Some of us have experienced either asking for a guarantor or getting asked to be one as a requirement in the application for a personal loan. As a guarantor, you’re responsible for paying back a personal loan in case the borrower cannot. For the borrowers, it’s much easier to secure a loan with a guarantor. If you agree to become a guarantor, you may need a personal guarantee form.

Contents

Personal Guarantee Forms

What is a personal loan guarantee?

A personal guarantee loan is often likened to a person’s legal promise to pay back a credit issued to a business for which they serve as a partner or executive. Signing a personal guarantee form means that in a case where the business cannot pay back the debt, you will assume the responsibility for the remaining balance.

For credit issuers, having a guarantor sign a personal guarantee template provides them with a level of protection that assures them that they will get paid back. There are two main types of personal loan guarantees:

- Limited guarantee

This allows lenders to collect either a specific monetary amount or a specific percentage of the remaining balance from the business owner or the principal. Generally, this type applies when there are several principals who will pay portions of the loan or debt. - Unlimited guarantee

This requires that the principal gets liability for the whole remaining balance. Personal guarantees required by the SBA usually fall under this type. If a business or person cannot fulfill their obligations on a loan with an unlimited personal guarantee, then the creditor can reach out to the principal to get the remaining balance.

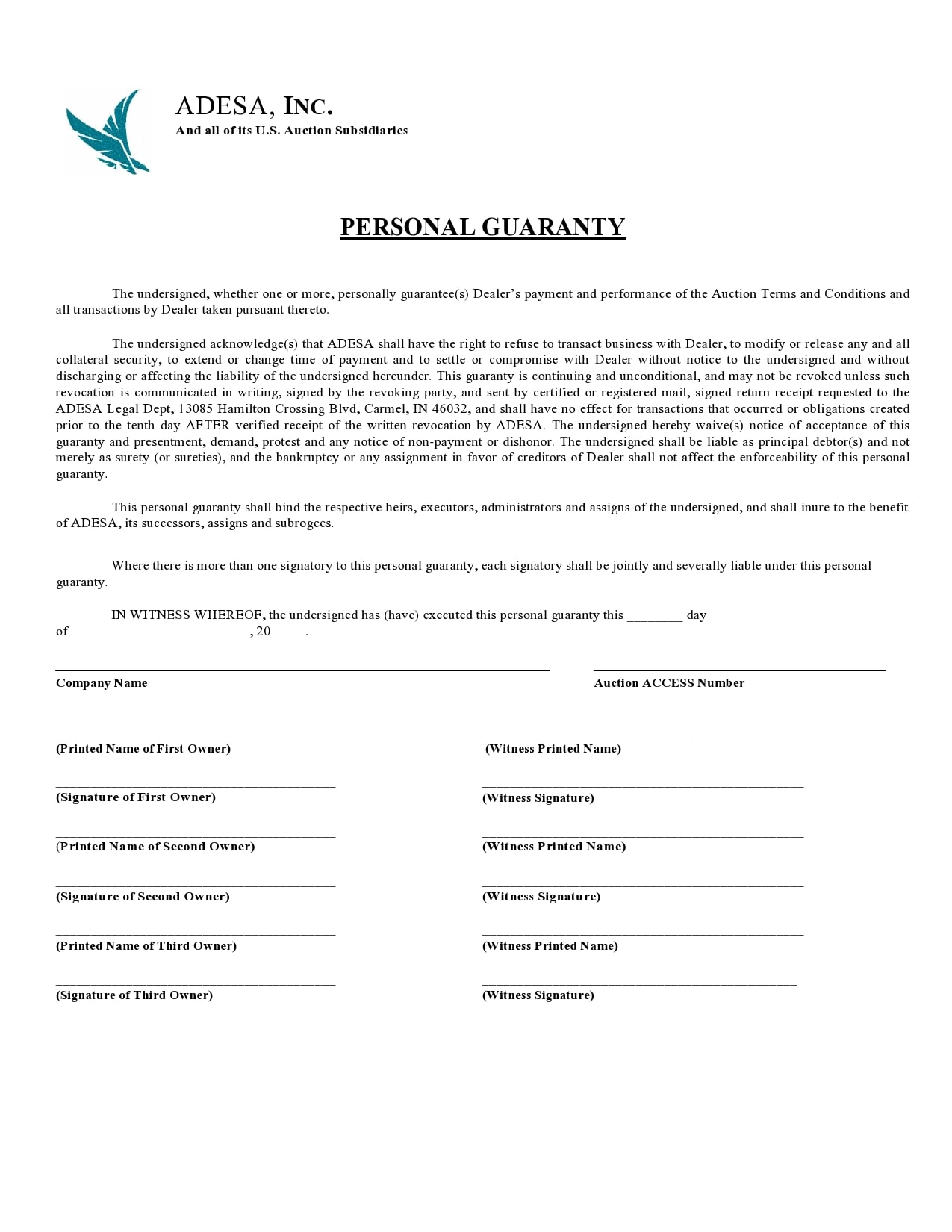

Personal Guarantee Templates

What does a personal guarantee look like?

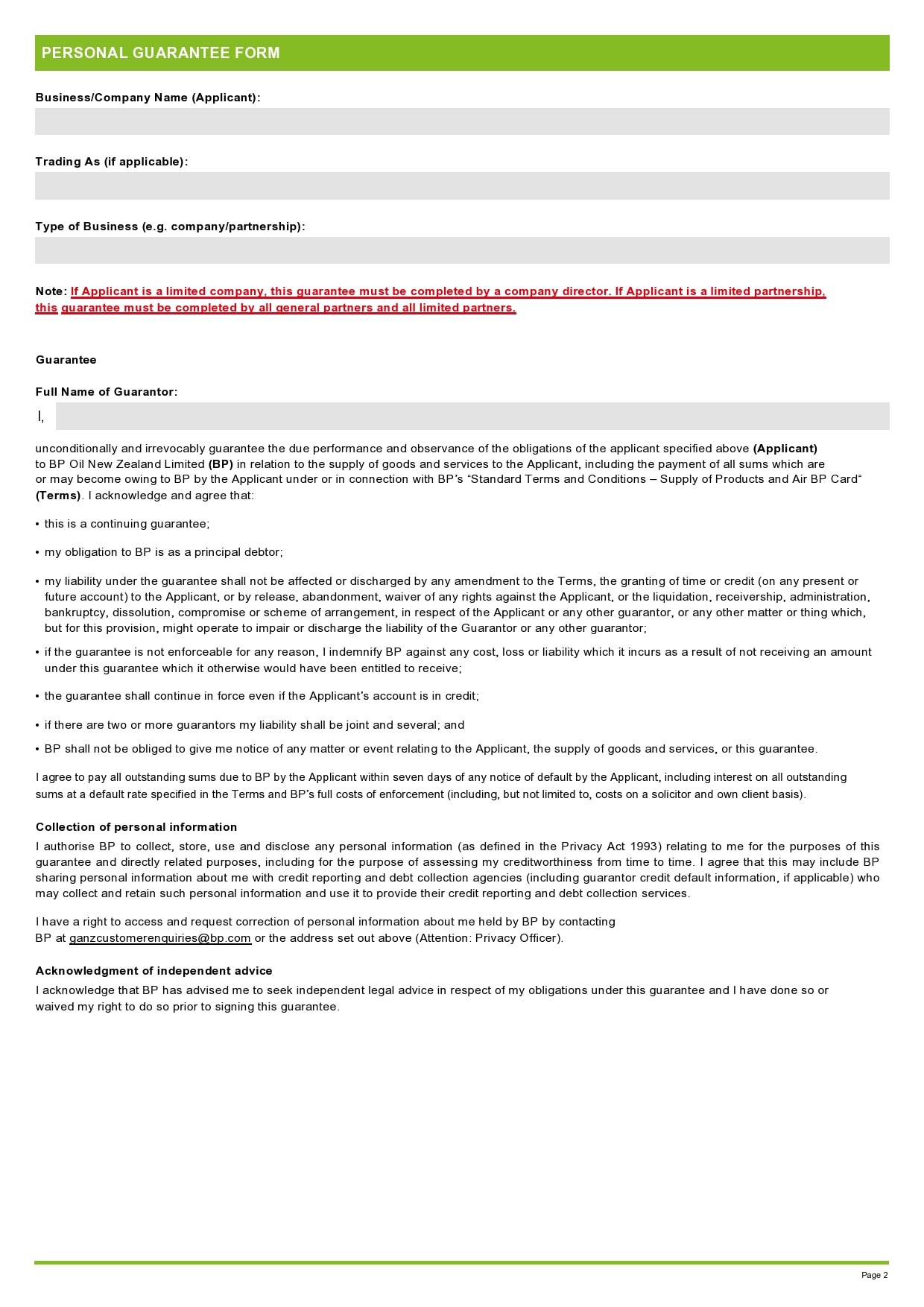

A personal guarantee form defines the entire loan balance, as well as, the specific condition in which the lender grants the loan. Since the lending standards can vary from state to state, specifying the state where you created the loan can easily help you determine the legal context and explicit provisions to include in the loaning contract.

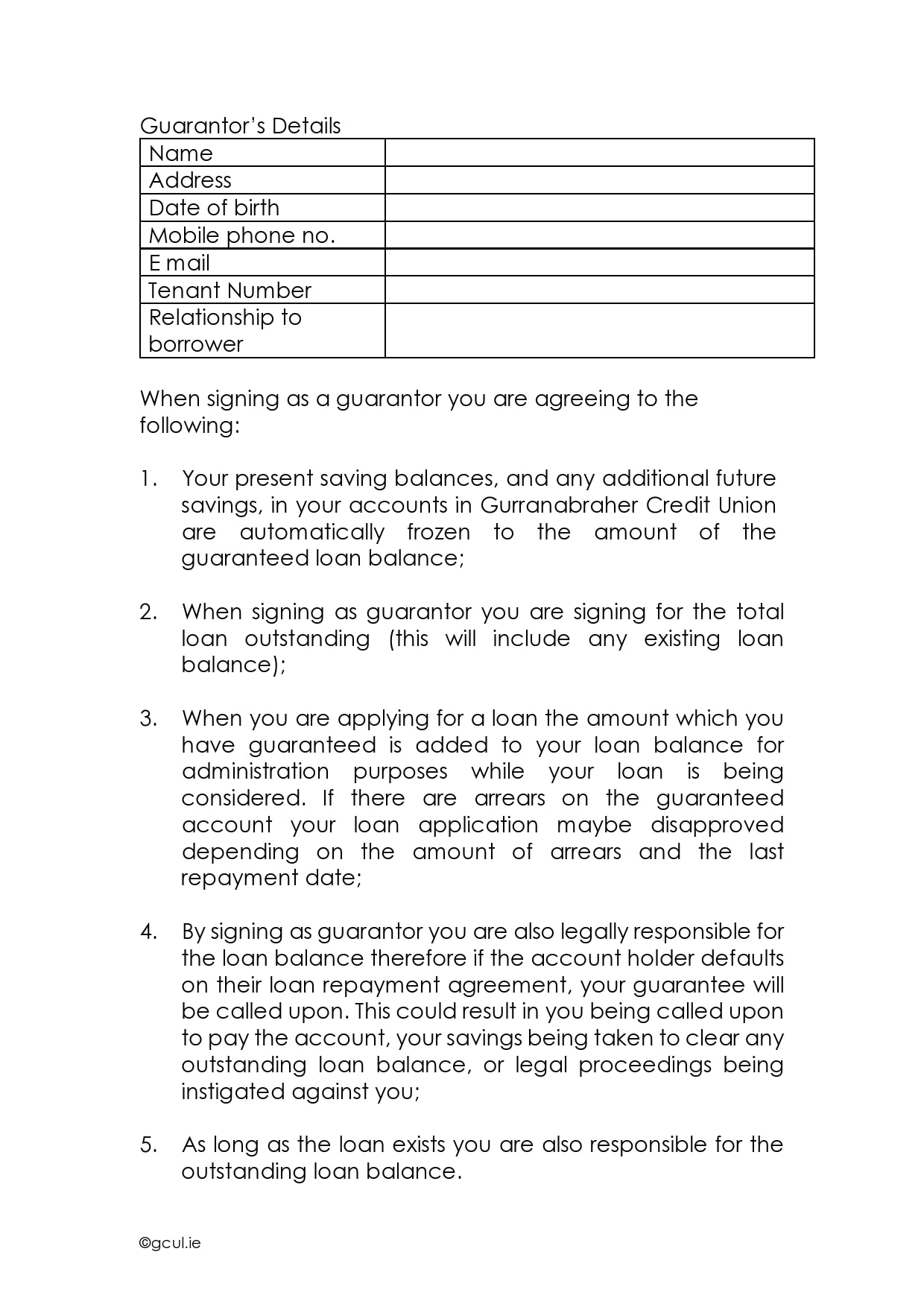

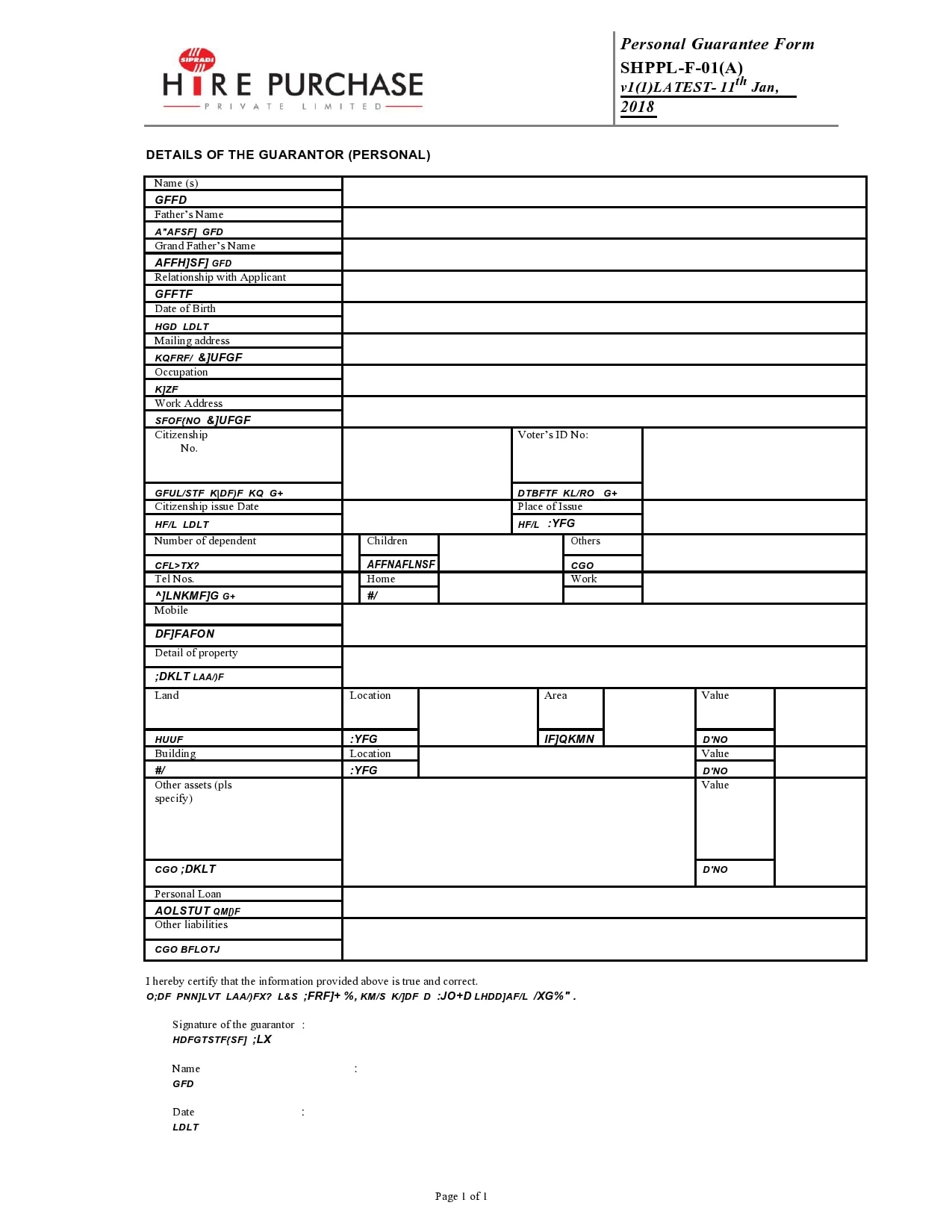

A personal guarantee letter or form must include the parties involved, together with their complete addresses. You should also make sure that the document has the signatures of everyone involved, dates, and some kind of authoritative symbol.

The borrower, lender, and guarantor should get copies of the document. Before you agree to any type of personal guarantee, consider the following first:

- Take a good look at your business or your finances.

- Understand the possibility that despite your best efforts and intentions, you might have to pay the loan as a guarantor.

- Look at all of the possible ways or how each provision within the agreement might affect your business or your finances in the future.

At the end of the day, you should ask yourself if the risk involved in becoming a guarantor is worth the price.

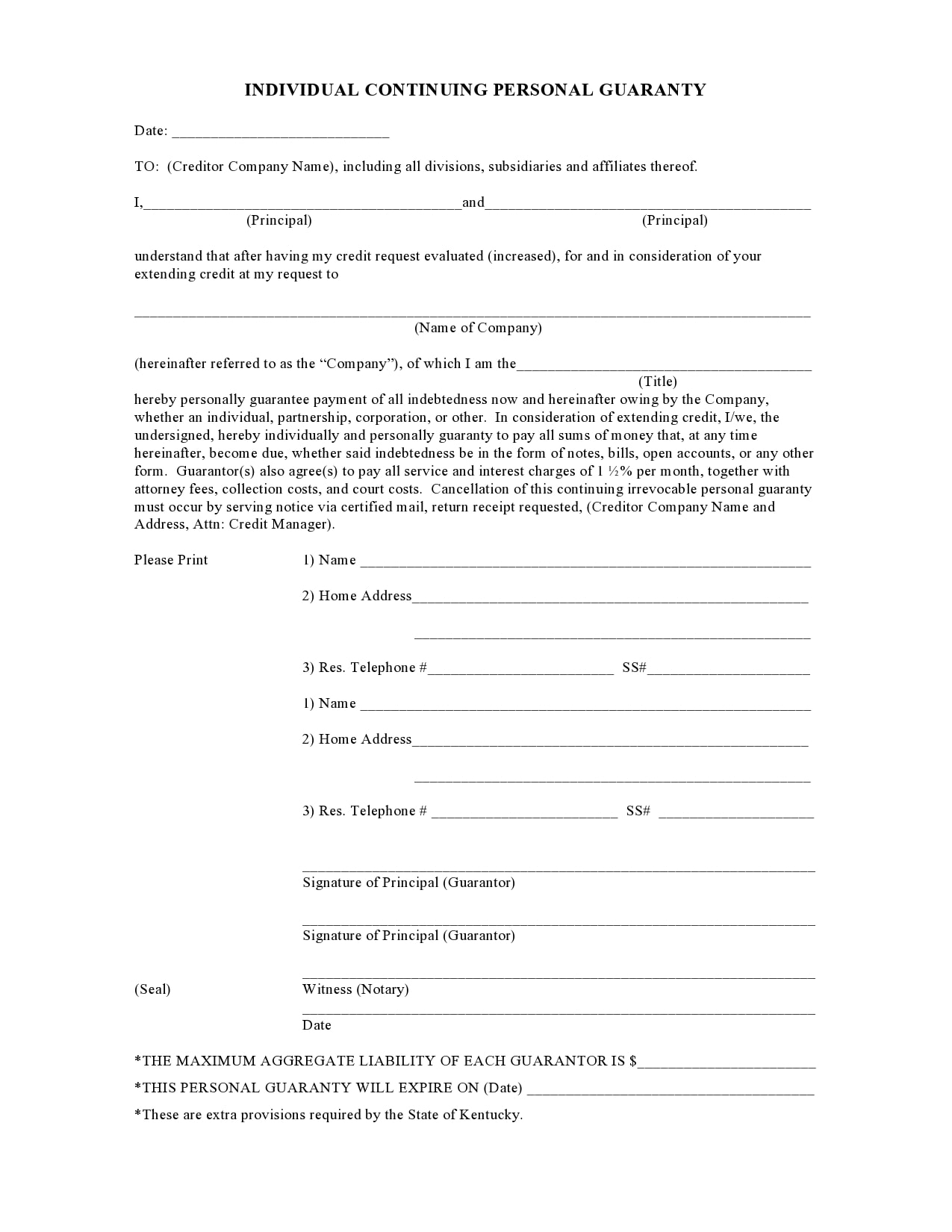

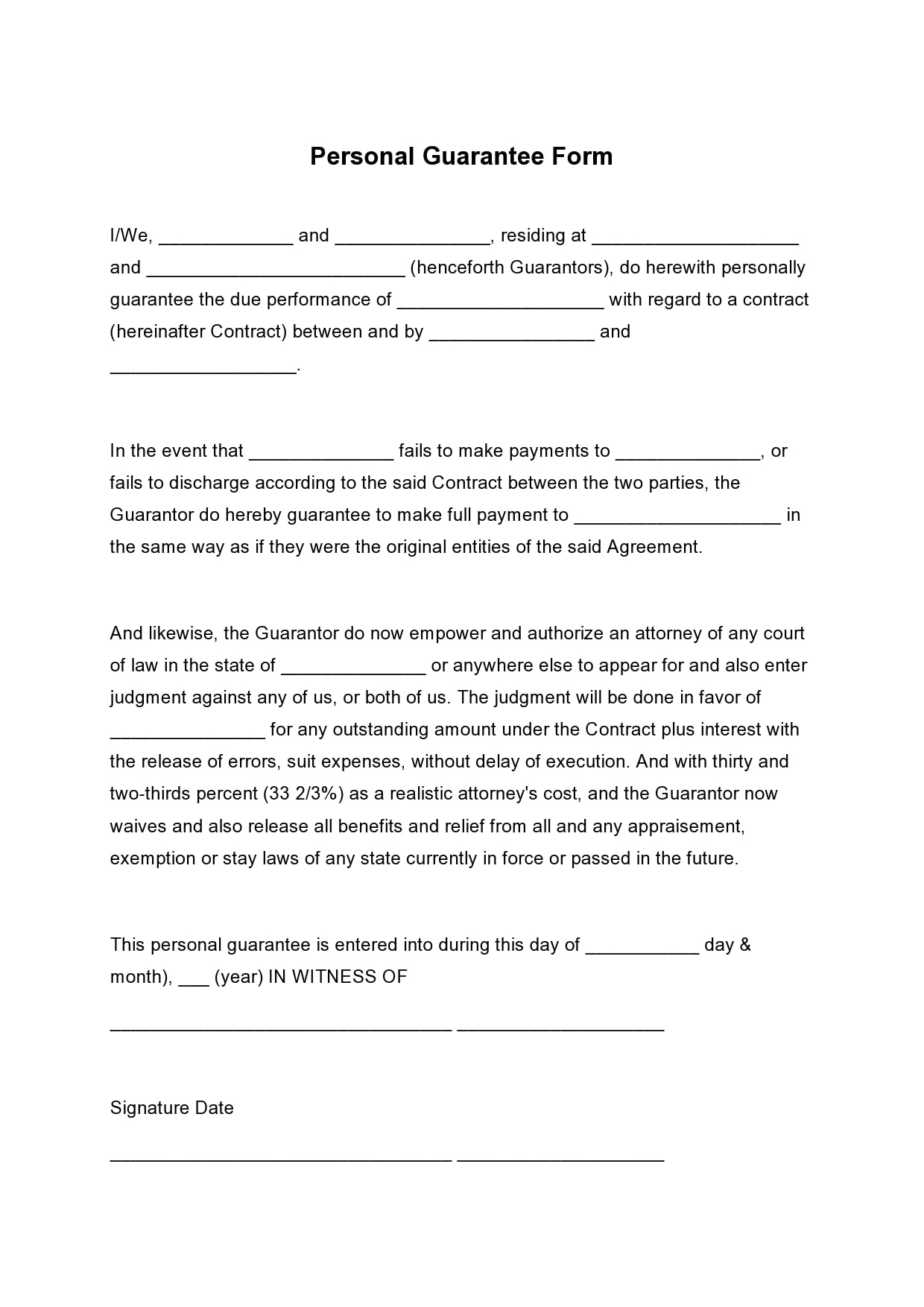

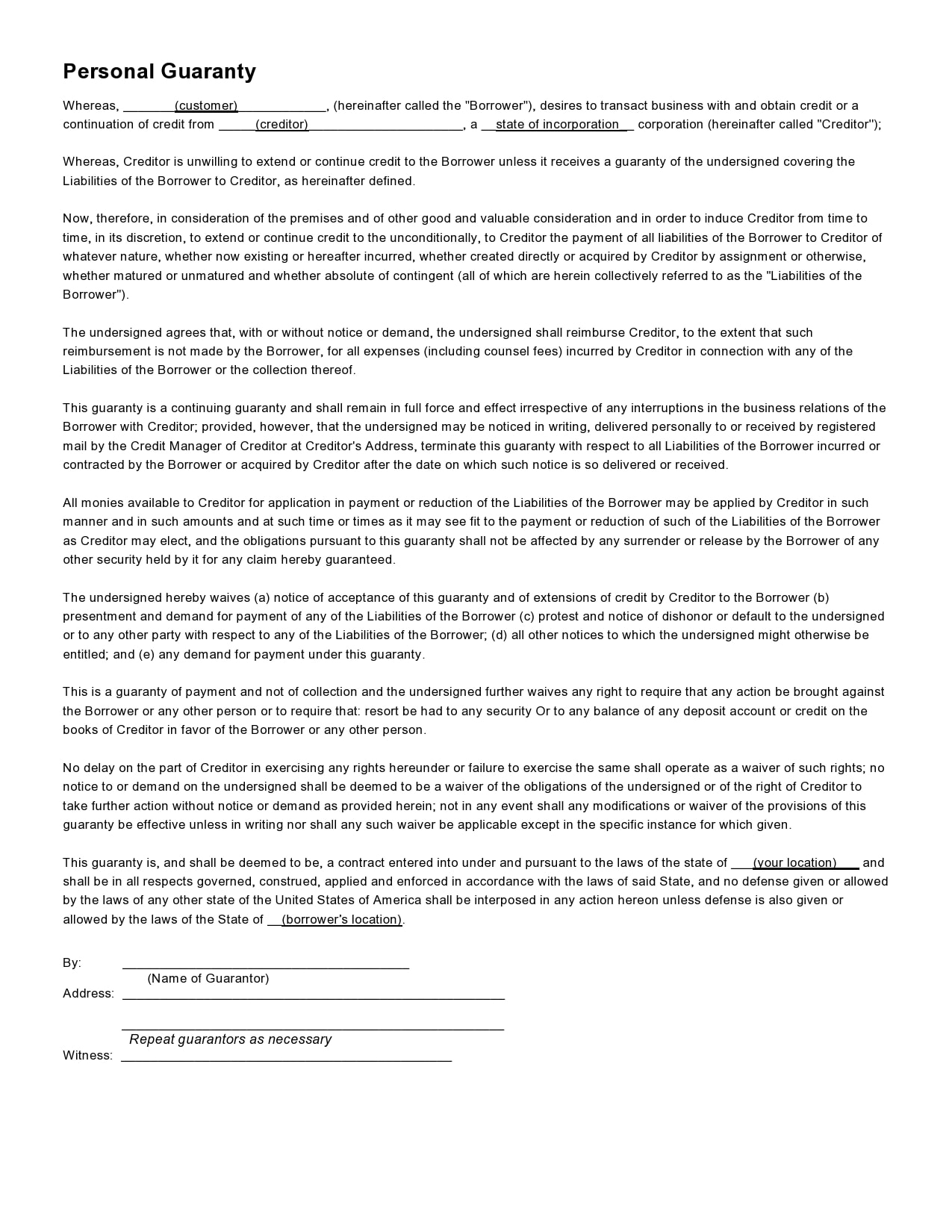

What to include in the document?

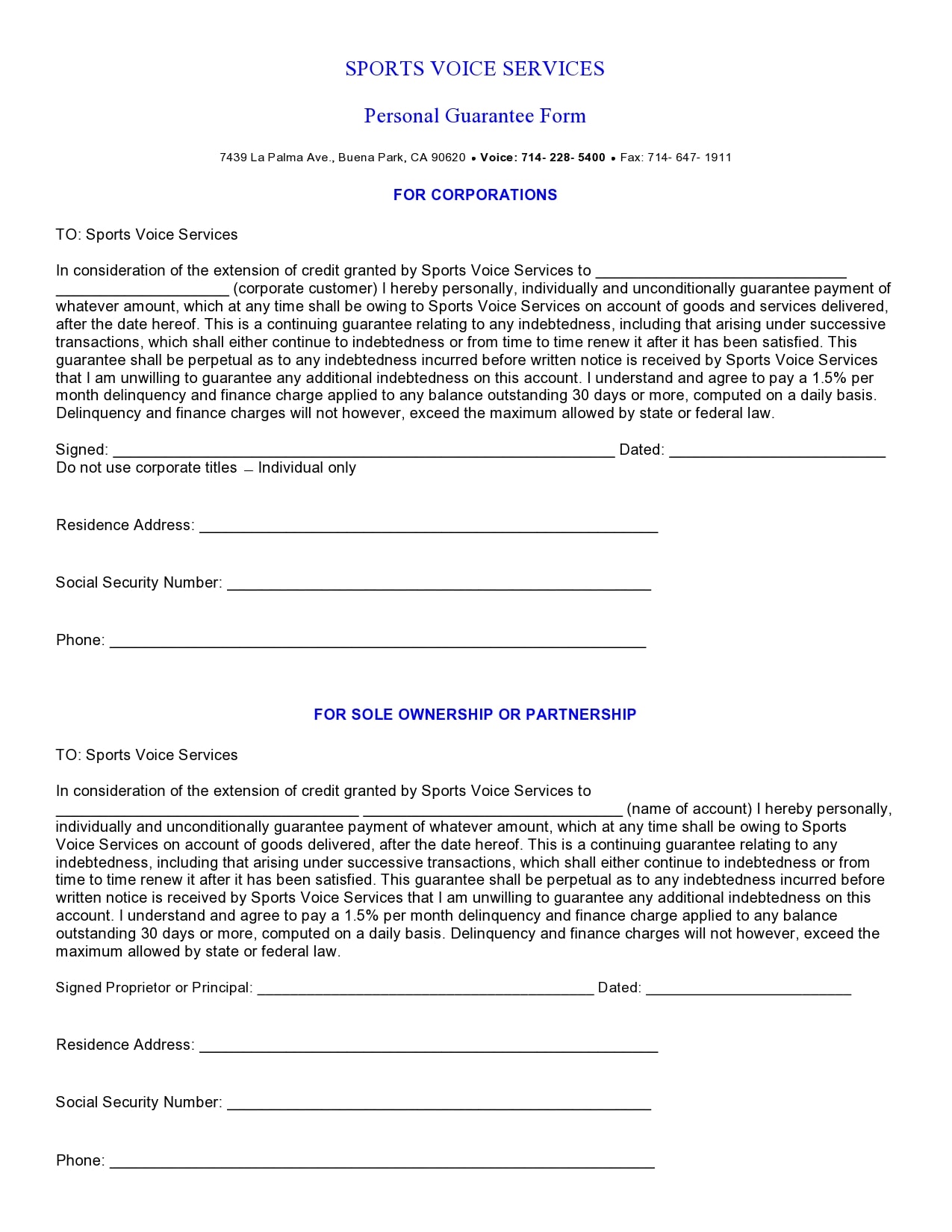

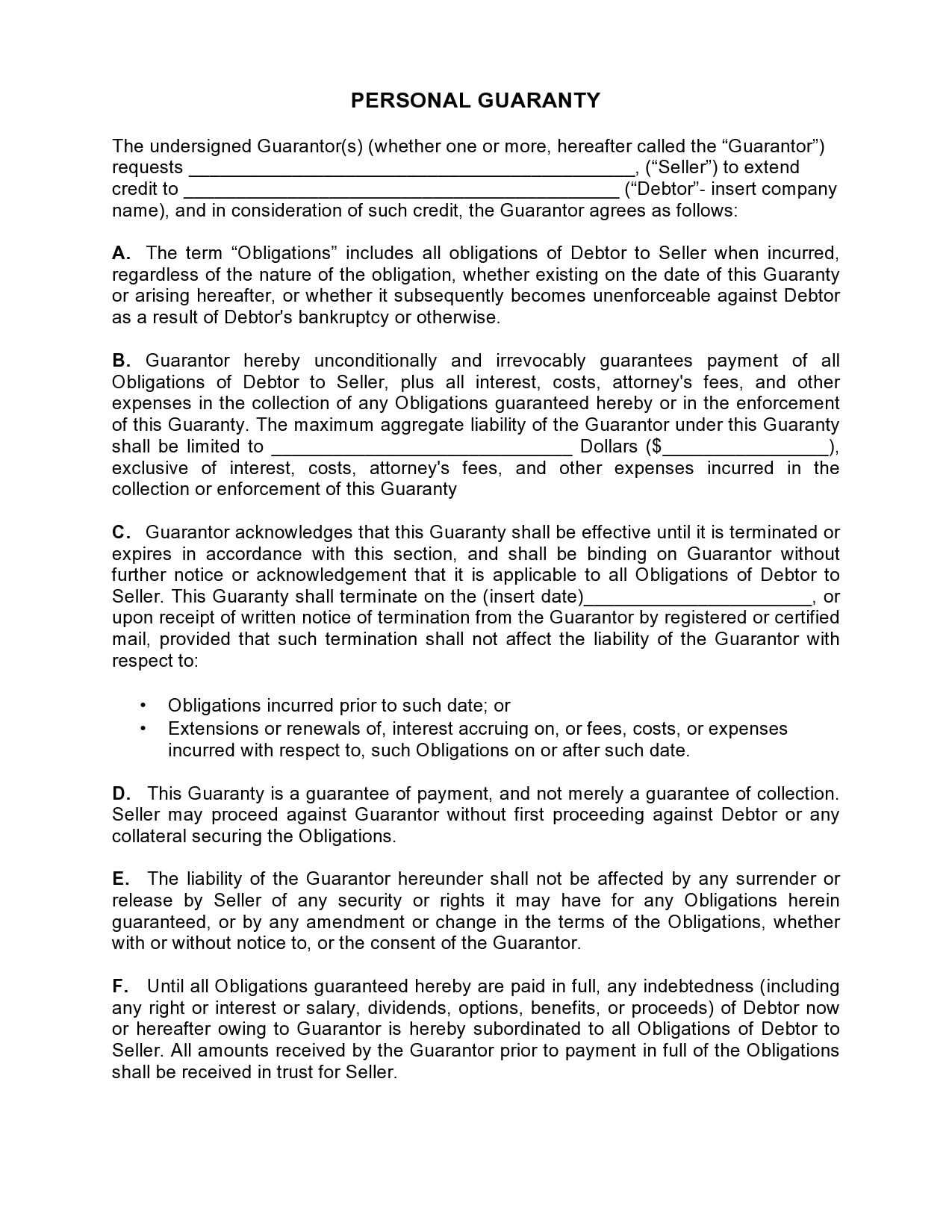

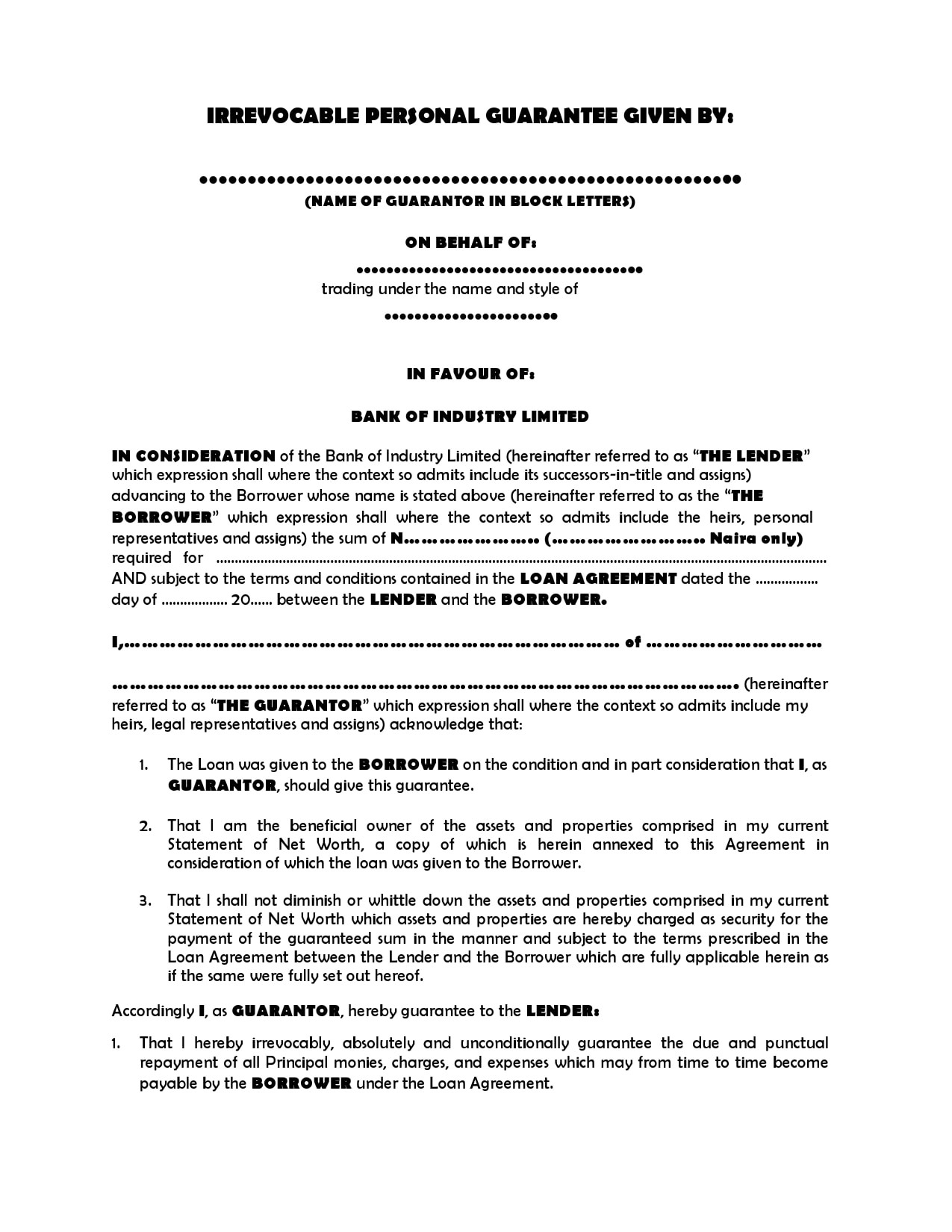

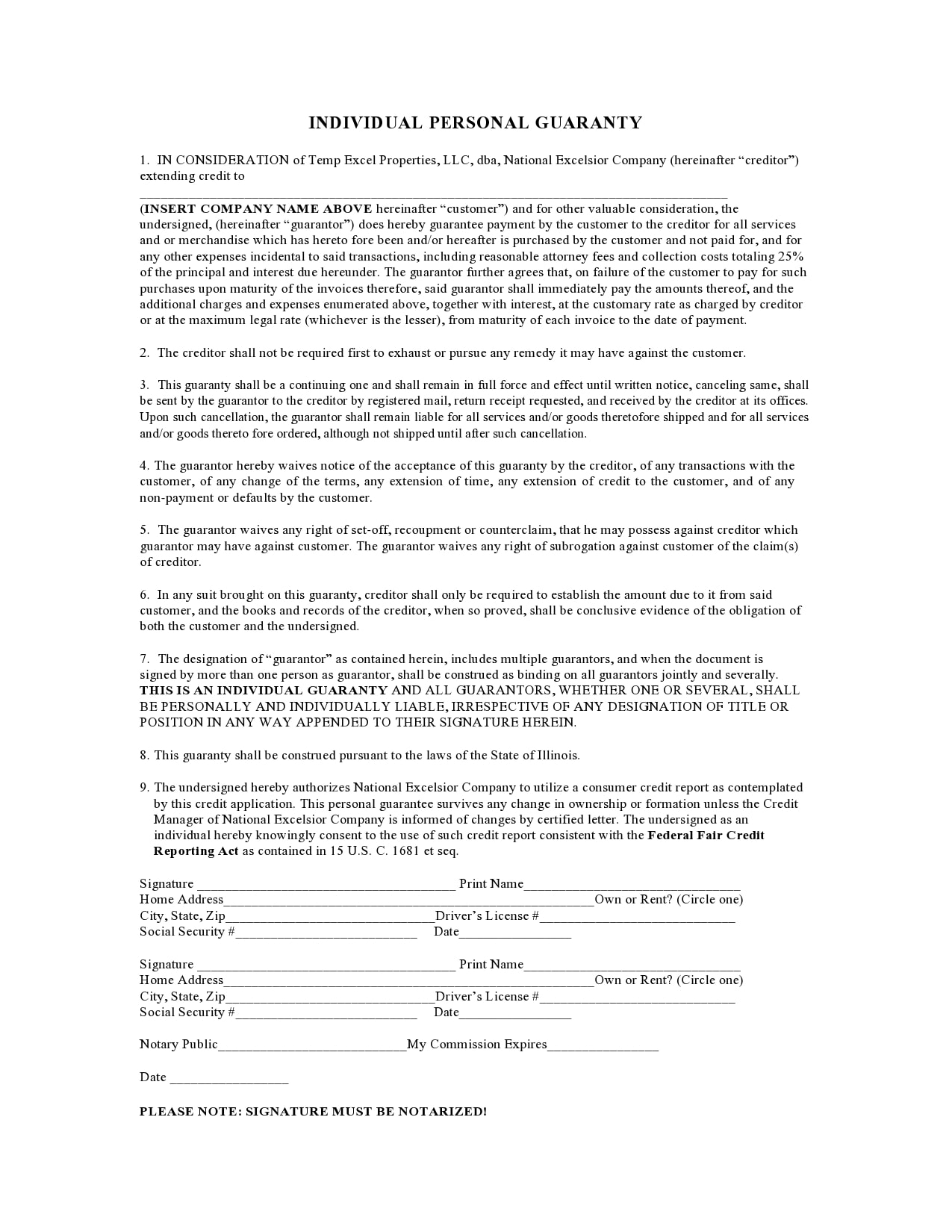

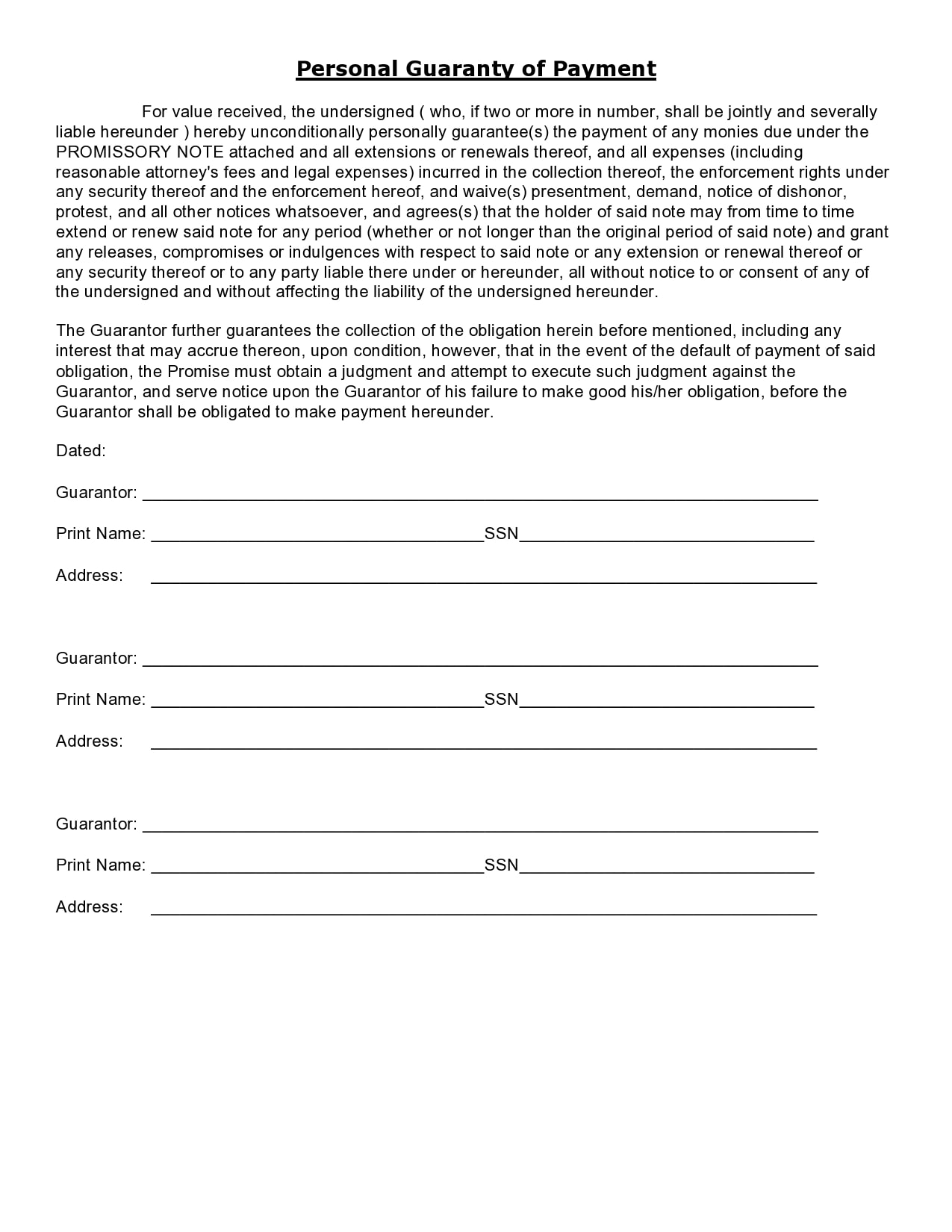

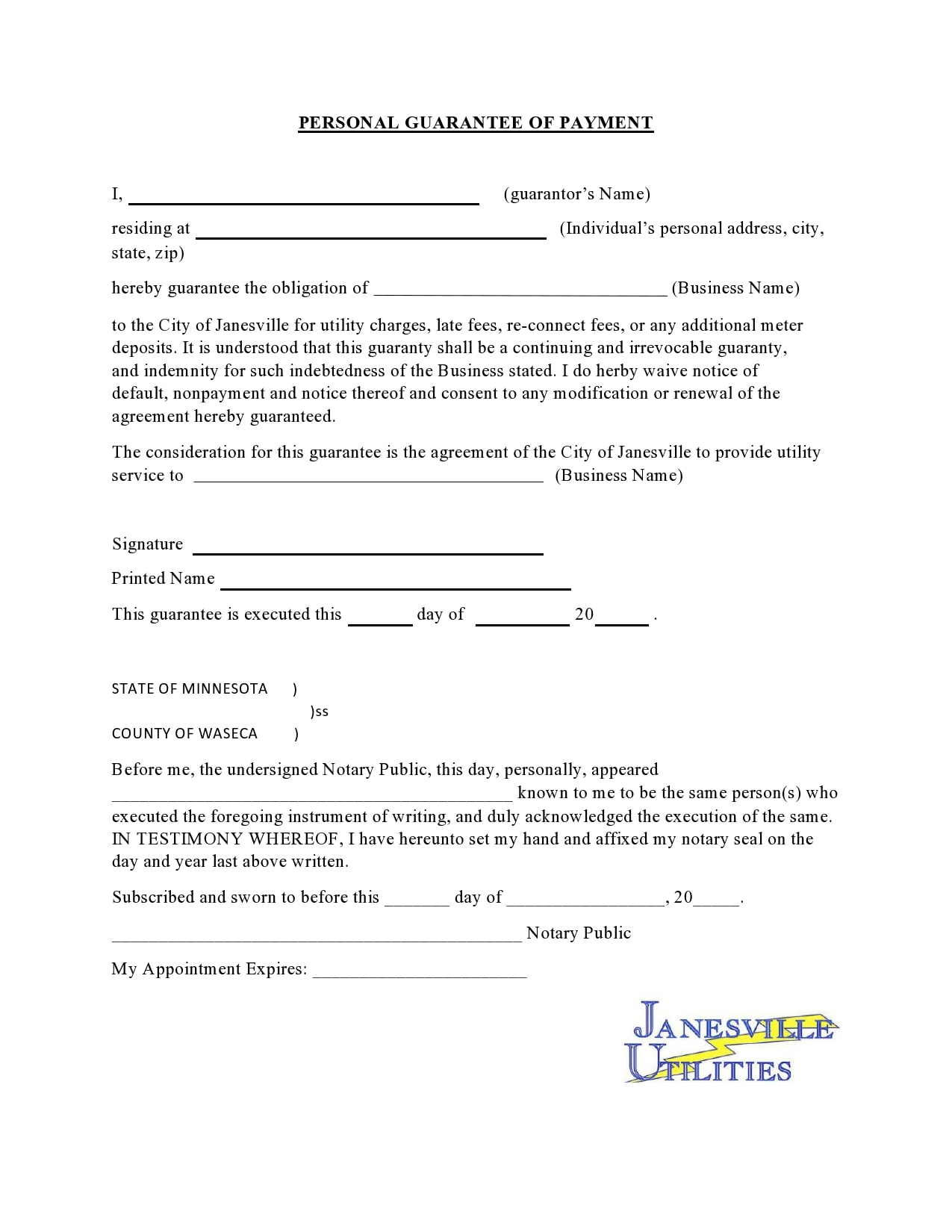

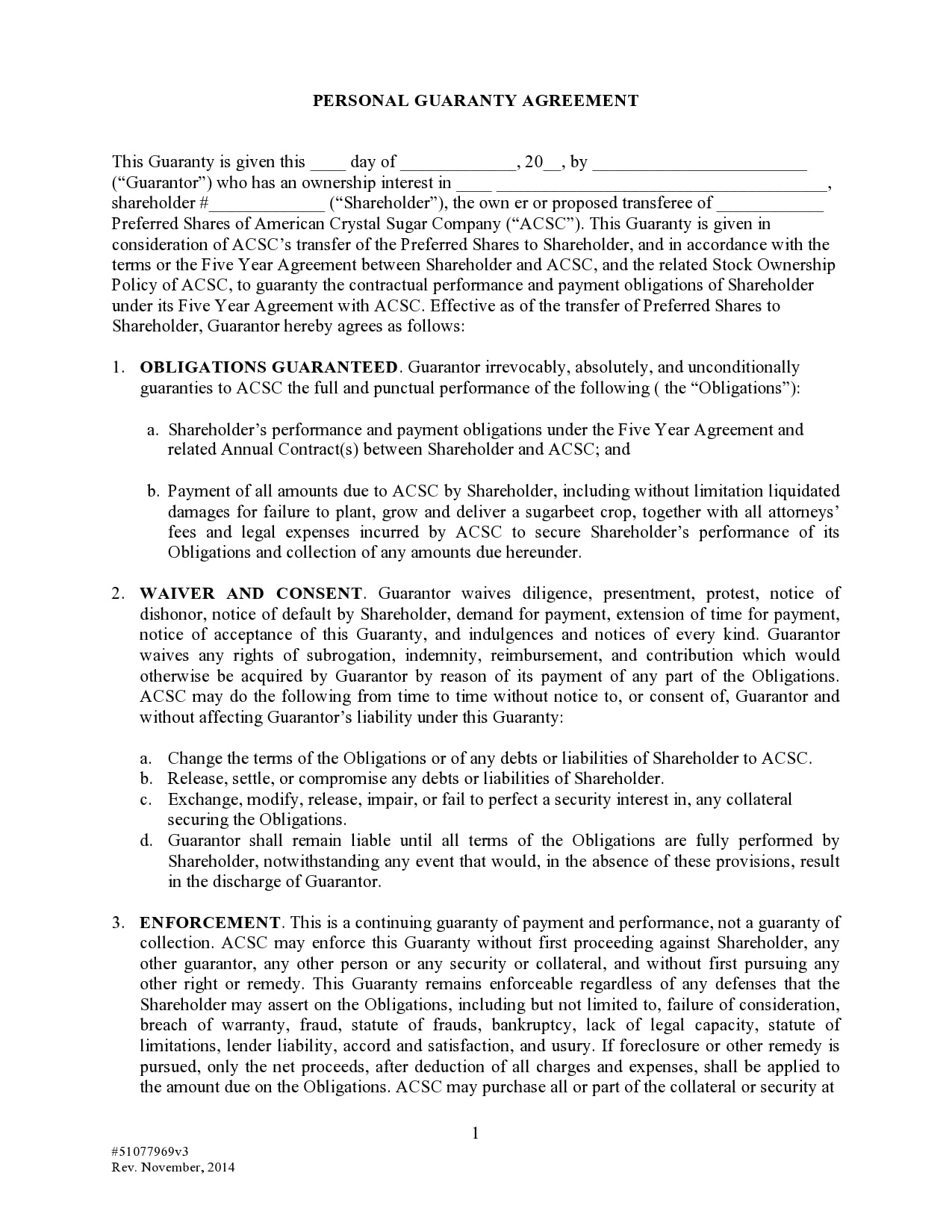

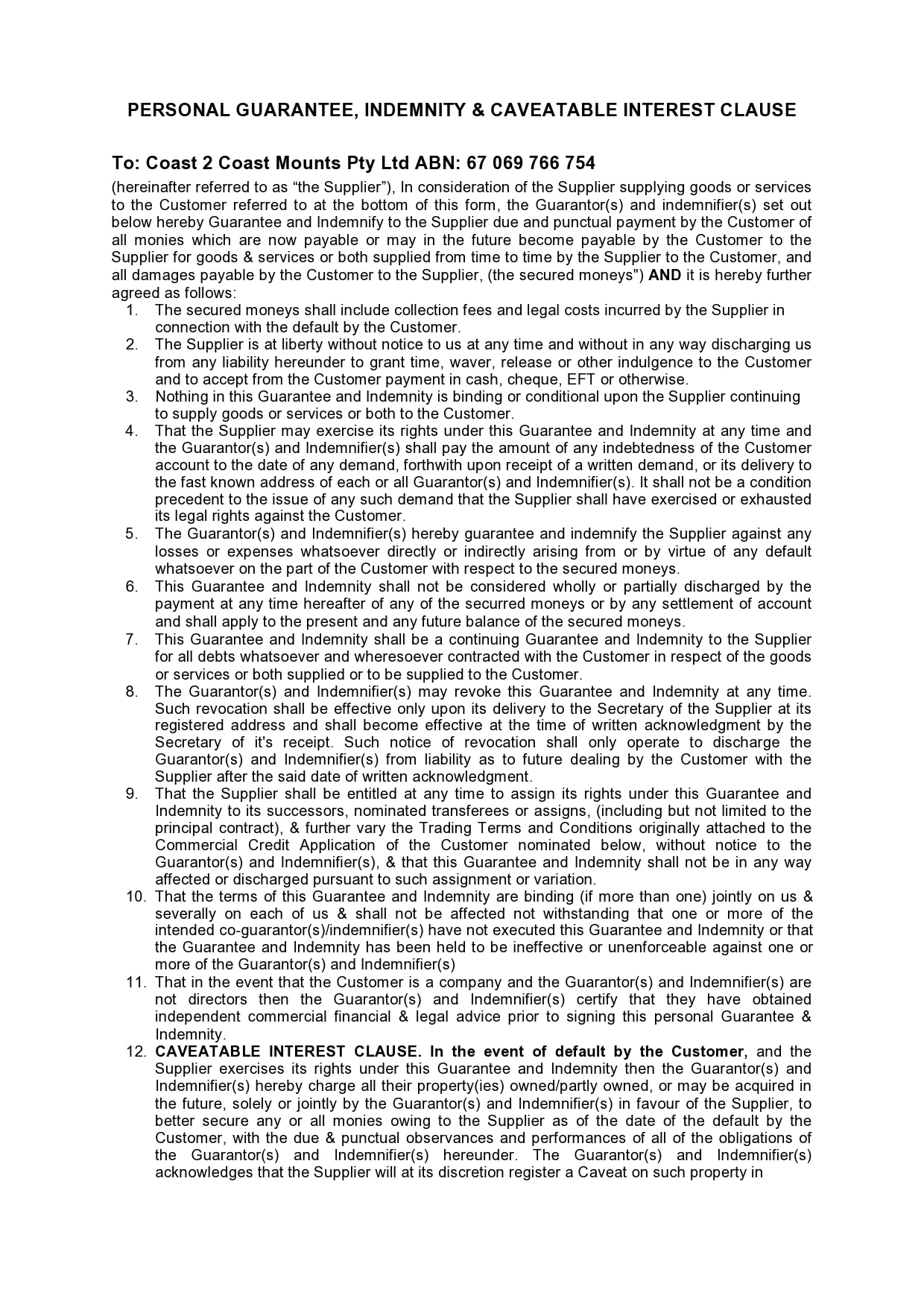

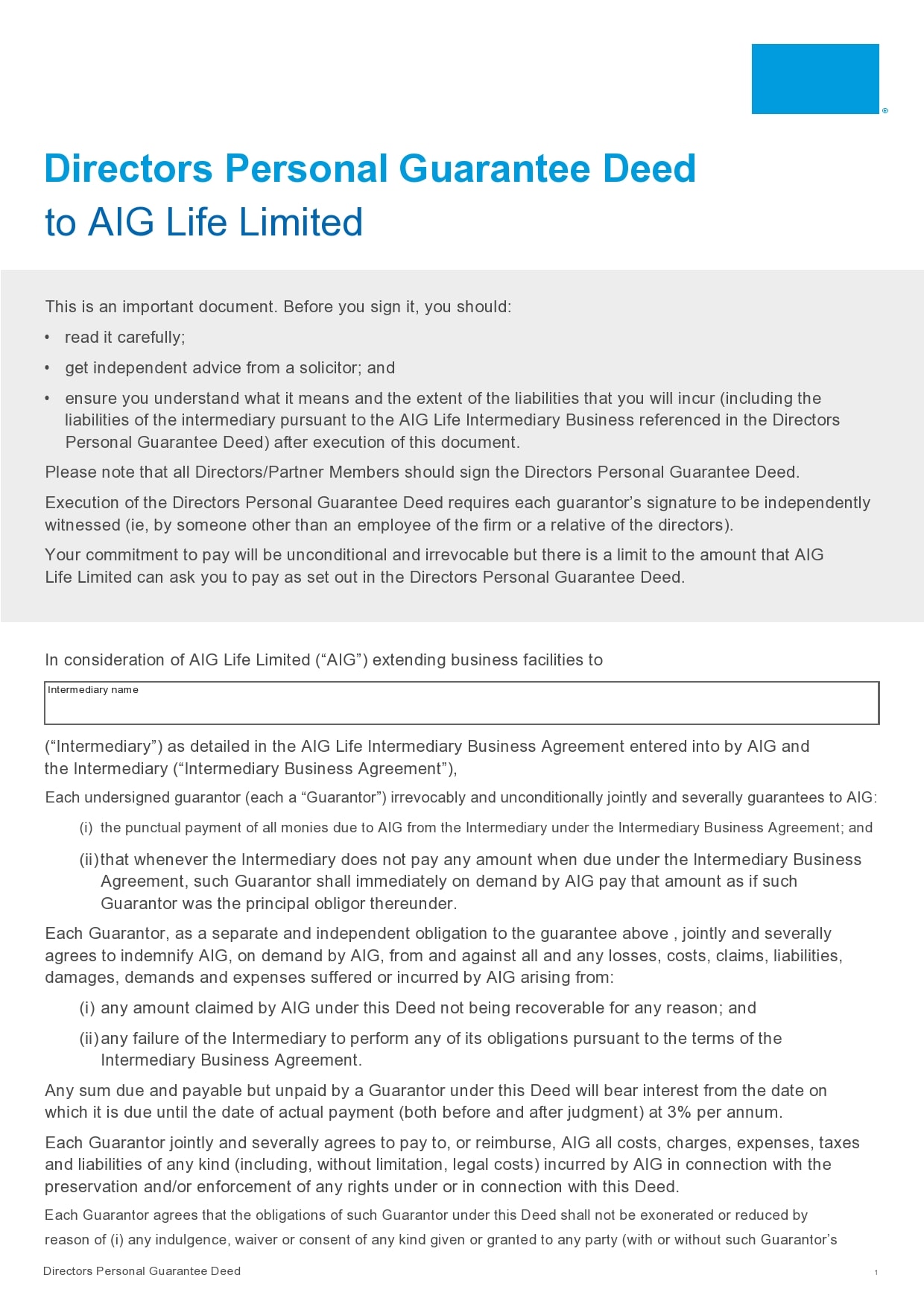

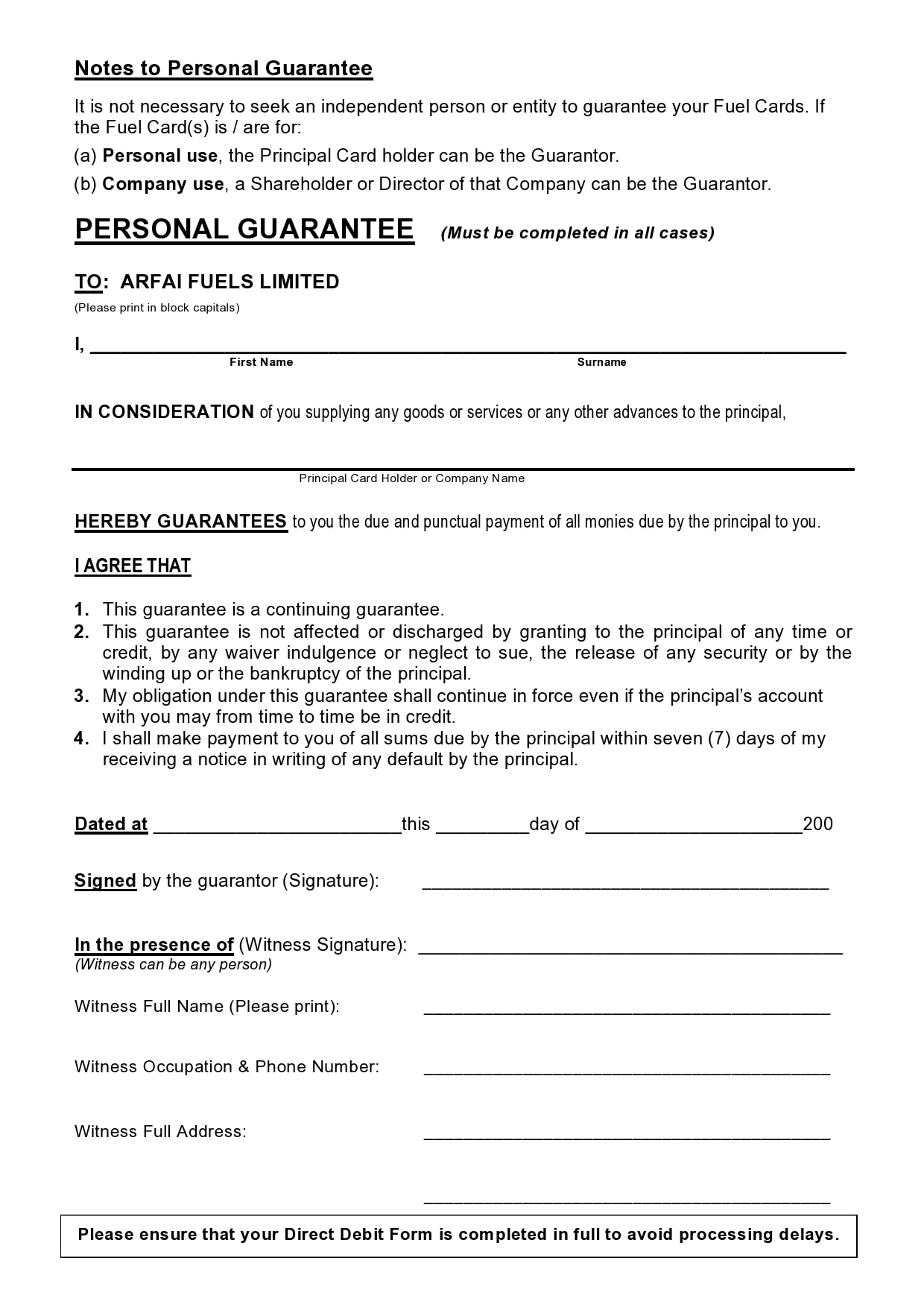

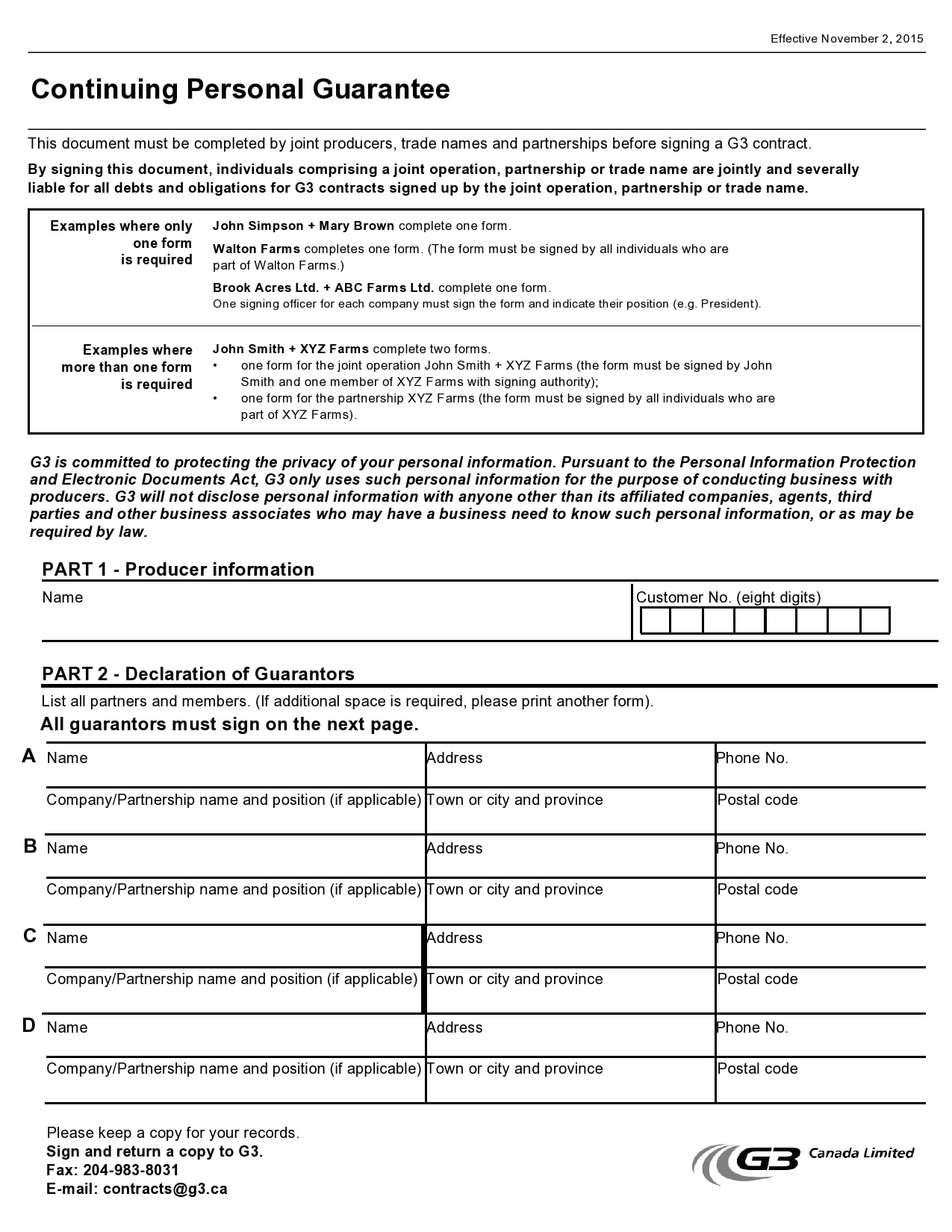

The essence of the personal guarantee form is the commitment of you as a guarantor to assume responsibility for the payment of the debt, in case the borrower fails to fulfill his obligation. In general, you’re subject to the same terms and conditions as the borrower and this includes a punitive situation should the debtor default.

This means you will have to pay back the whole remaining balance immediately. Additionally, since you are the financial backup of the borrower, the personal guarantee typically forbids you from transferring your assets or significantly altering your personal financial circumstances without the lender’s approval.

Every personal guarantee template should include details about the total balance of the loan and the state in which it got granted. Since the standards of lending vary by state, specifying a loan’s place of origin makes things much clearer for everyone involved.

Like any other legal agreement, this one should clearly state the names of everyone involves and your addresses. It should also have dates, signatures, and you can even have it notarized. Finally, copies of the agreement should get distributed to all parties too.

Personal Guarantee Letters

Who needs this form?

The use of a personal guarantee form is very common with certain organizations, groups or individuals:

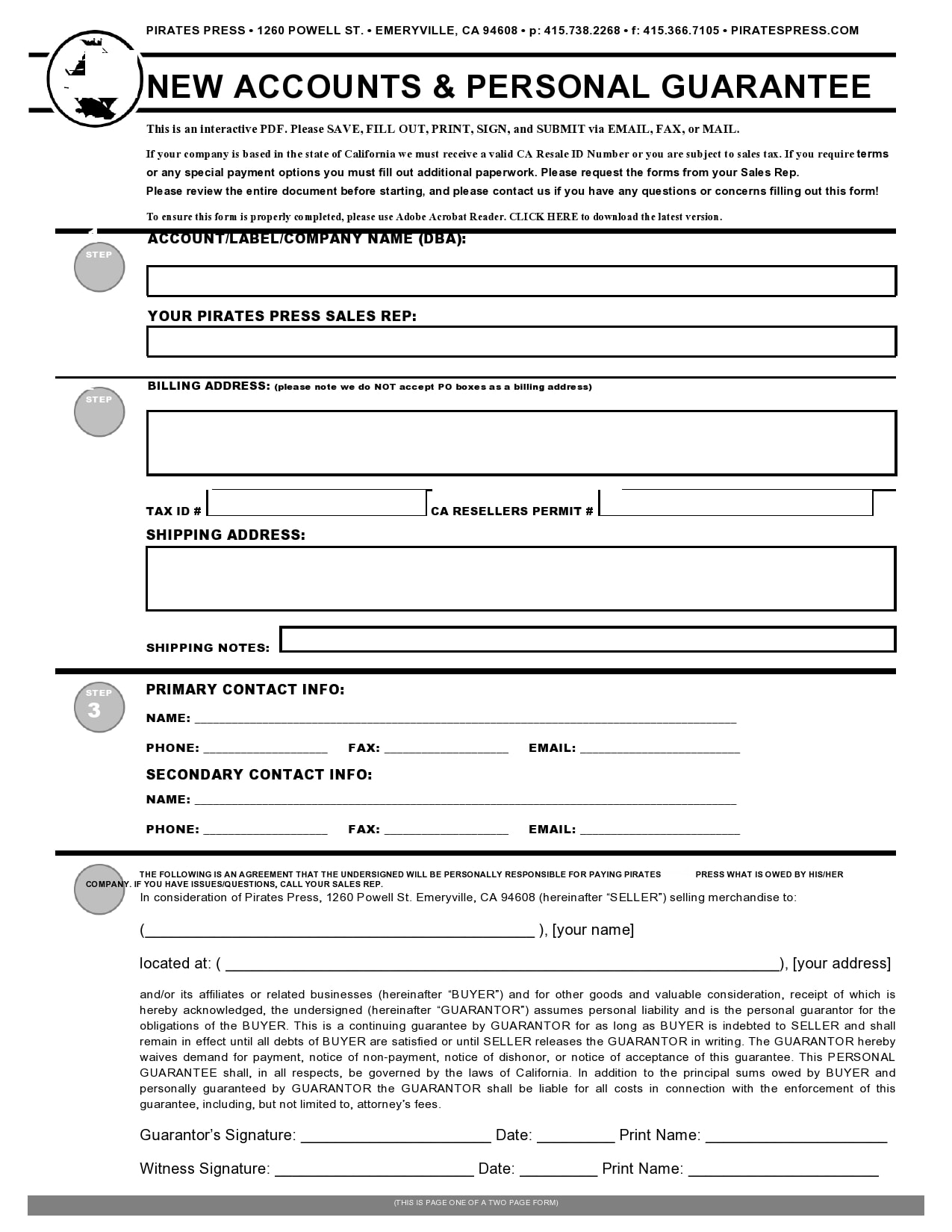

- Trading Companies

Business establishments will usually enter into different types of transactions with other institutions or companies and will need a personal guarantee letter or form. they will use it to document that the company that will trade to personally guarantee that they will perform as expected based on the terms and conditions set in the agreement.

Moreover, the document also specifies the State acts or laws that regulate the guarantee and the agreement in the whole duration of the transaction. - Lease Property Owners and Landlords

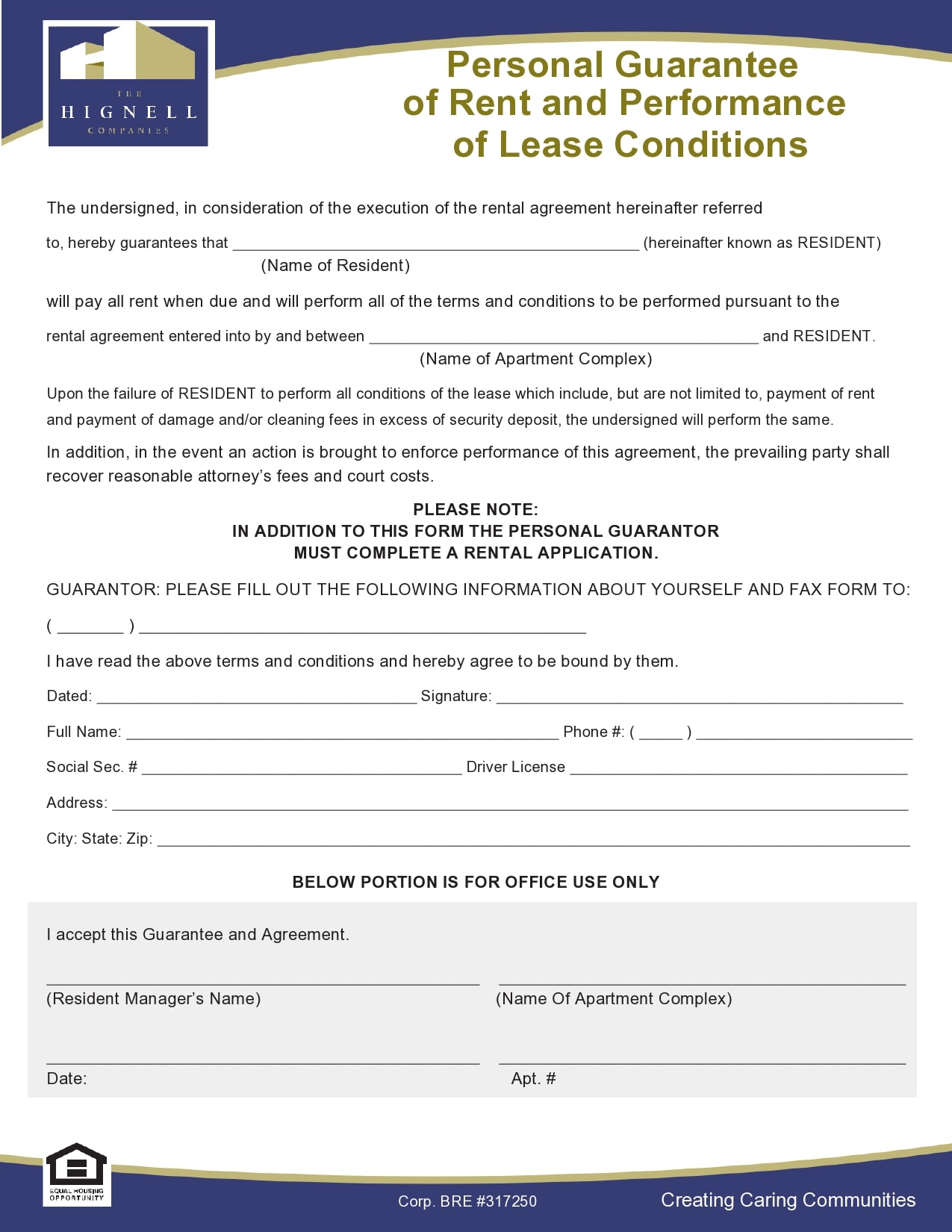

Another area where guarantee forms are generally used is in leases, like the owner and the landlord of leased properties. With this form, the owner or the landlord has the assurance and documented proof that the renter or tenant has a guarantor who will pay any dues in case of a default.

Furthermore, the form also provides general information about the guarantor, particularly their contact details that landlords can use to contact the guarantor and send notices that contain the details of the unpaid rental payments or fees. - Hiring Managers

The main reason why hiring managers of a company will use this form is to clarify and verify the latter’s employment claims and background. The hiring manager will use the form to collect the information regarding the guarantor, the applicant, and the previous company where the applicant worked for.

It will also contain the guarantor’s assessment regarding the performance of the applicant, along with their strengths and commitments while they worked in their previous company. This means that the personal guarantee serves as a supplement document for the applicant’s character reference and application. - Insurance Providers

The intension of a personal guarantee for insurance providers is for the recording of basic information of the applicant and the guarantor who will shoulder the payments in case the applicant doesn’t pay their financial obligations to retain their insurance coverage.

In such a case, the applicant may have several guarantors. Additionally, insurance providers also include in the agreement, the terms and conditions which the applicant should agree to and follow. All of the parties involved should also read these terms and conditions for them to comply.