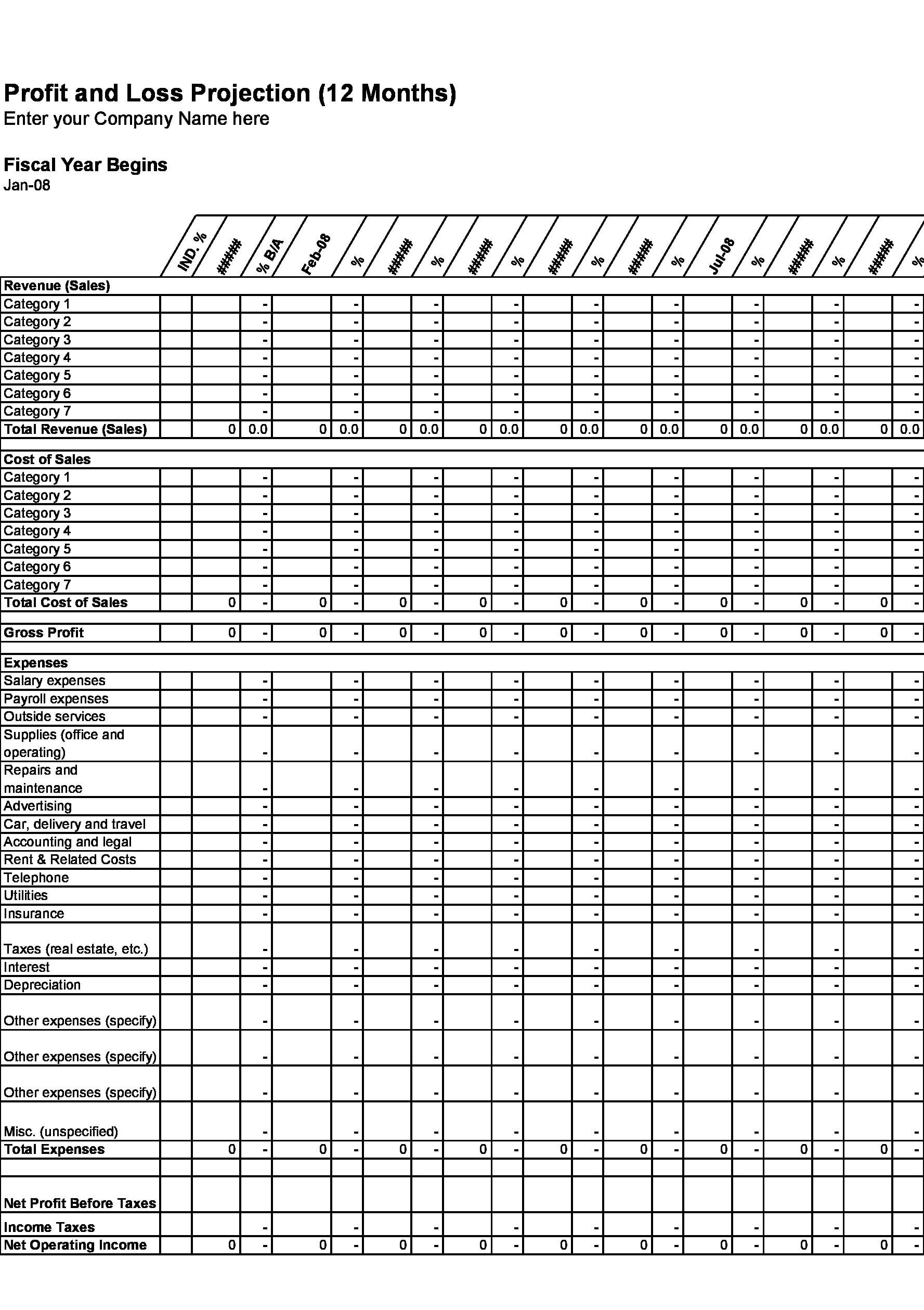

- First, show your company’s sales or the net income for each of the quarters of the fiscal year. You may break the income down into sub-categories to show your company’s income from all the different sources.

- Itemize each of the expenses of your business for each of the quarters. Show each of these expenses as a sales percentage. Make sure that the total of all these expenses should be 100% of the sales.

- Show the difference between expenses and sales as earnings. This step is sometimes known as earnings before interest, taxes, depreciation, amortization or EBITDA.

- Show the total interest of your company’s business debt for the fiscal year and subtract this from the EBITDA.

- Make a list of the estimated taxes on net income then subtract.

- Finally, show the total amortization and depreciation for the fiscal year and subtract.

The number you’re left with is your company’s net earnings or the profits (or losses) of your company.

If you’re starting a new business, you wouldn’t have actual information to create your statement. Therefore, you have to come up with good estimations. New businesses create pro forma statements each month during the first business year.

However, lending institutions might require you to create a statement for additional years or months to the projections to show your company’s break-even point when it starts generating a positive cash flow consistently. Here are the steps to follow:

- Make a list of all the possible expenses. It’s better to over-estimate the values and add a “miscellaneous” category.

- Come up with estimations for your company’s monthly sales. This time, underestimate the values and timings.

- Keep in mind that for a certain period of time, the difference between your expenses and sales would be a negative value. These negative values should accumulate to give you a better idea of how much money you need to loan for your business’ startup.